Japan: Hotter than expected inflation, output rebound should support the BoJ’s policy normalization

Today’s data were a mixed bag, but the Bank of Japan will pay more attention to the sharp rise in Tokyo’s inflation

| 2.6% |

Tokyo consumer prices%YoY |

| Higher than expected | |

Sharp rise in inflation should catch the eye of the Bank of Japan.

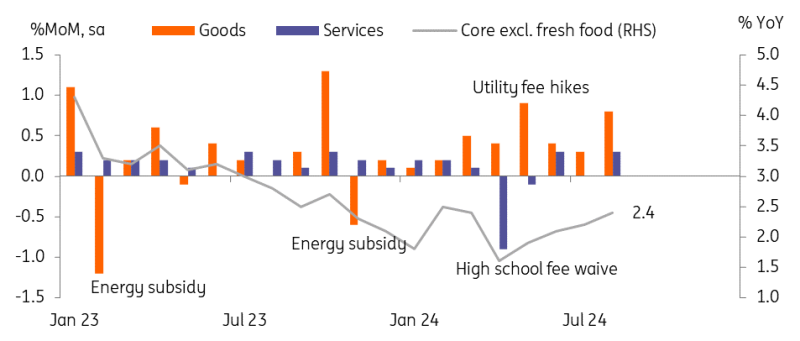

Tokyo consumer prices rose more than expected to 2.6% YoY (vs 2.2% in July, 2.3% market consensus). Fresh food and utilities rose the most by 8.1% and 15.9% respectively. Service prices also showed modest gains, and core inflation excluding fresh food rose unexpectedly to 2.4% (vs 2.2 % in July and market consensus). Utility prices rose more than expected mainly due to a high base related to the government subsidy programme, though other key prices such as household goods (5.7%) and entertainment (5.7%) also continued to rise. On a monthly comparison, inflation jumped 0.6% MoM sa in July, the fourth consecutive monthly rise. Goods prices increased 0.8% MoM while services prices rose 0.3%.

Utility prices push up Tokyo inflation more than expected in July

| 2.8% |

Industrial Production% MoM, sa |

| Lower than expected | |

Industrial production rose 2.8% MoM sa in July (vs -4.2% in June, 3.5% market consensus)

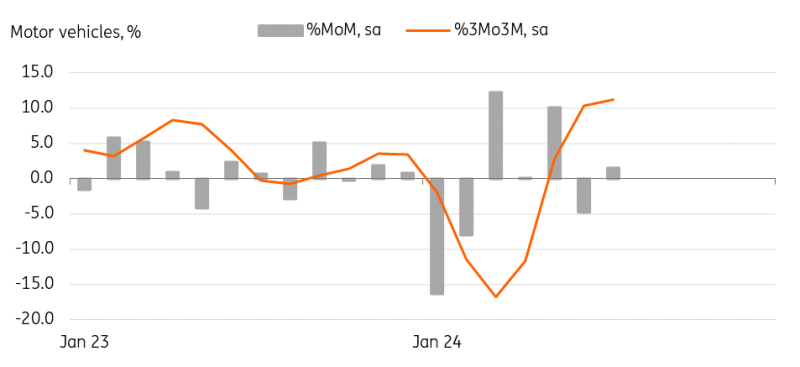

The rebound in industrial production was weaker than expected, but we still think the economy is moving in the right direction as production gains were broadly based. The monthly volatility was mainly driven by auto production. Auto production increased 1.5% MoM sa in July after a big drop of -4.8% in June. A major car company continues to keep some production lines shut down for a second month due to a safety scandal issue, so the recovery is still quite gradual. However, solid output gains in semiconductor-making machinery (25.3%) continued on the back of strong global chip demand. Other major sectors such as steel (1.8%) and petrochemicals (9.4%) recorded strong gains. With optimistic business surveys and normalization of auto production, we expect healthy 3Q24 GDP growth.

Retail sales rose a less-than-expected 0.2% MoM sa in July (vs 0.6% in June, 0.4% market consensus), but have risen now for four consecutive months. Motor vehicle sales (5.6%) have risen for three months, and household machines (5.5%) also rebounded solidly.

However, labour market data was a disappointment. The unemployment rate unexpectedly rose to 2.7% in July (vs 2.5% in June and market consensus) but the job-to-application ratio edged up. We continue to believe that labour market conditions remain healthy.

Auto production hasn't recovered fully from safety scandal issues

BoJ watch: October hike probability increased but we maintain our base case for December for now

We believe that upcoming data on wages and household consumption will be in line with the BoJ’s projections and that the BoJ will adjust its policy accordingly. Market opinions for additional rate hikes are spread sometime between October and January. While it's true that today's inflation is raising alarms about an October hike, we are sticking to our December hike call as the base case for the following reasons.

- The upside surprise to inflation mainly came from utility prices, and we expect inflation to subside over the next few months as the government temporarily reintroduces relief on utility bills over the summer.

- The recent JPY appreciation should ease the BoJ’s concerns that rising import prices could push up domestic inflation higher than expected.

- Having experienced market turmoil earlier this month, the BoJ will monitor financial market conditions more closely than in the past. The US Fed’s policy meeting in September and its impact on global financial markets are still uncertain. Thus, the BoJ may wait a few months after the Fed’s first rate cut.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap