- Quick take

Benign UK inflation data reduces chance of June rate hike

- 10 hours ago

- United Kingdom

Yes, UK inflation is set to rise again later this year, having dipped below 3% in April. But the data should reassure the Bank of England that last year's food price spike hasn't triggered a wave of second-round effects across the inflation basket. Like yesterday's jobs numbers, the data questions the need for aggressive rate hikes

Today’s UK inflation data, like yesterday’s jobs numbers, questions the need for aggressive rate hikes. We continue to think markets are overestimating the Bank of England’s willingness to tighten policy, at current levels of energy prices. Investors are pricing between two and three rate rises by next spring.

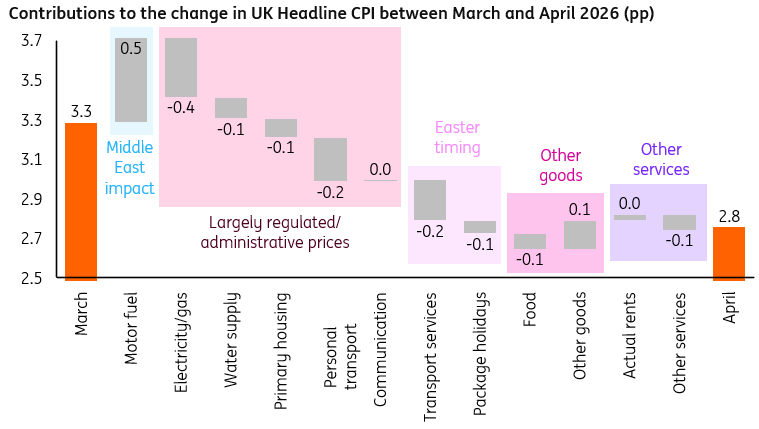

There’s nothing too surprising about the latest numbers, even if they came in a bit below consensus. Headline inflation fell from 3.3% to 2.8%. The Middle East impact is still really only showing through in petrol/diesel prices; that’s added 0.5pp extra to headline inflation compared to March. Regulated/administrative prices – including significantly lower water/sewerage bill increases, reduced policy costs on household energy bills, and no repeat of last year’s vehicle tax increase – have shaved 0.8pp off relative to March, by our maths. Travel components affected by the timing of Easter chopped three-tenths off headline inflation, too.

How UK inflation changed between March and April

Taken all together, we’re now expecting inflation to bounce around between 3.5-4% in the second half of the year, peaking briefly just below 4%. The next big shift comes in July, when the energy regulator Ofgem is due to update the quarterly household price cap. We’re looking for roughly a 12% increase, which is remarkably benign, all things considered. This is based on 6-12 month-ahead natural gas futures prices, which Ofgem uses as a proxy for hedging costs of the utility providers, and are within spitting distance of pre-war levels. If nothing changes, those futures prices point to an 8% fall in energy bills in October, though our commodities team is wary that wholesale costs could push higher as Europe increasingly competes with Asia for LNG cargoes. Food inflation is also likely to gradually build throughout the year.

All together, the fact that the latest data didn’t surprise on the upside – as April’s CPI numbers have tended to do in recent years – should in itself provide some comfort to the Bank of England. Lots of services prices are only updated once per year, in April. The fear of the hawks last year was that the rise in food inflation – a very visible trend to consumers – together with big payroll tax and minimum wage hikes, would manifest in a more persistent bout of inflation. So far, there’s not much evidence that’s happening.

That should provide some reassurance that the impending energy shock is unlikely to spark a wave of “second round effects”, or at least not nearly as pronounced as four years ago.

Currently, we think the Bank is somewhere between zero and one hike(s), with officials arguing that the mere fact they aren’t cutting rates (as was previously likely this year) amounts to de facto tightening.

That said, after April’s BoE meeting, we narrowly shifted our call for a prolonged hold to a one-and-done rate hike in June. That is now in serious doubt, though clearly a lot can still happen in the Middle East between now and then. And we suspect if there’s no big improvement in energy flows by mid-June, officials might still be tempted to raise rates. We’re open-minded; it’s just as conceivable that the Bank could play for more time.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more