- Quick take

- Yesterday, 16:05

- United States

US sentiment underlines K-shaped consumer strife

Consumer sentiment is off its lows, but remains very weak. However, the relationship with spending has been poor recently, reflecting the growing influence of higher-income households who have seen their finances boosted by surging property and stock market wealth

Sentiment gets a lift, but remains weak

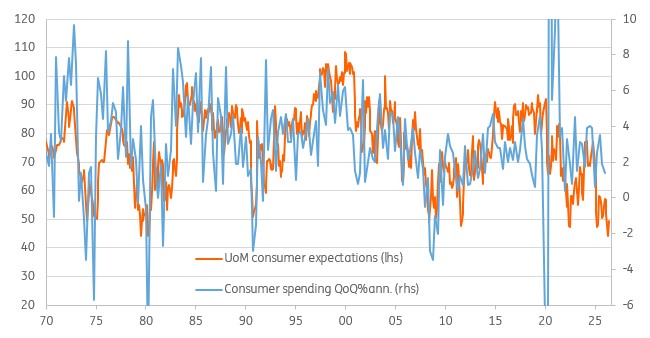

The University of Michigan sentiment index has improved to 48.9 from 44.8 (consensus 46.0), but this remains at very weak levels by historical standards. The chart below suggests the latest reading should be consistent with consumer spending falling around 1.5% year-on-year. However, consumer spending is being driven by higher-income households who are buoyed by big wealth gains, whereas sentiment reflects the median American. Unfortunately, they are seemingly finding the current economic situation much more challenging.

Consumer confidence & spending 1970-2026

High income households are driving the growth in spending

Bureau for Labor Statistics data suggests the top 20% of households by income (those making $155k or more based on 2024 numbers) account for more than 40% of all spending. Moody's Analytics suggests the skew towards high-income households is even greater, with their data indicating that the top 20% are currently accounting for more than 60% of all consumer spending!

Consumer confidence reflects the median household, which is much more concerned about weak income growth and high prices – remember that real household disposable income has fallen for three straight months. Federal Reserve data also shows that the bottom 60% of households by income, which obviously includes the median person, only hold 15% of the wealth of America. As such, the surge in stock and property prices has not had the same positive boost as for high-income households who hold 70% of the wealth.

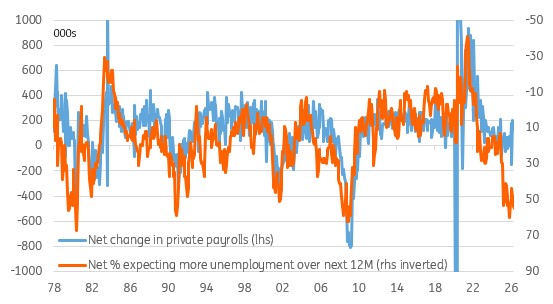

Unemployment fears & US jobs

Cooling inflation expectations dampens rate hike prospects

Today’s survey also suggests there is real concern about job security, with a net 54% of respondents expecting unemployment to rise over the next 12 months. That reading is on a par with the readings experienced during the Global Financial Crisis and the early 1990s recession.

In better news for the Federal Reserve, inflation expectations receded, with the 1Y ahead reading dropping to 4.6% from 4.8% (consensus 4.9%), while 5-10Y ahead dropped to 3.4% from 3.9%. Today’s moves in oil prices on the back of positive news on the prospect of a deal to reopen the Strait of Hormuz, suggest that retail gasoline prices could drop back below $4/gallon next week, having recently been as high as $4.60/gallon. This should mean further declines in both market and consumer inflation expectations, which would remove a key argument that hawks use to justify calls for higher US interest rates. We expect the Federal Reserve to hold rates steady next week and not hike at all in this cycle, as we outlined in our FOMC preview.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more