National Bank of Poland forced to amend hawkish stance amid lower inflation

Polish headline inflation in the first quarter was lower than expected and below the National Bank of Poland's (NBP's) projection. With an improving outlook, the NBP must adjust its hawkish stance to align with current conditions before initiating the first rate cut in the easing cycle. We expect rates to remain steady in April, with a potential cut in July

Inflation plateaued in the first quarter

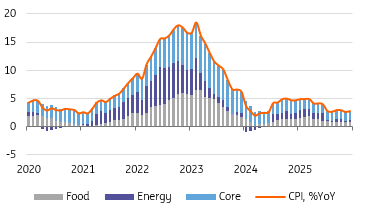

CPI inflation stood at 4.9% year-on-year in March, i.e. the same level as in January and February. This was lower than expected, with the ING and market consensus at 5.0%, but the range of forecast was wide between 4.8-5.2%YoY. The broadly expected peak in headline inflation was much lower than previously feared. The annual review of the inflation basket resulted in a revision of January CPI by -0.4 percentage points. Core inflation, which was stubbornly elevated, also started to moderate, and in March most likely fell to 3.4-3.5%YoY.

Consumer inflation to decline substantially in 2H25

CPI and its composition, %YoY

Price outlook has improved

The beginning of 2025 brought lower inflation, and the outlook for the rest of the year has improved as well. Headline inflation may return to the band of acceptable deviations from the target (2.5% +/- 1 percentage point) in July, a year earlier than projected in the March NBP forecast.

The projection was formulated before the revision of CPI weights and was based on the assumption that energy prices will bounce back in the fourth quarter of the year, which we think is unlikely.

In the first quarter of 2025, CPI inflation averaged 4.9%YoY vs. 5.4%YoY which was projected by the NBP in March. According to our estimates, core inflation was 0.4 percentage points lower than the central bank expected. Slowing wage growth has improved the core inflation outlook for the rest of 2025. What's more, the new Energy Regulatory Office (URE) electricity tariffs, expected in June, are likely to be lower than the current rates. At the same time, the government maintains it will extend the maximum price of PLN500/MWh into the fourth quarter if needed.

We expect inflation to moderate throughout 2025 as the statistical base becomes more favourable. Inflation should decline in April following the government's restoration of VAT on food in April 2024. A further decline is expected in July due to the partial unfreezing of energy prices in July 2024, which had previously increased energy costs. Our updated forecasts point to inflation running at 3% in 2H25, and average CPI this year may turn out close to the 2024 level, but with a downward rather than upward trajectory.

Hawkish NBP governor at odds with improving inflation outlook and more dovish MPC members

NBP governor Adam Glapiński has presented a hawkish bias in recent months, referencing various inflationary risks, but some are unlikely to materialise. Regulatory price updates do not seem to pose a threat to CPI in 2H25, and core inflation, to our surprise, is trending downwards (around 3.4-3.5%YoY in March), whereas the central bank staff projected it to stay around 4% by the end of the year. Wage growth has also moderated to a single-digit pace and surprised to the downside recently.

Inflation data and an improving price outlook have resulted in a change of mood within the MPC that is increasingly at odds with the hawkish Glapiński, as policymakers become more dovish. In their public statements, seven out of 10 rate-setters talk about possible rate cuts in 2025.

Easing cycle drawing nearer

In the face of an improving inflation outlook, discussions about the optimal moment for beginning the monetary easing cycle within the MPC will intensify. While we do not rule out that a motion to cut rates might be put forward this Wednesday, we do not expect it to garner enough support to pass.

Still, inflation is clearly on a lower path than in the March NBP projection and the July projection should reflect this. The start of the rate cut cycle is approaching, with the first cut expected in July and potential for a 100bp reduction in Polish rates by the end of 2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap