China’s manufacturing PMI continued to improve in September

China’s manufacturing purchasing managers’ index was generally encouraging, rebounding to a six-month high in September. Yet, the non-manufacturing PMI disappointed by falling back to neutral levels

| 49.8 |

China's NBS Manufacturing PMI |

| Higher than expected | |

Manufacturing PMI slightly beat forecasts in September

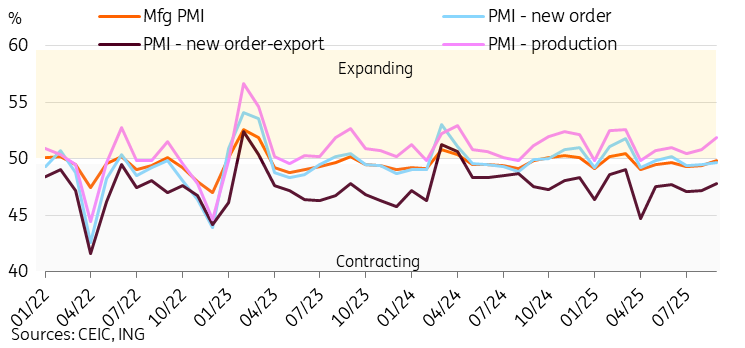

China's official manufacturing PMI was 49.8 in September, up from 49.4. The data from the National Bureau of Statistics was slightly stronger than forecasts for a smaller rebound, marking a 6-month high. Still, it remains in contraction territory for the sixth consecutive month.

Overall, the data breakdown is generally encouraging. Production increased to 51.9, also reaching a six-month high. New orders remained in contraction but edged up 0.2pp to 49.7. New export orders also rebounded to a six-month high of 47.8. Employment reached a seven-month high of 48.5.

Less encouraging was the ex-factory price slump to 48.2, which remained in contraction territory for the 16th consecutive month and hit a three-month low. It signals that “anti-involution” efforts against aggressive price competition have yet to have a significant impact on prices.

By company size, the recovery was mostly driven by large and small enterprises, which rose 0.3pp and 1.6pp, respectively, to 51.0 and 48.2 on the month. Medium-sized enterprises edged down 0.1pp to 48.8. Large enterprises have generally outperformed small and medium-sized enterprises since the start of the pandemic reopening.

Key components of the manufacturing PMI improved in September

Non-manufacturing PMI disappointed on the month

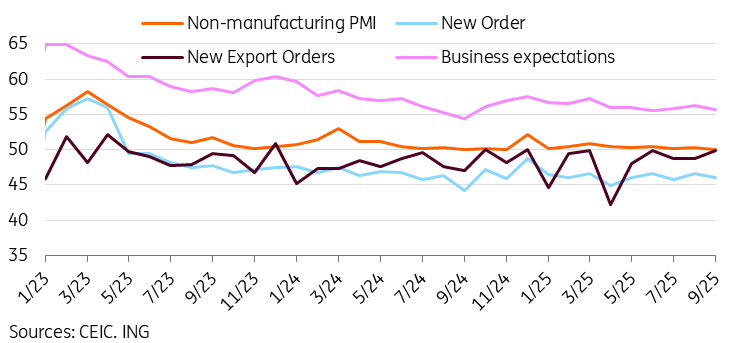

While the manufacturing PMI data offered some reason for optimism, the non-manufacturing PMI softened to the lowest level of the year at 50.0. The series has been at neutral or expansionary levels since the start of 2023. It has come dangerously close to falling into contraction a few times in 2024, and again in September.

New export orders were the lone silver lining in the non-manufacturing PMI data, edging up to match the year's peak at 49.8. Other categories were down across the board.

China's growth year-to-date has been supported by stronger-than-expected external demand, and this trend is likely to continue as a key driver for the remainder of the year. With that said, third-quarter economic activity and inflation data released to date suggest a strong case for further policy support in the coming months. We continue to expect one more 10bp rate cut and 50bp reserve-requirement ratio (RRR) cut before year-end.

Non-manufacturing PMI fell to the critical 50.0 threshold

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap