More fertile ground for monetary easing in Poland

The National Bank of Poland has maintained its hawkish policy stance but data from the beginning of 2025 suggests the conditions for monetary easing are starting to emerge. Headline and core inflation surprised to the downside and wage growth continued to moderate after three years of double-digit growth. We see room for 100bp of cuts this year

Act 1: High inflation path in March NBP projection and hawkish policy stance

The MPC has kept rates unchanged at 5.75%, and the central bank governor devoted almost the entire press conference to the upside risks to inflation, stressing the expected bounceback in electricity prices in the fourth quarter, persistently high core inflation, high wage growth, the expected economic recovery, and loose fiscal policy. According to the March NBP staff projection, headline inflation is projected to be 4.9% in 4Q25, assuming no change in interest rates. Governor Adam Glapinski suggested that rate cuts are not imminent, however policymakers are prepared to debate the timing of future policy easing.

Act 2: CPI inflation surprises on the downside amid annual basket update

The first cracks in the pessimistic inflation scenario, as presented by the NBP governor, appeared when the StatOffice published the February CPI report. This also brought an annual update of CPI weightings which reduced the January inflation reading by 0.4 percentage points vs. the preliminary estimate. Meanwhile, annual price growth was unchanged at 4.9% year-on-year in February. This means that the starting point for the NBP's projection was already too high. What's more, core inflation excluding food and energy prices moderated to 3.6% YoY in February from 3.7% YoY in January and 4.0% YoY in December last year, whereas the NBP saw it running around 4% by the end of this year.

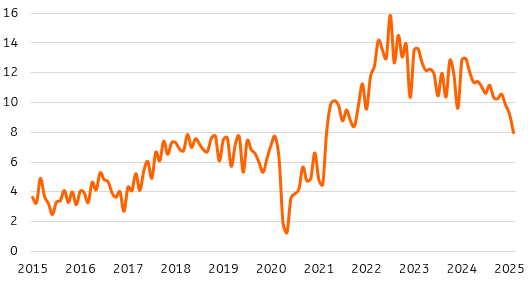

Act 3: Wage growth continues to slow in early 2025

The labour market data provided more arguments for a less hawkish policy stance and mitigated the main driver of sticky core inflation. Wage growth in enterprises slowed to 7.9% YoY in February from 9.2% YoY in January and double-digit levels in 2024. Employment remains in decline. A lower increase in the minimum wage this year, less generous hikes in the public sector, and lower indexation (as the period of exceptionally high inflation has passed) all contributed to easing wage pressure. On top of that, enterprises are feeling pressure from rising labour costs and have thinner margins so are less eager to hike wages.

Wages growth moderating at the beginning of 2025

Average wage in enterprises, %YoY

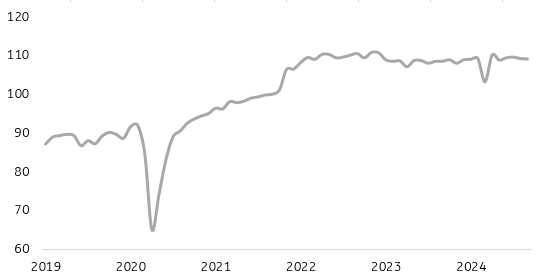

Act 4: Soft start to the year in economic activity

Industrial output continues to fall and construction production was stagnant in annual terms in February, reflecting subdued housing market activity, with Poland facing the highest mortgage costs in Europe. In February, industrial production fell by 2% YoY compared to -0.9% YoY in January. The decline is partly due to the difference in working days, but other factors are also at play. While there is a revival in global industry, it has not extended to Germany or our region. The beginning of the year has not shown a continuation of the revival seen at the end of 2024. In this cycle, Polish manufacturing relies on domestic demand (consumption and public investment), but with exports still weak, the cyclical rebound of Polish industry will be slow. In February, sectors reflecting the state of domestic demand were unable to lift total production into positive territory. The seasonally adjusted index of output declined by 0.2% month-on-month.

Construction production was stagnant In February (0% YoY vs +4.3% YoY in January). Housing construction resumed after a one-off rebound in January, but the oversupply of dwellings is growing. A positive signal is the continued revival of public investments, as shown by the moderate growth in infrastructure construction (1.7% YoY vs. 1.6% in the previous month) and specialised works (3.0% YoY vs. 3.9%). In the first category, we should see stronger growth from spring onwards due to the increased disbursements of EU funds. Overall, the upward threats from economic recovery and wages to inflation are probably smaller than perceived by the NBP.

Industrial production still stagnant

Industrial output, 2021=100, SA

Market perception and monetary outlook

Market participants are reluctant to take the March inflation projection and hawkish central bank stance at face value. The inflation path is likely to be more favourable than envisaged in the March inflation report. First, inflation at the beginning of 2025 was lower than expected. Second, the NBP projects the current Energy Regulatory Office (URE) electricity tariff of PLN623/MWh to increase when the cap (maximum price) of PLN500/MWh expires at the end of 2025, which is unlikely. Investors are aware that energy distributors are obliged to submit new tariff motions by the end of April, and given that wholesale forwards for electricity continue to run below PLN500/MWh, the new tariffs will be lower and may be close to the expiring price cap. In other words, electricity bills are unlikely to increase in 4Q25 and headline CPI at the end of this year may be close to 3.5% rather than close to 5% as projected by the NBP.

In our view, financial markets are correctly pricing in monetary easing in 2025. The July NBP projection may bring substantial downward revisions to the inflation path, taking into account a lower starting point and new electricity tariffs. Along with lower pressure from wage growth, this means there is room for monetary easing this year. An increasing number of MPC members will likely abandon the hawkish narrative of the NBP governor and join the more dovish camp. We see room for 100bp of cuts in rates this year, starting in the second half of this year. But a discussion on policy easing within the Council will likely start earlier, and some policymakers may even propose rate cuts before July.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap