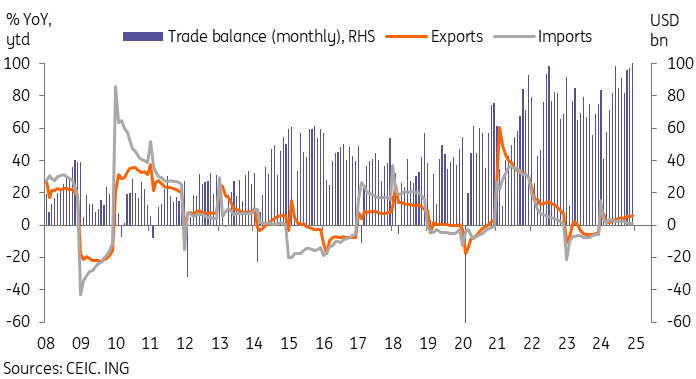

China’s trade surplus hit a record high in 2024

Solid export growth combined with sluggish import growth helped China's trade surplus reach a new high in 2024

| USD 992.2bn |

2024's trade surplus reached a new record high |

| Higher than expected | |

Exports end the year on a strong note

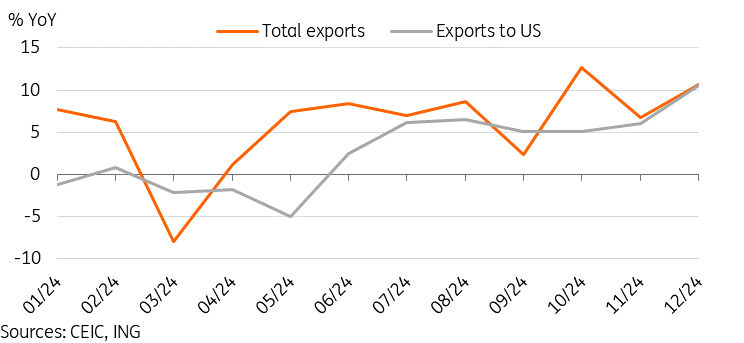

China's December export growth rebounded to 10.7% year-on-year from 6.7% YoY in November, beating consensus forecasts. December saw USD335.6bn of exports, bringing the full year exports to USD3.58tr, which was good for a 5.9% YoY growth rate and comfortably higher than what most economists were expecting at the start of last year.

December's data likely benefited from some export frontloading ahead of US President-elect Donald Trump's inauguration this month. Exports to the US rose 15.6% YoY in December, which marked a 30-month high, behind only exports to ASEAN (18.9%) in December. For 2024 as a whole, the fastest growth came from ASEAN (12.0%) and Latin America (13.0%), while exports to developed economies remained modest, with export growth to the US (4.9%), EU (3.0%), the UK (1.2%) and Japan (-3.5%) still sluggish.

In terms of export product, China's key winners of 2024 have been concentrated in several key sectors. Ships (57.3%), semiconductors (17.4%), autos (15.5%), and household appliances (14.1%) were key areas of strength on the year.

Data showed that there was noticeably stronger volume than value growth for some export categories in 2024, suggesting price competition remains heavy, and this will no doubt add fuel to the fire for those criticising China of "exporting deflation". The sectors where we can clearly see this are in auto, steel, and household appliances.

China's December exports were likely supported by frontloading demand

Import growth remained soft amid still sluggish domestic demand

Import growth was a comparably more modest 1.0% YoY, though this too was a recovery from November's -3.9% YoY level. December imports totalled USD230.8bn, bringing full-year imports to USD2.59tr. Imports grew a tepid 1.1% YoY in 2024.

China's import data shows a clear divide within the economy. Sectors benefiting from policy support were the only areas of strength in terms of import demand. Automatic data processing equipment imports surged 57.9% YoY, semiconductor imports rose 10.4% YoY, and hi-tech imports were up 10.7% YoY as China continued to commit heavy resources toward tech self-sufficiency and hi-tech development.

However, other import categories were quite soft. Commodities demand softened in 2024, with agricultural (-7.9%), iron ore (-2.5%), crude oil (-3.9%), lumber (-1.5%), and steel (-9.2%) all in negative growth for the year.

Imports also took a hit from a more cautious Chinese consumer. China's auto imports were down -16.7% YoY, as domestic producers dominated the market amid strong price and quality competitiveness and a general slowdown of luxury vehicle purchases. Cosmetics imports also saw a -9.0% YoY decline as consumers shifted to domestic alternatives.

China's consumption could see a modest recovery in 2025, depending on how effective policy support is, but it remains uncertain how much of this will translate into stronger import demand as policies look likely to benefit domestic producers more.

Trade balance reached new highs amid solid exports but sluggish imports

Annual trade surplus moved to a new record high in 2024

As a result, December's trade balance data ended the year on a positive note, with both the monthly (USD101.6bn) and annual data (USD992.2bn) marking new record highs. The monthly trade surplus cleared the 100bn barrier for the first time on record, though the annual trade surplus fell a little shy of reaching the USD1tr mark.

External demand has been an important contributor to growth momentum in 2024, not only through the record trade surplus but also the impact on manufacturing. However, with the looming prospect of increased tariffs and expectations for generally moderating global growth, external demand looks likely to soften in 2025. Our ING scenario currently has tariffs starting to take effect in the second quarter of this year, with tariffs on China potentially coming earlier.

While we are not as pessimistic as many in markets on the impact of tariffs on China's growth trajectory, it's likely that for China to be able to see stable growth in 2025, we will need to see the domestic demand side picking up the slack. All eyes remain on China's stimulus rollout.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap