RBA to cut next week, and again in August

Seldom has a central bank rate decision been so clearly flagged - the market focus will be on how much more easing is coming and how soon

| 1.3% |

CPI InflationTarget rate is 2-3% |

New easing cycle, or just the old one extended?

August 2016 was the last time the RBA changed interest rates. This was the last cut in a series of eleven rate cuts that started in 2011 when the cash rate was 4.75%. One could make a case that the extent of the easing was in part determined by the rate increases that preceded it, with emergency easing during the global financial crisis being unwound rapidly from late 2009 until late 2010. You could say that next week's cut and the likely cut or cuts that follow this year and possibly next will simply mark a continuation of the interrupted easing process that started in 2008.

Cash rate history

What has changed?

So much for the history lesson, what about this particular meeting?

There has been a distinct change in rhetoric from the RBA this year. This started in February with a move from a tightening bias (though admittedly with a long time horizon) to a neutral stance. The full argument for the change is fleshed out in the Opening Statement to the House of Representatives Standing Committee on Economics in February this year by Governor, Phillip Lowe.

But in short, this shift acknowledged some softer consumer spending figures and house price corrections, together with enhanced risks from the global environment - the trade war and China. 4Q18 Inflation at this time was 1.7% and had just shown some signs of softening, having been 1.8% in 3Q18.

Switch to easing bias

By the time he made his speech to the Brisbane section of the Economics Society of Australia on May 21, 1Q19 inflation had dropped to only 1.3%YoY. Governor Lowe turned the screw even more firmly in a dovish direction.

Here, he described the discussions of the RBA board, saying, "...we discussed a scenario in which there was no further improvement in the labour market and the unemployment rate remained around the 5 percent mark. In this scenario, we judged that inflation was likely to remain low relative to the target and that a decrease in the cash rate would likely be appropriate. A lower cash rate would support employment growth and bring forward the time when inflation is consistent with the target. Given this assessment, at our meeting in two weeks' time, we will consider the case for lower interest rates".

To cut a long story short, without a sizeable fall in the unemployment rate, the RBA now does not believe that inflation can move back to target and that one of the things they can do to make up for this shortfall, is to cut rates.

There has been no labour market data since then, and there will be none before the meeting on 4 June. The next labour market report is not until 13 June, and the subsequent rate meeting not until 2 July. Further labour market data for June is released on 18 July, and the next quarterly inflation report is not due until 31 July.

We would be very surprised if the RBA did not kick off its easing process at the meeting on 4 June. Markets are certainly geared up for it, with Bloomberg showing the implied market probability of a cut standing at 87.2% at that meeting. By August, markets imply more than a 50% probability of a further cut. We concur. By then, the RBA will have received more data on inflation, as well as further labour market information.

90-Day bank bill futures (implied 3m rates)

How low can they go?

After that, cate cut probabilities remain quite high. The 3 December RBA meeting is now priced at about a 40.4% chance of a further cut, though for the moment, we are holding off at 2 cuts this year.

- Firstly, the government is likely to have put together some fiscal stimulus by then, and this can take over some of the heavy-lifting from monetary policy in late 2019 / early 2020. At the very least, it may make sense for the RBA to see how this plays out before embarking on further easing.

- Secondly, the viewpoint that the unemployment rate can probably go lower before it starts to drive inflation higher, is subject to the possibility that Australian unemployment may not ever fall far enough to bring inflation back to 2.5%. This is a global rather than Australian phenomenon and reflects globalization. it also reflects the change in the nature of goods and services we buy, as well as automation of jobs, even in the service sector courtesy of Artificial Intelligence and other technology. At some point, the RBA may recognise that this is the pursuit of the unattainable and reconsider its tactics.

- Thirdly, by early 2020, with the US Presidential election race having kicked off in earnest, we imagine that the trade war will at least have entered a state of cease-fire, and global tensions may have eased somewhat. The risk to our forecast of 50bp of rate cuts before cash rates trough is that we will have to be somewhat more aggressively dovish. But we are not going to rush to join the race to the bottom that some of our peers seem engaged in, with some houses penciling in a full 100bp of easing before policy rates trough.

AUD to drift lower, gradually

Given the aggressive market pricing of rate cuts by the RBA, we suspect that the negative impact on AUD could be relatively limited for the time being. Three additional considerations support this view:

- In the absence of a clear commitment by the RBA to more rate cuts, the 3M-1Y segment of the yield curve could face little risk of downward adjustments for now.

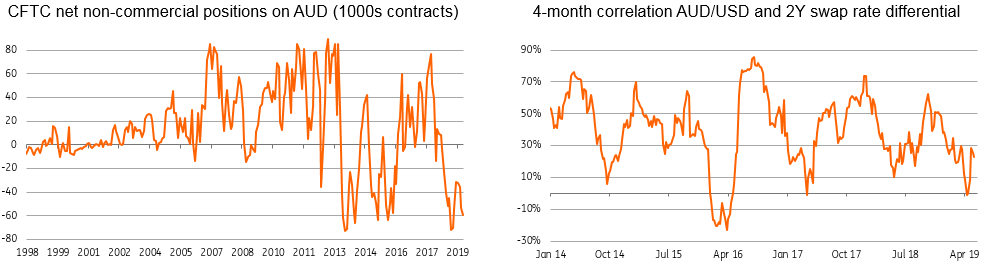

- CFTC data show that market short positions on AUD are close to historically high levels, which suggests that further depreciation could face some position-squaring related resistance.

- Correlation between AUD/USD and the short-term swap rate differential has slightly recovered of late, but is still far from being a significant driver of the pair.

Despite expecting a relatively contained move in the immediate aftermath of the meeting, we remain in favour of AUD/USD downsides in the upcoming months. In addition to gradual market pricing of future RBA cuts, we expect a further deterioration in US-China trade relationships to pressure the pair. We therefore expect AUD/USD to approach the 0.68 area in Q3 2019, in line with our most recent forecast.

Positioning and correlation suggest relatively limited downside risk for AUD

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap

30 May 2019

Good MornING Asia - 31 May 2019 This bundle contains 4 Articles