Inflation still falling in Turkey despite recent FX moves

Annual inflation dropped in June amid a better-than-expected monthly reading but the downtrend since October seems to be coming to an end

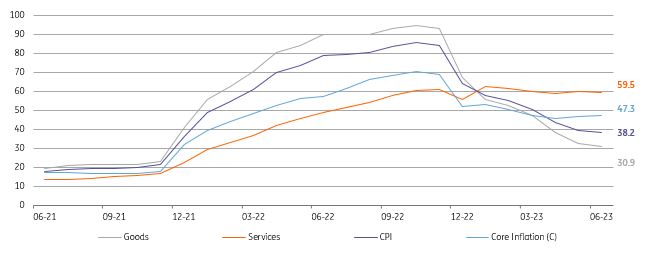

With the better-than-expected June figure of 3.92% month-on-month (vs the consensus at 4.84%), annual inflation continued to fall, dropping to 38.2% from 39.6% a month ago. This continuation of the downtrend last month was attributable to lower price increases in non-food groups compared to last year, despite recent exchange rate developments and the continuing impact of buoyant domestic demand. With the June data, cumulative inflation in the first half of this year reached 19.8% (vs the 22.3% full-year forecast from the Central Bank of Turkey in its April inflation report). Given this backdrop, we will likely see a revision to the CBT's forecast following the release of the new inflation report at the end of this month.

Core inflation (CPI-C) came in at 3.84% MoM or 47.3% on an annual basis. While the exchange rate and commodity price-driven improvements in core inflation indicators helped to keep a lid on inflation expectations for some time, the pass-through effect from recent currency weakness has now started to impact the inflation outlook again. In June, durable goods prices rose by 6.6% MoM, while core goods inflation accelerated to 36.7% year-on-year. Accordingly, the underlying trend (as measured by the three-month moving average, annualised percentage change, based on the seasonally-adjusted series) for the headline rate markedly increased in comparison to the previous month due to goods inflation along with continuing pressure in services, which has kept the trend in this group elevated given the continuing pressures in rent and catering services.

After mild PPI readings in recent months, we saw an acceleration to 6.5% MoM reflecting the impact of exchange rate volatility, though annual inflation slightly dropped to 40.4% due to large base effects. The data implies that cost pressures have started to gain strength again and will likely continue in the near term given recent minimum wage adjustments and the hike in civil servant salaries.

Inflation outlook (%)

In the breakdown of the main expenditure groups, transportation was the major contributor to the headline rate, at 1.19ppt, on the back of FX-driven effects. This group was followed by food at 0.83ppt thanks to unprocessed food, particularly fresh fruit and vegetables, despite moderating inflation in processed food. Among other segments, catering (reflecting cost-related pressures), housing (sensitive to the exchange rate and domestic demand) and alcoholic beverages & tobacco (due to price hikes in cigarettes) were other drivers pulling the headline up by 35bp to 40bp.

Despite strengthening underlying momentum, goods inflation moderated to 30.9% YoY thanks to base effects while annual inflation in services recorded a 59.45% YoY increase, close to the peak of the current inflation series as it was significantly affected by domestic demand and hence accelerated significantly due to rents, and restaurants and hotels.

Annual inflation in expenditure groups

In sum, the downtrend in inflation since last October seems to have come to an end. We will likely see an increase in the headline rate ahead given the FX pass-through from recent lira weakness, as well as the continuing strength in demand conditions which is allowing companies to pass on their cost increases to consumers. Potential adjustments in administered prices could also boost overall inflation. On the policy front, the equilibrium point in exchange rates and interest rates has yet to be seen given signs of a gradual policy approach which implies that a pivot to more conventional policies will take time. Going forward, market participants will be focusing on the government’s new Medium-Term Program which is reported to be announced in September. In this regard, the normalisation process and related policy moves will also be closely followed in the near term.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap