July brings a surplus in the Hungarian budget

The overall fiscal position has improved slightly in Hungary with a surplus in July. However, economic activity remains weak and this poses an upside risk to the 4.5% deficit target. We’re maintaining our call for an end-year deficit in the range of 4.5-5.0% of GDP

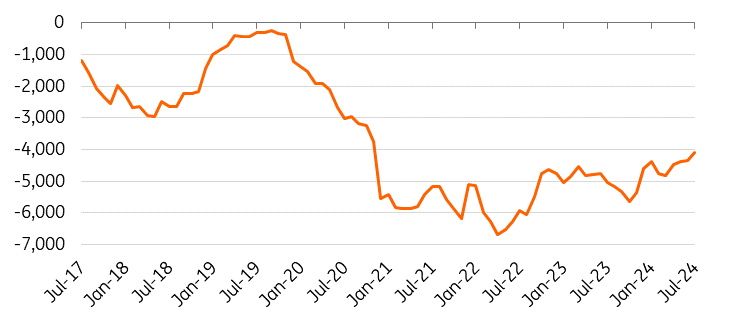

The monthly budget surplus was HUF213bn in July, bringing the year-to-date general government cash flow deficit to HUF2.44tr. This means that the shortfall sits at 61% of the Government Debt Management Agency’s planned financing needs for 2024. July’s surplus was the second highest monthly surplus we’ve seen for the seventh month in 22 years, which is a great positive development. Speaking of positives, what is even more encouraging is that for the first time since 2021, the 12-month rolling cash flow based budget deficit got within shooting distance of HUF4tr.

The 12-month cumulative cash flow budget deficit (HUFbn)

The Ministry of Finance's statement provided even less information than usual on the specifics of the deficit structure. As usual, interest expenditure was once again highlighted as a key ingredient in budgetary developments with an outflow of HUF2.2tr in coupon payments YTD. Based on our calculation, this means that coupon payments amounted to around HUF207.5bn in July, almost the same size as in June. With the overwhelming majority of retail bond coupon payments to households due in the first seven months of the year, we believe that the pressure on the expenditure side from this particular item is going to ease in the coming months.

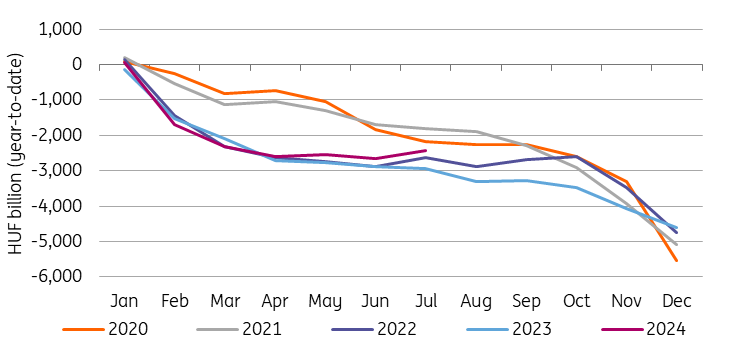

Budget performance (year-to-date, HUFbn)

The official statement indicates that the Ministry attributed the July surplus to government measures taken this year, improving the room for fiscal manoeuvre by around HUF1,000bn. This estimate is probably the approximate result of the HUF675bn investment postponement announced in April, combined with the recent HUF400bn tax increases announced in July.

New measures taken by the government to help cover slippage risk, but…

We have long argued that there is a slippage risk in the 2024 budget, which we have previously calculated at around 0.0-0.5ppt of GDP. However, with the recent government measures, our calculated slippage risk for 2024 could be covered. Nevertheless, the recent disappointing GDP data for the second quarter signals that economic activity remains weak, posing a downside risk to the inflow of indirect tax revenues – the main pillar on which the budget’s revenue side rests.

As we lowered our GDP forecast by 0.7ppt to 1.5% for 2024 as a whole, we maintain our call that the 2024 deficit will be between 4.5–5.0% of GDP, with a preference for the higher end given the government's recent track record. As the 2026 election approaches, we believe the government will seek to use any fiscal space to implement new spending programmes to boost consumption, hence our call for the current range to be maintained.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap