Hungarian inflation remains higher than expected in April

Hungary's headline and core inflation both slowed in April, but the overall picture isn't exactly encouraging. This month's data fully reflects the impact of the price curbs, yet price changes have caused an upside surprise. The repricing that we are trying to avoid now through interventions will come back later, only stronger

| 4.2% |

Headline inflation (YoY)ING estimate 3.5% / Previous 4.7% |

| Higher than expected | |

Weaker than expected slowdown in headline inflation rate in April

Hungary's average price level increased by 0.2% in April compared to March, according to the latest data from the Hungarian Central Statistical Office (HCSO). Consequently, the year-on-year inflation rate fell to 4.2%. However, the slowdown in the pace of price increases was weaker than expected; it was essentially more of an unpleasant surprise. Analysts had almost unanimously expected a significant slowdown, with the inflation rate perhaps falling to 3.5–3.6%.

Of course, there was an unusually high degree of uncertainty surrounding these forecasts. This is mainly because inflation is driven not by a structural process, but by one-off factors and interventions.

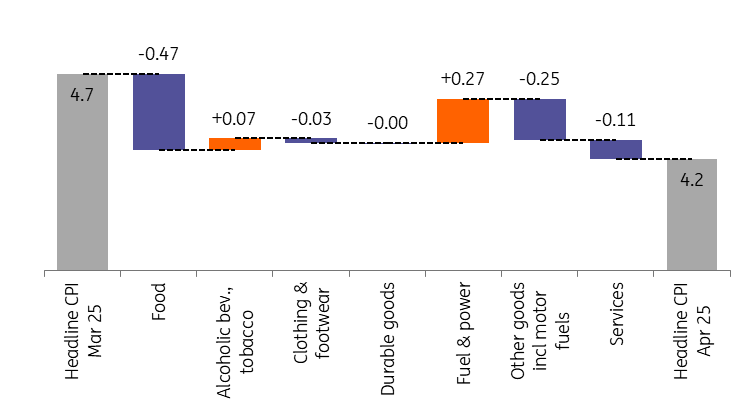

Main drivers of the change in headline CPI (%)

The details

- The introduction of price curbs on 30 major food categories from mid-March is a one-off factor. Its anti-inflationary impact was evident to a small extent in March, but was fully reflected in the April indicator. In food prices, the decline over one month was only 1.3%. In turn, this item alone essentially explains the decline in the headline inflation indicator. However, it's interesting to note that prices for non-regulated food items generally rose significantly in April.

- The other significant and predictable factor contributing to the low monthly inflation rate was the development of fuel prices. Here, the HCSO recorded a 1.4% month-on-month fall, due to the slump in global commodity prices and the weakening dollar.

- There are two important items to add to the list of unpleasant surprises and inflationary factors. Firstly, the price of tobacco products rose sharply by 2.4% on a monthly basis. Secondly, the monthly inflation rate for household energy of almost 4% was a significant surprise. As the heating season drew to a close, residents saw a considerable increase in their full-year energy bills, with inflation being particularly drastic for piped gas at 8.3% MoM.

- The spring months are typically marked by one-off, regular annual price increases in financial services and telecom services, which are broadly in line with the previous year's inflation. However, at the government's request, the companies concerned have now 'voluntarily' withdrawn the previously announced price increases and postponed them until the middle of next year (i.e., until after the general election). Statistically, however, the price increases in the telecommunications sector have still occurred, presumably temporarily.

- The increase in domestic holiday services was more pronounced than usual in spring, as was the sharp rise in air fares. These trends probably reflect the increased demand during April, which had many long weekends.

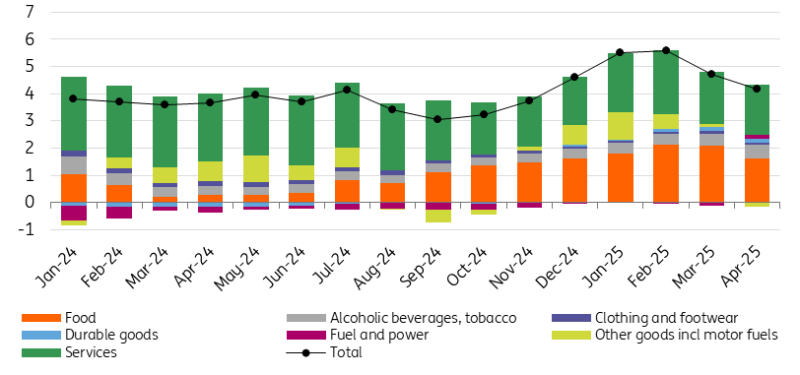

The composition of headline inflation (ppt)

Underlying inflation improving, but measures pose risk to consumer confidence

So, the 0.5ppt decline in the annual rate of inflation was due to a slowdown in the rates for food and fuel, offset by increases in other non-core items such as tobacco and household energy. Accordingly, the core inflation indicator – capturing the underlying inflationary developments – has fallen to 5.0% on an annual basis, after easing by 0.7ppt versus March, reflecting the impact of a negligible monthly price change and the high base.

Overall, the official statistical indicators have moved in a favourable direction. However, the main question remains as to how this will affect perceived inflation and inflation expectations among households and businesses. So far, the central bank has said that not much has changed, with inflation expectations generally remaining elevated.

Following the announcement of the new margin freeze measure on 30 household goods items from mid-May, there is a greater chance that households' inflation expectations will begin to moderate. Still, too much intervention could have the unintended side-effect of causing consumer uncertainty. In other words, consumers may interpret these measures as a sign that the problem is so serious that more is needed to keep inflation under control. Meanwhile, rising prices in other areas (e.g., household energy, tobacco and food not subject to price controls) may reinforce this perception and encourage households to exercise greater caution.

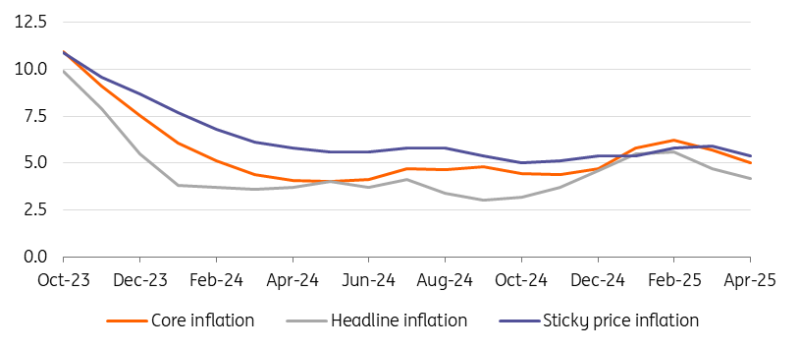

Headline and underlying inflation measures (% YoY)

Inflation is a double-edged sword, because what goes around comes around

Looking ahead, inflation is expected to remain at around 4% in the coming months. This suggests that government interventions will create a semblance of price stability in the near future. However, the problem is that this relative stability is not the result of underlying economic processes, meaning a new wave of inflation could arrive when the measures are withdrawn and/or are kept in place for too long. In other words, inflation being suppressed now will re-emerge later, meaning we will pay for today's lower inflation rate with higher inflation in the future. This could permanently keep the pace of price increases above the central bank's target, which could be harmful in the longer term as it will become embedded in the expectations of economic actors.

In light of April's inflation data, we expect inflation rates to fluctuate between 4.0% and 5.0% for the rest of the year. In 2025, we expect average annual inflation to be around 4.5%. For next year, we have revised our forecast upwards by 0.5ppt and now expect average inflation to be around 4.0% in 2026.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap