Manufacturing and construction slowdown puts the focus on US services

The ISM manufacturing index is still indicating a contracting sector with the key new orders and production components remaining in the doldrums. Construction activity is also cooling meaning that growth in the second half of this year is going to have to be provided by the services sector

ISM suggests manufacturing continues to contract

The US ISM manufacturing index has risen to 47.2 in August from 46.8. It is a touch weaker than the 47.5 figure predicted with the disappointment concentrated in the new orders and production components. New orders slipped to 44.6 from 47.4 while production deteriorated to 44.8 from 45.9. Remember that anything below 50 is a contraction and the further below 50 the steeper the contraction.

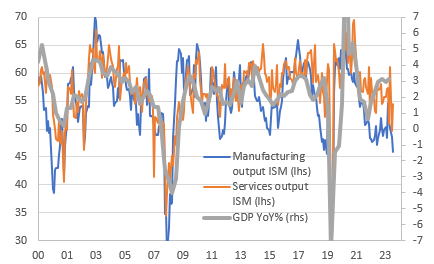

Additionally, there is a worrying narrowing of the pockets of strength. Just 22% of industry is experiencing rising orders and just 17% are seeing rising production. Historically, this weakness in output and orders points to a sharp slowing in GDP growth as the chart below shows.

ISM output balances and GDP growth

The reason for the increase in the headline index – which merely indicates a less steep pace of contraction for the sector – was that the backlog of orders rose a touch and employment improved from 43.3 from 46.0, but again, this is just saying that workforces are shrinking at a slower pace. Some in the market may be wary about the rise in prices paid to 54.0 from 52.9, but the trend is still cooling and it remains below its 6M average of 55.5. As such this report remains fully consistent with an ongoing series of meaningful interest rate cuts from the Federal Reserve.

Construction is cooling too

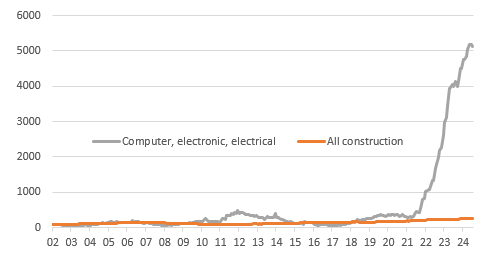

Separately, construction spending fell 0.3% rather than rise 0.1% month-on-month as predicted. There were some significant revisions, including a 0.3pp upgrade to June from -0.3% MoM to 0.0%, but the trend is certainly softening. The outlook for residential construction is not great given the weakness seen in home builders sentiment as a lack of affordability continues to constrain demand. Meanwhile, there appears to be a notable cooling in non-residential construction with two consecutive negative monthly prints. Importantly, the report hints that the support from the inflation Reduction Act is waning quite noticeably with the huge surge in construction activity tied to semi-conductor manufacturing seemingly starting to subside. So with manufacturing languishing and construction cooling, there is going to be an increasingly reliance on the service sector to provide economic growth.

Construction spending levels Jan 2002 = 100

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap