China: PBoC cuts rates amidst data weakness

The market was expecting the PBoC to wait until September before easing again, and today's cuts suggest that the authorities' concern about the state of the macroeconomy is mounting. But that doesn't mean that they are about to undertake unorthodox policy measures

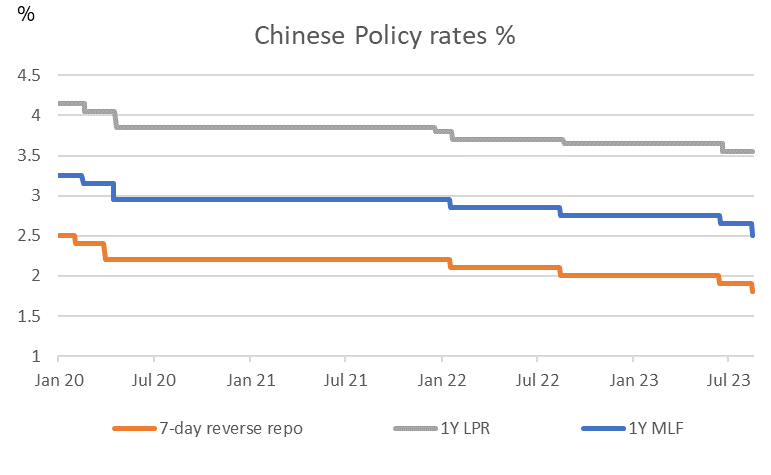

| 2.50% |

Medium term lending facility rateCut from 2.65% |

| Lower than expected | |

Chinese policy rates

Rate cuts show that concern is mounting

The 15bp cut to the medium-term lending facility (MLF) was unexpected. Almost all forecasters expected China's central bank, the PBoC, to wait until September to cut again. MLF lending volumes of CNY401bn were in line with expectations. The PBoC also cut the seven-day reverse repo rate by 10bp, which now stands at 1.8%.

The market responded abruptly. The CNY rose to close to 7.29 immediately after the decision, though eased lower soon after. And 10Y Chinese bond yields dropped about 6bp to 2.56%.

From a macro perspective, today's policy decisions are somewhat helpful. They will help improve the debt-service ability of cash-strapped local governments and property companies. But this isn't a game-changing outcome, and so we doubt that market sentiment will dramatically improve just on this.

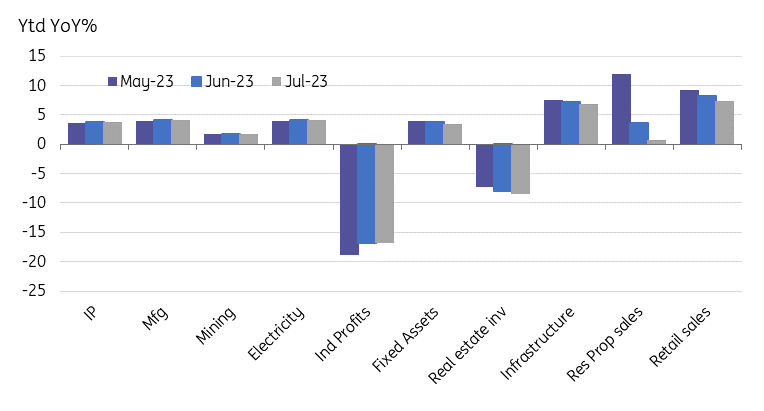

Activity data remains extremely poor

The activity data release contained no bright spots, and quite a few downside surprises. Perhaps the worst of these was the 2.5% YoY growth in retail sales. This has declined sharply from an admittedly base-effect inflated 18.4%YoY growth rate in April as the re-opening briefly led to a retail sales surge. Now the idea of a consumer-spending-led recovery is looking very vulnerable.

In year-on-year terms, industrial production slowed to 3.7% YoY, from 4.4% in June. Year-to-date, production growth remained at 3.8% for the second month.

Property investment slowed at a faster pace in July, falling at an 8.5%YoY pace, weaker than the 7.9% YoY decline achieved the previous month. Property sales growth also slowed to almost a standstill in July, rising at only 0.7% YoY YTD, down from 3.7% in June. And fixed asset investment slowed to 3.4% from 3.8% YoY YTD. Topping all of this off, the surveyed unemployment rate rose to 5.3%.

China activity summary

What does this mean for policy?

The question of the day based on the number of times it has been posed to this author is "Does this mean the PBoC will undertake Quantitative Easing (QE), and if so, when?"

At the current juncture, QE does not seem to be the right response to what we are seeing. Nor does a large dollop of fiscal stimulus.

China is undergoing a painful transition to a less debt-fuelled, less property-centric and more consumer-driven economy. An "emergency" policy like QE that primarily inflates real and financial asset prices does not appear to have a strong role to play here. QE would also put the CNY under further weakening pressure, which it is very clear the PBoC does not want and would make it much harder for them to manage the CNY. It would also raise the risks of capital outflows, which they will also be keen to avoid.

More policy measures will be needed and more will certainly be delivered. The PBoC has not ended the rate-cutting cycle yet, and there will be further iterations of policy rate cuts along the lines of what we have seen today.

As for government stimulus policies, these, we think, will tend to be along the lines of the many supply-side enhancing measures that we have already seen. The way through a debt overhang is not to print more debt, though it may be to swap it out for lower-rate central government debt, or longer maturity debt to ease debt service. Enhancing the efficiency of the private sector will also play a key role, though this and all the supply-side measures will take a considerable time to play out. The tiresome chorus clamouring for more stimulus is unlikely to stop in the meantime. And we will continue to see weak macro data for the foreseeable future. It is a necessary part of the adjustment and is far preferable to resurrecting the debt-fuelled property model that propelled growth previously. But we do need to lower our expectations for China's growth.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap