Japan avoids a technical recession, but GDP disappoints

Japan's fourth quarter GDP was revised up to avoid a technical recession, and yet it still missed market expectations. We believe sluggish private consumption should remain a concern for the BoJ in order to change its policy direction. We therefore see a higher chance of a policy change in April than in March

| 0.1% |

4Q23 GDP%QoQ, sa |

| Lower than expected | |

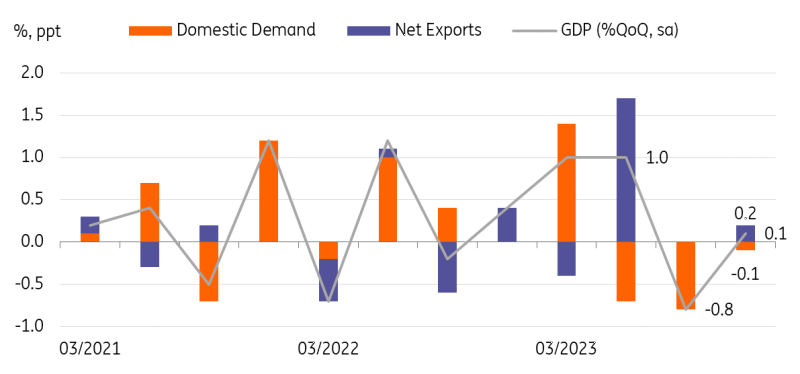

Strong exports and non-residential investment led the fourth quarter growth

Japan’s fourth quarter GDP for 2023 was revised up to 0.1% quarter-on-quarter seasonally adjusted from the preliminary -0.1%. So, the country avoided a technical recession, but today’s reading was weaker than the market consensus of 0.3%. As suggested by earlier capital spending data, solid non-residential investment growth of 2.0% was the main driver behind the rebound (vs -0.1% preliminary, 2.4% market consensus). But private consumption remained sluggish, contracting by 0.3% (vs 0.2% preliminary and market consensus), a key reason for the modest growth. Exports rose 2.6%, mainly due to strong services exports (11.3%) related to one-off royalty income.

Looking ahead, we expect the economy to expand in the first quarter of this year. Exports should remain a key driver of growth. Solid vehicles, IT equipment, and falling commodity prices should allow for a higher positive contribution of net exports to growth. Domestic demand should improve, partially supported by government spending. With inflation decelerating and supported by another year of solid wage growth, private consumption is also expected to pick up. Investment is expected to remain positive on the back of strong corporate profits.

Weak domestic demand continued

The repricing of rate-hike bets has been particularly aggressive since last week

We believe there are two reasons for this rapid change in market sentiment: i) the data releases have been positive in supporting the Bank of Japan's policy change in the near future, and ii) the preliminary Shunto results will be out this week, just before the BoJ’s March meeting – and Rengo, the Japanese Trade Union Confederation, said that its member unions demanded an average wage growth of 5.85% at this year’s Spring Wage Negotiations (vs 4.5% last year’s demand). This is the highest seen in 30 years. We don’t think the proposed rate will be agreed upon, but certainly, this year’s wage growth is expected to exceed last year’s 3.6% rise. We think 4-4.5% growth is possible.

As for the data releases, we had argued that the BoJ wouldn’t be in a hurry to raise rates as long as the economy was in a recession. As fourth-quarter GDP is revised up, one of the major hurdles is cleared, and this may give the BoJ more confidence to move. January’s cash earnings result was also stronger than expected. This is why we have changed our forecast for a BoJ rate hike from June to April.

A higher chance of rate hike and ending NIRP in April

However, private spending-related data was on the weak side. Household spending data was disappointing, with a higher-than-expected decline of -6.3 % year-on-year in January, suggesting that wage growth couldn’t keep up with higher inflation and consumer purchasing power. As mentioned earlier, private consumption growth in the fourth quarter of last year contracted for three consecutive quarters. The market does not seem to be paying much attention to weak private consumption, but we believe it is a key concern for the BoJ and could be a reason for its patience. We continue to believe that April has a slightly higher chance of seeing a rate hike than March.

What to expect in the near future

We expect to see a change in forward guidance in the statement at the March meeting and possibly an end to the yield curve control policy. We are also watching closely to see how the government view of the growth and inflation has changed. This will be likely revealed in its monthly economic report. Ending NIRP will require some kind of policy coordination or agreement between the government and the BoJ, so the central bank won’t rush into a rate hike or ending NIRP in March.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap