Cheaper fuel helps consumption rebound in Poland

Poland’s retail sales have fallen less than expected as lower prices boosted gasoline sales. The underlying trend is also positive as the improvement is driven by recovering real disposable household income amid double-digit wage growth and falling inflation. Consumption is expected to be the main driver of economic growth in 2024

September retail sales surprised to the upside on strong fuel sales

Retail sales were only 0.3% lower in September than a year ago (ING and consensus: -2.0% YoY), following a 2.7% YoY decline the previous month. Seasonally adjusted sales went up by a fourth consecutive month in MoM terms - this time by a hefty 2.2%. This was boosted by, among other things, a solid increase in fuel sales linked to a favourable reference base and lower prices, which encouraged local drivers and also people from neighbouring countries to fill up.

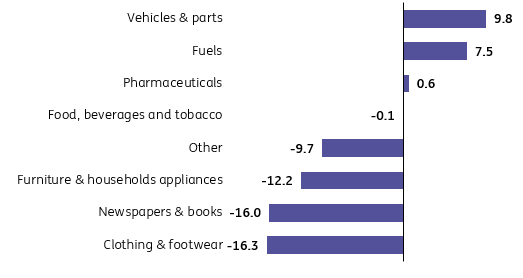

Car sales are recovering as well (+9.8% YoY). At the other extreme, clothing and footwear sales fell sharply (-16.3% YoY), largely thanks to warmer weather delaying new autumnwear sales. Last year, the influx of Ukrainian refuges also probably supported clothing demand.

Sales were boosted by strong fuel purchases amid lower prices

Structure of real retail sales in September, % YoY

Improving household disposable income is driving the consumption rebound

Double-digit wage increases have been accompanied by falling inflation, resulting in a recovery of households' real purchasing power. We expect this trend to continue, which should support a rebound in private consumption in the fourth quarter after a year of declines. In fact, consumption should be the main driver of growth acceleration in 2024.

This implies a return to an inflationary GDP structure. This is why it is so important to support domestic enterprise investments, which have been underperforming for many years, and to unlock RRF (the EU's Recovery and Resilience Facility) funds and 'pent-up' Foreign Direct Investment so a sustainable GDP structure can be restored thus boosting economic potential.

A brighter growth outlook ahead but its composition is set to turn pro-inflationary

We now have an almost full set of September data from the real economy; on Monday, the StatOffice will publish data on construction output. On that basis, we can assess the overall economic situation in the third quarter of this year. We estimate that GDP grew by around 0.4% YoY, following a decline in the first half of 2023. In the GDP composition, we expect a smaller decline in household consumption, slower investment growth, a less negative impact of any change in inventories and a less supportive role of net exports. The preliminary estimate of 3Q23 GDP will be released on 14 November. On Monday, we'll get the revised quarterly GDP data for 2022-23.

We are sticking to our forecast for GDP growth in 2023 at 0.4%. In 2024, we expect an acceleration to 2.5%. Should the new government reach a swift agreement with Brussels and be able to unlock the RRF funds and obtain payment of some of the delayed tranches, there is a growing chance for higher economic growth in 2024-25.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap