South Korean manufacturing jumps on frontloading ahead tariffs

South Korean industrial production rose in March as export activity was brought forward to beat tariffs. But service activity, retail sales and investment point to sluggish demand, weighed by domestic political turmoil. Yet even as trade-war headwinds rush Asia’s way, domestic growth is likely to rebound as political events stabilise

| 2.9% |

Industrial Production (%MoM, sa)5.3% YoY |

| Higher than expected | |

All industry production rose for a second month, but consumption and investment remain weak

South Korean industrial production rose 0.9% month on month, seasonally adjusted, in March, following a 1.0% gain in February, as exporters continued to front-run tariffs. Strong manufacturing (3.2%) and public administration (4.5%) activities led the gains, while increases were partly offset by the decline of services (-0.3%) and construction (-2.7%). In addition, retail sales and facility investment contracted in March.

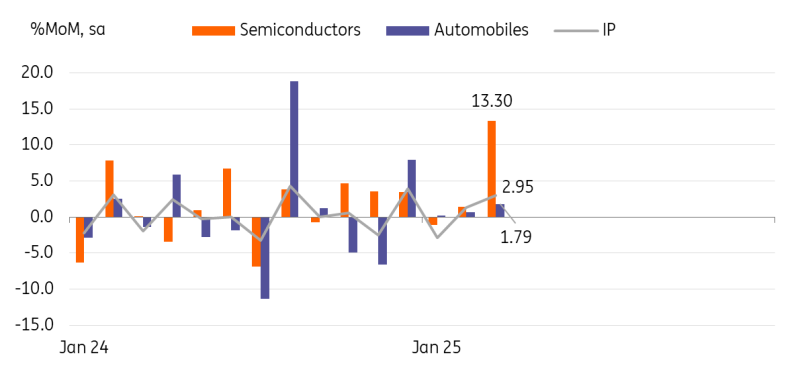

Semiconductors and cars output rose in March

Mining and manufacturing IP advanced a stronger-than-expected 2.9% MoM (a revised 1.4% in February, 0.3% market consensus)

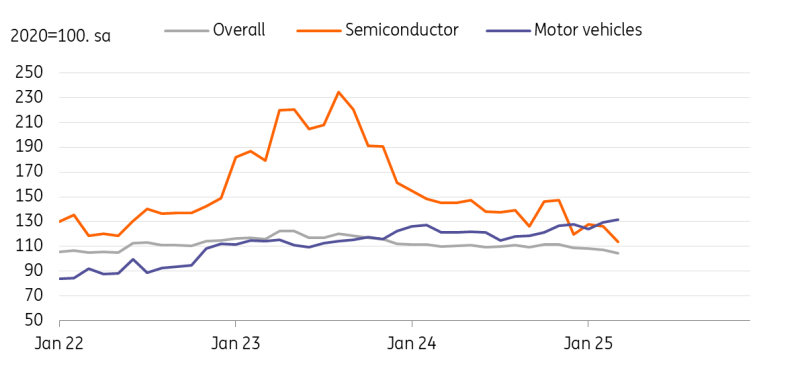

The most notable gains were semiconductors (13.3%) and pharmaceuticals (11.8%). Overall information technology (IT) output was strong, with electronics (7.8%) and computers (7.2%) posting gains. Transportation equipment rose, too, with cars up 1.8% and other transportation up 9.4%. We believe that strong demand for higher-end chips continues as they were exempted from tariffs. Auto output gained in March partly due to front-run 25% tariffs.

Shipments increased in March by 0.7%, but at a slower pace than the previous month’s 5.1%. Notably, export shipments rose 2.8% in March, following an 8.6% jump in February. This shows front-loading peaked in February and has since slowed down. Domestic shipments dropped 0.8% in March, suggesting sluggish demand. As shipments rose faster than production, inventories dropped 5.0%. Inventory levels show a quite significant downshift in the first quarter of 2025.

Inventory was down for semiconductors while up for cars

Services activity declined in March as weakness spread across the board

Main private service activities, such as wholesale and retail sales (-3.5%), financial activities (-2.1%), and real estate (-2.3%) dropped. Meanwhile, healthcare and social welfare activity gained 3.4% thanks to the government’s welfare programme. Despite the wildfires in the southern province at the end of March, leisure-related services -- such as eating out and recreation -- improved. Thus, the impact might’ve been locally limited. We believe that service activity is likely to recover in the second quarter. But consumer sentiment remains weak, limiting the expected rebound.

Retail sales dropped 0.3% MoM in March

The largest drop was durable goods consumption, which fell 8.6%. Auto sales were down 5.3%, following a sharp 13.6% rise in February. We believe that the government's tax incentive programme is creating monthly volatility in car sales. Meanwhile, semi-durable goods and consumer goods rose 2.7% and 2.8%, respectively.

Investment contracted in March, particularly in construction

Facility investment fell 0.9% MoM, sa, following a 21.3% gain in February. Despite the monthly drop, we still believe facility investment is on the recovery path. In a three-month-over-three-month comparison, facility investment contracted 1.9% 3Mo3M, sa, a smaller contraction than January's 3.5%. Capital goods imports have gained robustly recently. This suggests solid investment ahead in semiconductor and transportation. Also, forward-looking machinery orders accelerated to 12.0% 3Mo3M, sa, from 6.2% in January. This suggests a recovery of equipment investment in the near term.

However, the construction sector will remain a drag for overall growth. Construction dropped 2.7% MoM, sa, with civil engineering and residential building construction down by 6.0% and 1.5%, respectively. Forward-looking orders also dropped 32.4%. In the three-month comparison, the contraction deepened to 24.6% 3Mo3M sa from -3.0% in January. We believe that ongoing efforts to revitalise construction and the drag from a sluggish housing market in the non-Seoul area will continue at least until 2Q25.

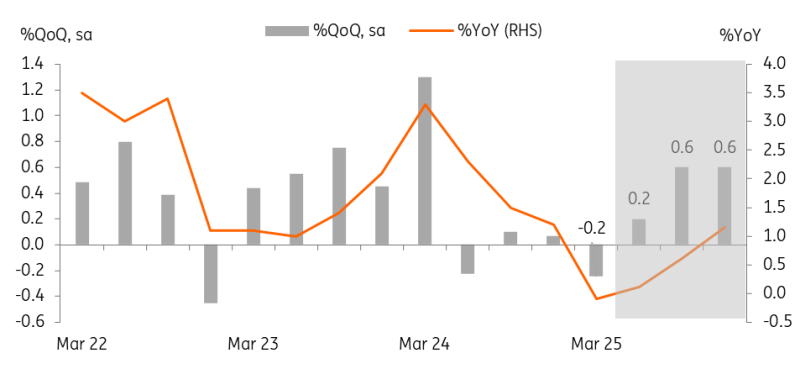

GDP is expected to rebound in 2Q25, but only marginally

Since first-quarter GDP is already known, today's better-than-expected IP data shouldn't be market-moving news. We don’t expect another contraction in the second quarter, but a sizable risk of recession remains.

Looking forward, we expect domestic demand to pick up gradually in 2Q25 as political uncertainty has eased considerably. Also, policy support will become more effective from 2Q25 onwards. Services and facility investments should rebound, even as construction will drag down overall domestic growth. Also, headwinds from weak external demand are likely to weigh on exports. But even if tariff threats peak in April, this won't trigger a sudden rebound in exports in the short term.

GDP is likely to rebound in 2Q25 thanks to recovery in services and facility investment

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap