- Quick take

- 11 October 2019

- Canada

Canada: Confounding the doubters

A really strong jobs market suggests there is still plenty of life in the Canadian economy, despite recent disappointment on the activity front. This diminishes the prospect of near-term rate cuts, but “insurance” action is still likely from the Bank of Canada

A resilient jobs market

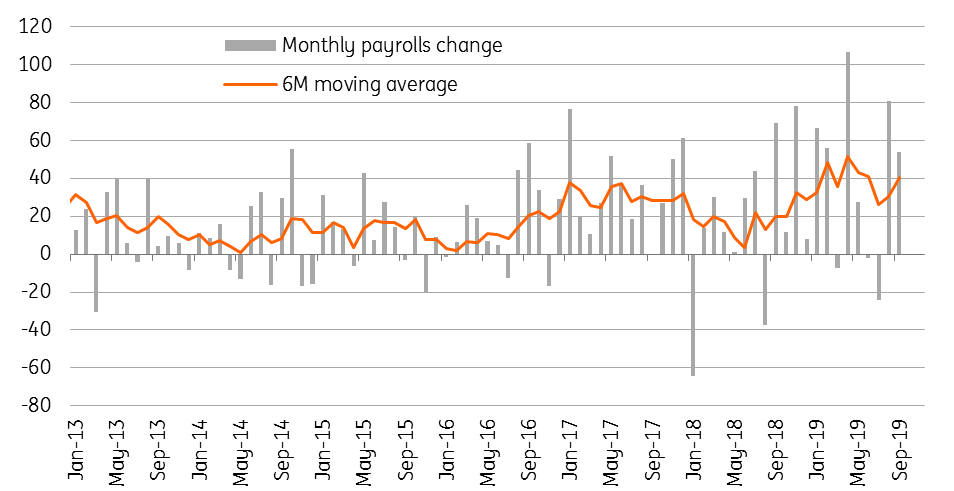

Given the uncertainty over trade and worries about global growth, the Canadian jobs market is proving to be more resilient than we had thought. After a subdued three months for employment growth between May and July, it bounced back sharply in August (81,100) with another 53,700 jobs created last month. As such the six-month moving average for job creation is moving higher again with full time jobs leading the charge, rising 70,000 in September. Year-to-date employment growth is at 358,100, the best figure for the first nine months of a year since 2002.

Canada monthly employment change

This outcome was well ahead of even the most optimistic forecast (the consensus was for a 7,500 gain overall), but there are caveats. It was entirely a public sector story (30,000 for healthcare, for example) for September. Private sector employment fell 21,000 with particular weakness in the goods producing sectors. This tallies with recent softness in some of the activity data and perhaps hints at weaker overall employment growth in coming months.

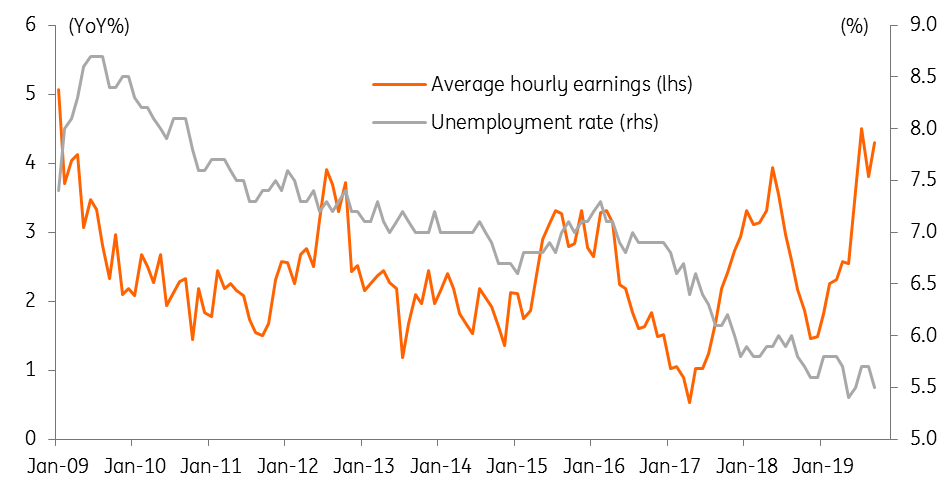

Nonetheless, with the unemployment rate dropping to 5.5%, which means there is a very small pool from which to find new employees and this is translating into robust wage growth. Wages are currently rising 4.3% year-on-year, which could be supportive for both consumer confidence and spending, at least in the near term.

Wage growth and unemployment confirm the strength

Where the US goes, Canada typically follows

For now, Canada looks to be in a relatively good position versus other major economies. Nonetheless, we question how long this can continue given global growth is weak and central banks elsewhere are gradually easing monetary policy. This could result in upward pressure on the Canadian dollar given its positive yield and hurt its international competitiveness.

We suspect that the Bank of Canada will end up following and cut interest rates fairly soon. After all, the domestic indicators on activity have become more “mixed” with July GDP showing unchanged activity and the IVEY purchasing managers’ index swinging sharply into negative territory.

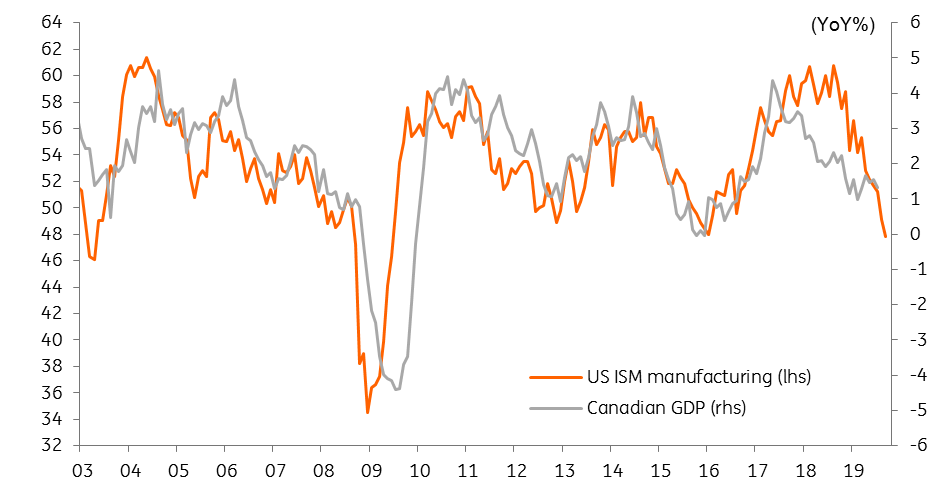

Moreover, the ISM index from the US is looking particularly foreboding as where this index goes the Canadian economy tends to quickly follow. After all, the Canadian economy is relatively open with trade accounting for more than 30% of economic activity versus little more than 10% for the US. Canada is also more dependent on commodities for a significant proportion of its output with mineral extraction and agriculture representing more than 10% of the economy. Recent price moves in energy don’t suggest a pick-up in investment in this sector is likely in the near term.

US ISM manufacturing index versus Canadian GDP (YoY%)

25 basis point cut still in the offing

For now the market is pricing just one rate cut over the next twelve months and we agree with that prognosis given the Bank of Canada didn’t raise interest rates as aggressively as the Federal Reserve over the past couple of years. However, we think the BoC rate cut will come sooner than September 2020 as futures contracts imply given the growth concerns, although our December 2019 prediction is looking a little shaky after today’s jobs numbers.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more