Japan’s 3Q21 GDP succumbs to covid restrictions

Like many other countries in Asia, Japan's latest GDP data demonstrate that Covid is still exerting a strong influence on the economy. Economic activity contracted sharply in 3Q21 as a result of emergency restrictions imposed on movement. These measures are now mostly lifted, and 4Q21 should bounce back.

| -0.8 |

3Q21 GDPQoQ% |

| Lower than expected | |

Heavy declines in domestic demand

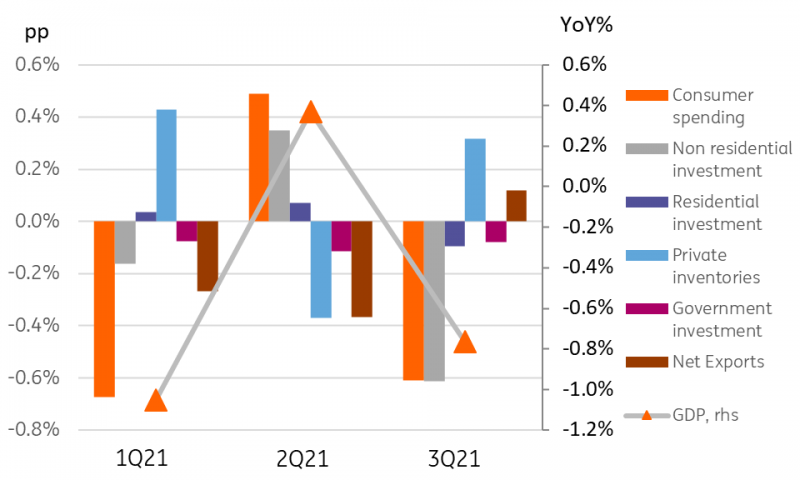

Emergency movement restrictions ahead of and during the Summer Olympics wreaked considerable damage to Japan's economic activity in the third quarter. Overall GDP declined by 0.8%QoQ, dragged down by a 1.1%QoQ contraction in consumer spending and a 3.8% contraction in non-residential business investment. Residential investment didn't fare much better, declining by 2.6% from the previous quarter. Government consumer spending provided a small boost to growth, but government investment was also affected by the emergency restrictions. Despite dismal domestic demand, imports rose more than 5% QoQ, though some of that fed into inventories, which provides about a 0.3pp boost to the quarterly growth rate. Net exports had no impact on the overall growth figure.

The chart below shows the volatile contribution to quarter-on-quarter growth from the main components over the last three quarters.

Contributions to QoQ GDP growth (pp)

4Q21 should bounce back

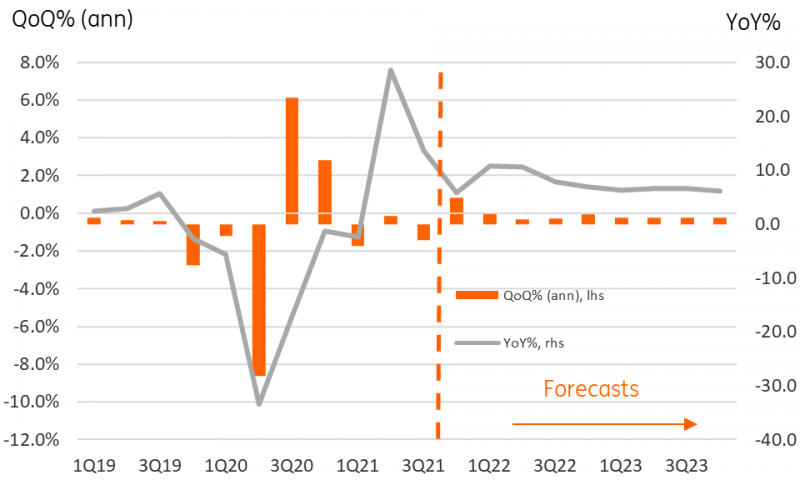

The only good thing you can say about the 3Q21 figures is that we know exactly where they came from - and the emergency restrictions that led to the contraction have now mostly been lifted, which should allow for a solid bounce back in 4Q21.

There is also some fiscal stimulus in the pipeline, which although it will probably not come in time to lift 4Q21 GDP, could provide some support to the 2022 growth profile. We have already made some provisional adjustments to our 2022 forecasts to incorporate this, though we are assuming that the stimulus impact will be substantially less than the headline JPY40tr figure. The fiscal measures include Covid relief spending, business support, childcare and education vouchers as well as cash handouts. but there will likely be some double-counting and inclusion of soft-loan and allowance figures which have a habit of being undrawn and are in any case, not "no-strings" support.

Incorporating these latest GDP figures, and making some preliminary adjustments for the forthcoming stimulus measures, leaves our GDP forecast for 2021 at 1.8%, and 1.7% for 2022. We don't see any notable change in Bank of Japan policy over the coming year.

Japanese GDP growth and forecasts

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap