Hungarian employment hits two-year low

Recent labour market trends suggest that the supply side is becoming increasingly restrictive in Hungary. Additionally, some companies are considering downsizing, which indicates that labour market tightness is easing and the bargaining power of employees is diminishing

| 4.4% |

Unemployment rate (Feb-Apr)ING Forecast 4.2% / Previous 4.3% |

| Higher than expected | |

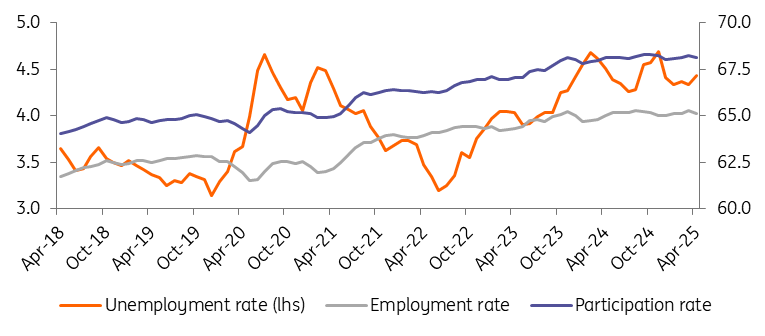

The latest labour market statistics from the Hungarian Central Statistical Office (HCSO) show a slightly worse picture than expected for April 2025. The model estimate shows the unemployment rate rising to 4.4%, rather than stagnating as expected by the market consensus. Meanwhile, the official three-month moving average survey rate moved in a similar direction, increasing by 0.1ppt. This puts the indicator at 4.4% for the February-April period. In terms of the number of unemployed people, the two statistics suggest the size of the group is around 215,000–217,000.

A closer look at the detailed data reveals that the number of people in employment fell by around 35,000 compared to the previous month. Around one-tenth of these people became unemployed, while the rest withdrew from the labour market; in other words, inactivity increased significantly. Accordingly, both the participation and employment rates declined significantly. This is, of course, only a one-month change, but official three-month moving average data reveals a similar trend.

Historical trends in the Hungarian labour market (%, 3-m moving average)

For the first time since the summer of 2023, the number of economically active people (e.g., labour market participation) fell below 4.9 million. This negative change is partly driven by people voluntarily leaving the labour market, but largely by population decline. Consequently, the supply constraint is becoming increasingly effective in the Hungarian labour market.

Employment is also now at its lowest level since spring 2023. The Hungarian economy has been stagnating since mid-2022, and this is slowly but surely starting to affect the labour market. Various confidence indices and company surveys increasingly suggest that companies are not planning to expand, and some are even considering downsizing. The outlook for growth is bleak, and the persistent lack of demand is prompting even those who have been hoarding labour to make redundancies.

Changes in the labour market since mid-2022 (mid-2022=0, '000)

For the time being, however, there does not seem to be a significant wave of layoffs. It appears closer to a trough, with the number of people in employment gradually and slowly reducing. This also suggests that labour market tensions are easing, which is clearly weakening workers' bargaining power. One factor contributing to this is that an increasing number of large companies are choosing to reduce their regular office presence. Most recently, the Mol Group announced that the home office would be abolished as of 1 July (moving from one home office day per week to zero). This may contribute to further job losses, particularly among those who have benefited greatly from this atypical form of employment, such as parents of young children.

Based on recent market rumours, it would not be surprising to see more and more firms follow suit, with unemployment rates slowly rising alongside weak economic performance. Of course, the unemployment rate could hover around 4.4–4.5% for the rest of the year due to seasonal work – but risks clearly point towards a further weakening of the labour market.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap