Polish GDP growth beats expectations as core inflation rises

The Polish economy saw 3.2% YoY growth in the second quarter of the year, led primarily by consumption. A wave of downward revisions to 2024 economic growth forecasts was likely premature. With solid GDP growth and detailed June CPI data illustrating a rise in core inflation, we see no room for rate cuts from the National Bank of Poland this year

Robust second quarter growth led by consumption

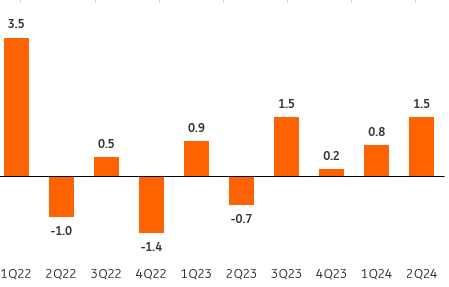

The Polish economy grew by 3.2% year-on-year in the second quarter of this year (ING and consensus: 2.8% YoY), compared to 2.0% YoY in the first quarter. according to the flash estimate. The seasonally adjusted data shows strong growth of 1.5% quarter-on-quarter after a 0.8% QoQ a quarter earlier. The preliminary GDP estimate confirms that the domestic economy continued its recovery, and that significant downward revisions to forecasts for 2024 may prove premature. One source of surprise may have been the better-than-expected health of the services sector.

Economic growth in Poland gains momentum

GDP, %QoQ SA

Full data on the second quarter GDP composition is not yet available (the CSO will report it on August 29), but we estimate that economic growth was based on rising consumption (private and public). This should come in alongside a continuation of the YoY decline in investment and negative contributions from foreign trade and inventory changes.

The beginning of the third quarter of this year brought a series of weaker-than-expected news from the global economy. The European economy is still unable to post a clear economic rebound, German industry is reporting weak results, and the situation in China grows increasingly precarious. The better-than-expected second quarter Polish GDP result provides some comfort and we're therefore maintaining our economic growth forecast for the whole of 2024 at 3.0% – even if the third quarter turns out to be slightly weaker than earlier forecasts. The biggest concern for the second half of the year is the outlook for both exports and investment.

Core inflation on the rise, no room for NBP cuts in 2024

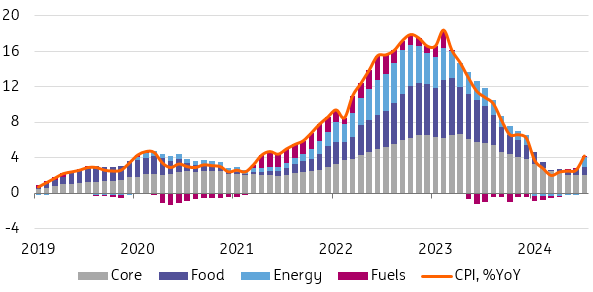

The CSO also confirmed its preliminary estimate of July inflation at 4.2% YoY, up from 2.6% YoY in June. Goods prices rose 3.5% YoY and service prices rose 6.2% YoY, compared to 1.3% and 6.1% a month earlier. The detailed data confirmed that essentially all of the increase in the annual CPI inflation rate in July compared to June was driven by increases in energy prices following the withdrawal of the energy shield. Prices of energy carriers rose 10.1% month-on-month in July, with electricity prices up 19.9% MoM, natural gas prices up 16.8% MoM and small increases in solid fuel and central heating prices.

Food and non-alcoholic beverage prices rose 3.2% YoY in July, following a 2.5% YoY increase in June. Fuel prices grew 1.2% YoY, following a 1.6% YoY rise a month earlier. We estimate that the core inflation (excluding food and energy prices) rose to 3.7-3.8% YoY in July from 3.6% YoY in June. We also note the high monthly price increase in the "recreation and culture" category (2.1% MoM), primarily related to rapid growth in the price of travel services (especially foreign tours).

Inflation up on higher energy prices

CPI, %YoY, prerc. points.

We expect CPI inflation to remain around 4.0-4.5% YoY until the end of 2024, which will not allow the MPC to ease monetary policy – especially as the economy remains on a recovery path. Much uncertainty surrounds the inflation outlook for the first half of 2025, as the government's plans for any further shielding measures on energy prices for households are unknown. We forecast that the second half of next year will bring a sharp decline in inflation, with the cycle of interest rate cuts beginning in the second quarter and continuing into 2026. Rates could be cut by a total of 75bp in 2025 and another 50bp in 2026.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap