- Quick take

- 30 January

- Hungary

Hungary’s GDP growth disappoints and we’re cutting our 2026 forecast

Economic growth in the final quarter of last year came in lower than expected. Ramped up government spending hasn't made a meaningful contribution to the economy's overall performance. We are still hoping for significant growth this year, but downside risks are growing, and we now cut our 2026 growth forecast to 1.9% from 2.3%

| 0.2% |

GDP growth in 4Q(QoQ, swda) ING forecast 0.7% / Previous 0.0% |

| Worse than expected | |

Although expectations were not particularly high, the latest GDP data failed to deliver any positive surprises. In the fourth quarter of 2025, the Hungarian economy grew by just 0.2% quarter-on-quarter. Prior to the release of the data, the overall picture was mixed based on the available high-frequency data, but a strong performance in December could have led to a more favourable outcome. While economic activity saw improvement rather than stagnation, the zigzag pattern continued: a stronger quarter was followed by a weaker one, and vice versa. This time, we experienced the downside. In contrast, several of the economies covered by my colleagues surprised to the upside (e.g. eurozone, Germany, Netherlands, Spain, Italy), leaving Hungary as a clear underperformer.

Hungarian GDP growth

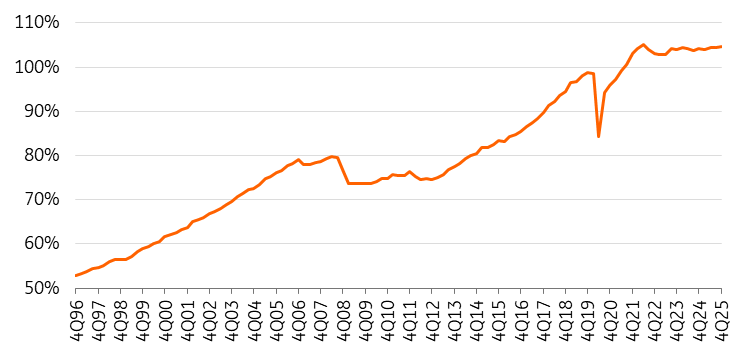

Based on seasonally and calendar-adjusted data, the year-on-year growth rate of the Hungarian economy slowed in the fourth quarter compared to the third quarter, which was not expected by many. While the raw data does show some acceleration, this is due to the effect of more working days. Nevertheless, the unadjusted annual growth rate of 0.7% is hardly explosive. Overall, the average GDP growth rate for 2025 was 0.4%, which was well below the initial projection at the start of the year, and worse than the performance in 2024. Consequently, Hungary has remained in the no-growth zone.

Real GDP in Hungary (2021 = 100%)

As usual, the Hungarian Central Statistical Office (HCSO) provided few details about the underlying drivers in its flash report. As expected, the services sector boosted the performance of the Hungarian economy, while the construction industry also contributed positively to the overall performance, despite enjoying only one exceptionally good month during the fourth quarter. In contrast, declining industrial activity held back economic activity, suggesting that industrial performance in December may also have been disappointing. We had expected agriculture to perform well at the end of the year, but the HCSO did not mention this sector at all in its report, suggesting that the expected improvement probably did not materialise.

The factors behind the economy's generally weak performance will be highlighted in the second estimate, due on 3 March. Regarding the drivers based on the final use of GDP, we believe that consumption was the main force in the fourth quarter once again. This was partially offset by the continued negative contribution of investments and net exports.

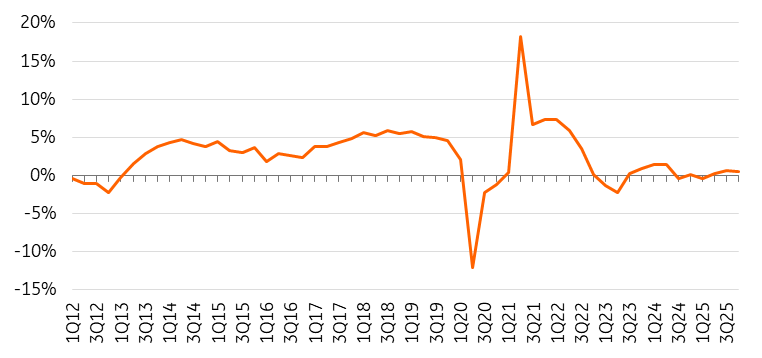

The quarterly annualised growth rate of Hungarian real GDP

In light of the fourth quarter data, we are revising our 2026 Hungarian GDP growth forecast downward. Slower-than-expected growth in the fourth quarter means the carry-over effect will also be weaker this year, at just 0.3%. In other words, if the economy were to stagnate in each quarter of this year, total economic growth in 2026 would be only 0.3%. However, government intervention is much more likely to generate intra-year growth, particularly in the first quarter, meaning that full-year GDP growth will realistically exceed the carry-over effect. Nevertheless, we are revising our previous forecast of 2.3% to an average of 1.9% in 2026.

Consumption may be the driving force this year, primarily due to new fiscal stimuli. However, this has yet to stimulate economic growth. The biggest question remains how much of the surplus income will enter the real economy and how much expanding consumption will generate imports, which would partially offset the positive effects of consumption. We do not expect any significant changes to investment. In a favourable scenario, investment activity could stop declining and grow by between 0 and 1%. Meanwhile, strong import demand driven by consumption, coupled with some recovery in investment and weak external demand, suggests that net exports will negatively impact economic growth this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more