ISM services rebound, but continue to track weaker than official US data

The disconnect between very strong official economic data, such as non-farm payrolls and GDP growth, and third party private data sources remains very wide. Today's ISM services report did improve after December weakness, but is at a level consistent with GDP growth closer to 1% than 3% and payrolls rising perhaps 50,000, not 350,000

ISM services rebounds, but contradictions with official data continue

The ISM services index has bounced back nicely in January with the headline index at 53.4 versus 50.5 in December. The consensus was 52.0 with anything above 50 equating to expansion and anything below 50 being a contraction.

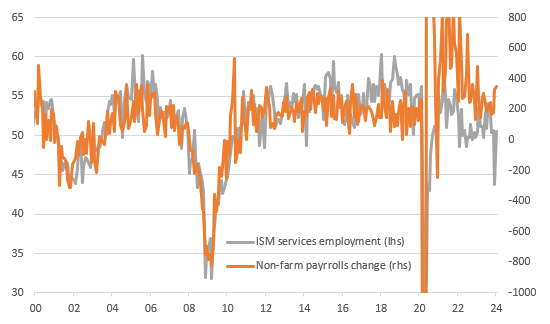

The most interesting aspect is the employment component. Remember that last month it plunged to 43.8, indicating a deep contraction in hiring, which completely contradicted the strength in non-farm payrolls that was initially reported as a 216k increase that was then revised higher last Friday to 333k. The ISM employment index has now rebounded to 50.5, but this is only indicating very modest hiring and leaves the index in line with its 6M average. It is fine, but certainly not consistent with two consecutive months of 300k+ payrolls.

Services ISM employment component versus non-farm payrolls change (000s)

They will eventually converge, not no sign of it yet

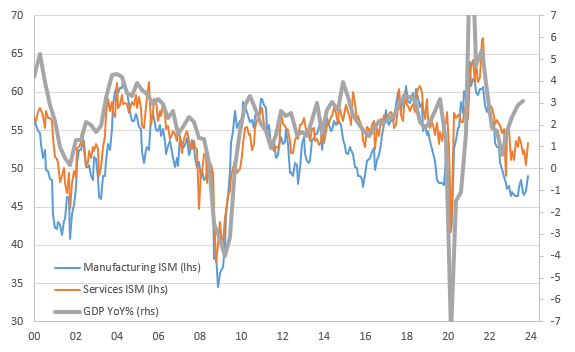

New orders were better, rising to 55.0 from 52.8, while business activity held at 55.8, but again both are only broadly in line with 6M averages. As with the employment component, the headline manufacturing and services ISM indices paint a weaker picture than official data. GDP rose 3.1% year-on-year in the fourth quarter, but as the chart below shows, the ISM's are at levels historically consistent with GDP growth closer to 1%. These ISM’s have been going for decades and we had assumed we would soon start to see a convergence between upbeat official economic data and more cautious private sector data. No sign of that happening yet though…

ISM Manufacturing and Service headline indices versus GDP growth (YoY%)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap