China’s September credit activity beats forecasts

Credit growth remains in year-on-year contraction but recent rate cuts and other stimulus should encourage recovery in the months ahead

| RMB 3760bn |

China's September new aggregate financing |

September credit data beats expectations

China's credit data has been very weak for most of the year, and we attribute this to two factors. First, a lack of private sector investment has held back lending to non-financial corporates, while lower household borrowing demand has resulted from fewer new mortgages amid the property market slump and a decline in big-ticket purchases funded by consumer loans. Second, despite China’s relatively low nominal interest rates, real interest rates have remained too high for the current economic conditions.

It is still early days and there's a lot of progress to be made, but there is hope that the People's Bank of China's (PBoC's) monetary policy easing is at least starting to address the second half of the weak credit demand equation.

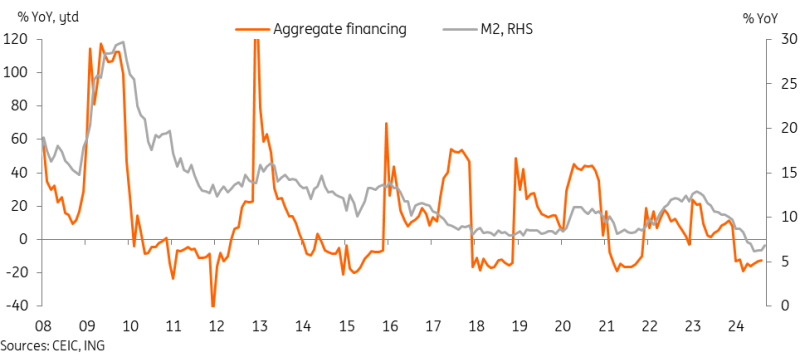

Aggregate financing grew by RMB 3760.4bn in September, which came in stronger than market forecasts. In the third quarter, aggregate financing fell by -3.0% year-on-year compared to last year. This was by far the smallest contraction of any quarter so far this year; first and second-quarter aggregate financing saw year-on-year growth levels of -12.0% and -24.4% respectively. In the year to date, aggregate financing is now down -12.6% YoY, which is certainly still a substantial decline but marked three consecutive months of a smaller contraction.

New RMB loans rose by RMB 1973.0 bn in September, which represented a -22.2% YoY decline for the month. Year-to-date, new RMB loans have fallen -21.2% YoY. After contracting at approximately the same pace as aggregate financing through the first five months of the year, we've seen RMB loans contract by more in the last few months, though this remains heavily skewed by July's contraction of new RMB loans. Trust loans and entrusted loans have fared relatively better in year-on-year terms over this period.

M2 growth also outperformed market expectations in September, up to 6.8% YoY from 6.3% in August. After flatlining at historical lows over the last few months, this uptick marked a four-month high for money supply growth, though this remains well short of historical levels.

With credit growth still in contraction, it remains too soon to declare a turnaround, but with the recent and upcoming stimulus policy rollout combined with the last few months of data, there are some encouraging signs that the worst of the credit decline could be over. At the very least, 2025 credit growth should look healthier. Combined with plans to recapitalise banks and expand the re-lending programme designed to facilitate bank lending to SOEs for real estate acquisition, there is some positive news for Chinese banks which have been facing notable challenges from narrowing net interest margins.

Aggregate financing and M2 growth both beat market expectations in September

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap