Food prices drive a higher-than-expected rise in Turkish inflation

The food group was once again the key driver behind Turkey’s rising inflation rate in November following a similar trend in October. Even so, the downtrend in the annual inflation rate has remained in place

Turkey's inflation rate came in at 2.2% in November, higher than the market consensus (1.9%) and our call of 1.8%. However, the annual figure has maintained its declining trend and fell to 47.1% from 48.6% a month ago as a result of favourable base effects (inflation stood at 3.3% in November 2023). Cumulative inflation reached 47.1% vs the Central Bank of Turkey's revised 44% forecast for the whole year.

PPI stood at 0.66% month-on-month, showing a drop to 29.5% year-on-year from the month prior, and this was driven by energy prices. While the data implies a notable weakening in cost pressures in the second half of this year – which is also attributable to supportive currency developments – global commodity prices, particularly oil prices given the current geopolitical backdrop, will likely remain the key determinant of the PPI trend in the coming period.

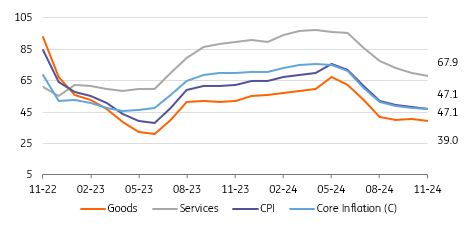

Core inflation (CPI-C) came in at 1.5% MoM, the lowest monthly reading since late 2021. It moved down to 47.1% on an annual basis, supported by the relatively slow-moving FX basket and increasingly benign PPI outlook. Going forward, pricing behaviour and inertia in services remain key risk factors for the pace of Turkey's disinflation process.

Inflation outlook (%)

Regarding the underlying trend, TurkStat will release seasonally adjusted (sa) headline CPI and core indicators tomorrow. An early analysis reveals that the underlying trend of inflation should maintain its gradual improvement in November driven by both goods and services. As an additional note, with the release of the latest inflation report, the CBT dropped its previous emphasis on an inflation path based on the quarterly average of monthly inflation rate (sa) as an indicator for a significant and sustained decline in inflation. However, according to new projections, the Governor sees the rate dropping below 1.5% MoM in seasonally adjusted terms in the third quarter of 2025, which implies a significant delay; this level was the call for the last quarter of 2024 previously. It's expected to decline further to slightly above 1% MoM in the fourth quarter of 2025.

In the breakdown:

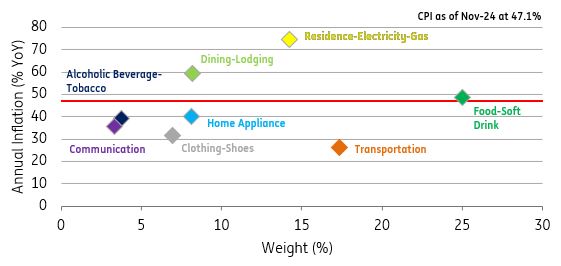

- The food group turned out to be the major contributor to the headline rate once again with 1.23 percentage points. Compared to the same month last year, unprocessed food inflation recorded a strong increase (9% vs 0.3% in 2023) with the highest November figure in the current inflation series, driving the upward move in food inflation. Processed food prices, on the other hand, showed a deceleration (1.6% vs 4.9% last year). Accordingly, monthly food inflation at 5.1% was one of the key factors contributing to a higher-than-expected increase in November.

- This was followed by housing, with a 0.4ppt contribution reflecting the continuing impact of rent increases. The pace of these increase has dropped, however. According to the MPC minutes, leading indicators suggest that monthly rent inflation will decelerate in December as well.

- Household equipment was the third largest contributor, pulling the headline rate up by 0.21ppt.

As a result, goods inflation inched down to 39.0% YoY, while core goods inflation – a better indicator for the trend – recorded a slight increase to 28.9% YoY. Services, which are less sensitive to currency movements but more heavily impacted by domestic demand and minimum wage increases, maintained their downtrend to 67.9% YoY with continuing signs of improvement.

Annual inflation in expenditure groups

Overall, the tightening in financial conditions and monetary policy has now started to contribute to the return to the disinflation path, and will likely continue in the period ahead. Last month, The CBT's communication suggested that we are nearing a gradual rate-cutting cycle, implying that a December move may be a real possibility. The revised guidance also tied rate cuts to both realised and expected inflation, suggesting that the central bank will closely watch ex-ante and ex-post real rates. Accordingly, we expect a 250bp cut from the bank this month – though we do not rule out a smaller move, especially given the higher-than-expected November figure signalling ongoing challenges to disinflation efforts.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap