- Quick take

- 15 October 2018

- Romania

BriefING Romania

Challenging 10-year auction

EUR/RON

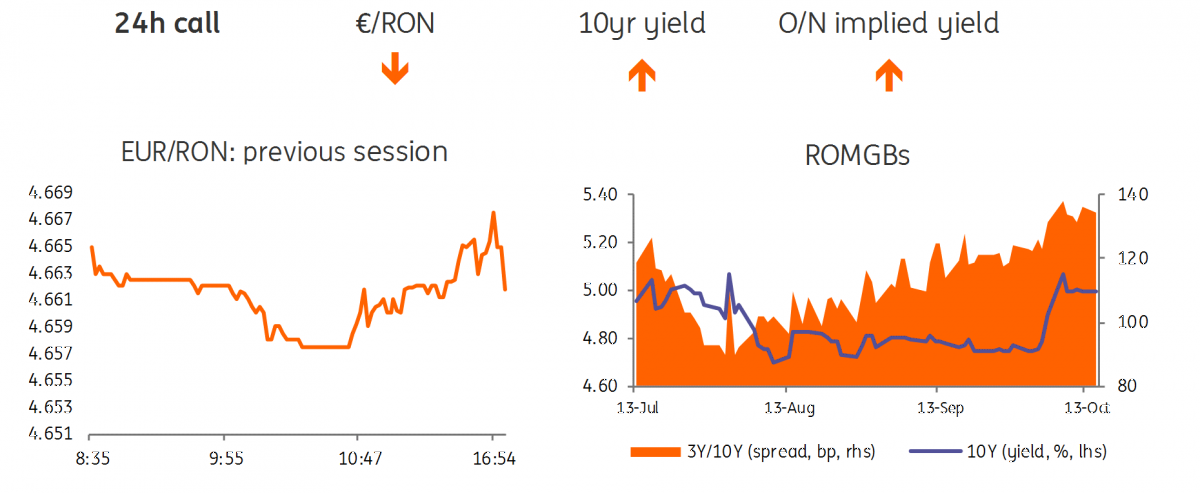

The EUR/RON tested below 4.6600 on Friday but failed to consolidate and closed the day around 4.6620 on average turnover. We see the pair maintaining the mild downside bias and eventually dip below the 4.6600 in the coming days, tracking peers, but still remaining fragile to risk sentiment.

However, the upside seems pretty much capped to 4.6700 for now as the central bank seems to stand ready to avoid any significant pass-through into inflation before the base effects bring the headline lower towards its target band. The central bank's deputy governor Liviu Voinea was cited by Bloomberg saying that “volatility on the global markets is the key risk for our monetary policy at the moment” given that “the biggest pass-through in inflation is from the exchange rate. It’s significantly higher in the short-term and medium-term than the nominal wage pass-through to inflation.”

Government bonds

Sluggish dynamics in the Romanian government bonds market as the curve closed flat despite the strong October 2020 auction in the previous day. Today the MinFin will face a challenging task to sell RON500 million in February 2029 bonds, the new 10-year benchmark.

Last month we had a rather long tail for this ISIN, at 4.98/5.03% average/cut-off yields with the initial RON 300million target being upsized to RON411 million. Meanwhile, the market shifted some 20bp higher while the MinFin has shown willingness to upsize any auction if there is a demand within a reasonable tail.

We expect moderate demand for today’s auction and look for an average yield within 5.20-5.25% depending on the MinFin's willingness to issue more. In the Bloomberg interview, the deputy governor added that the central banks is “in the tightening cycle - the number of hikes isn’t over” but “when this will happen - either this year or next - depends on evidence”. The overall tone of his interview was hawkish in our view.

Money Market

The money market implied yields traded flat as the minimum reserve heads into the second part of the maintenance period, offsetting to some extent the absence of NBR’s liquidity injections. These could be unnecessary for now, but starting with the next reserve period, rates might be under pressure again.

The week ahead

In the week ahead, we see US retail sales bouncing back strongly in September after a disappointing August for retailers. Due to hurricane Florence, there is the risk for some data volatility within the industrial production report, but again we see some upside to the market forecast of a 0.2% MoM gain. The Eurozone will be focused on the Italian budget proposal to the European Commission, and whether that will show any last minute changes that could indicate a softening of the stance on the Italian side. From a data perspective, the trade balance will be interesting to watch given the trade turmoil, especially after a significant slide in the balance in July.

With nothing notable on the domestic calendar, we see 4.6500-4.6700 range for the EUR/RON this week.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more