Bank of Japan preview: New macro forecasts will shed light on next policy move

Markets expect no change in the BoJ's ultra-loose policy next week, but we still see a slightly higher chance of another tweak to the yield curve control policy, with forward guidance adjustments. Policy decisions aside, the BoJ's latest outlook will drive market moves

Growing speculation over BoJ policy change, but markets expect no change in current policy settings

The BoJ’s ultra-loose monetary policy continues to pile pressure on Japan's financial markets. The 10Y JGB yield is hovering around 0.85% while USD/JPY just broke the critical 150 level this morning. The BoJ has conducted an unscheduled bond operation and offered one trillion yen's worth of 5Y loans to commercial banks in order to bring yields down while FX authorities continue to warn FX market participants that they will intervene when necessary.

The weakening yen is putting more pressure on inflation, which will eventually hurt consumption, and a sharp rise in rates will likely hurt business investment. Increasing bond purchase operations, meanwhile, will put more of a burden on the BoJ.

However, the central bank is not yet ready to abandon its negative yield policy, as the prerequisites (discussed later) for such action have not been met. The YCC policy is facing greater challenges though as higher-for-longer trends strengthen globally. Thus we expect the BoJ's bond purchase operations to increase, aiming to slow the pace of the rate rises in the near future.

If the BoJ were to leave the current policy settings unchanged, however, financial markets might move in the opposite direction to the BoJ's wishes, and the economic recovery could falter, especially with growing concerns of a global economic slowdown. Also, a fresh outlook report will be released on the same day, which could support a policy change. However, if the BoJ misses the chance next week, it still leaves open the possibility of making such a decision at its December meeting. By then, the FOMC's decision will have been announced and the impact of the policy action could be even greater at a time when market volumes are thin at the end of the year.

The BoJ might change the 10Y JGB target

We think scrapping the YCC policy is too radical for the BoJ and the central bank will likely keep the current 1% flexible cap. In light of Governor Kazuo Ueda's comments at the last meeting that the appropriate level for the 10Y JGB is below 1%, the BoJ is unlikely to take the 1% limit any higher.

Instead, it is possible that the BoJ might lift its 10Y JGB target from the current level of around 0% to 0.25% or to 0.5% (the current formal upper limit of 10Y JGB) to reflect the current market conditions. Bringing the anchor year of the yield foward from the current 10Y to 5Y is also a possible option. Or the BoJ could make changes to its forward guidance. It would be more effective to signal to the market that the BoJ is gradually moving toward normalisation. If such changes come with a higher outlook for inflation in FY23 and beyond, it would give a clearer signal to the market.

BoJ’s quarterly forecasts will hint at the timing of policy normalisation

Even if the Bank of Japan doesn’t deliver any policy changes, the market will keep a close eye on how the central bank's growth and inflation outlook has changed, and it could still be a market-moving event mainly because it could give hints about future policy moves.

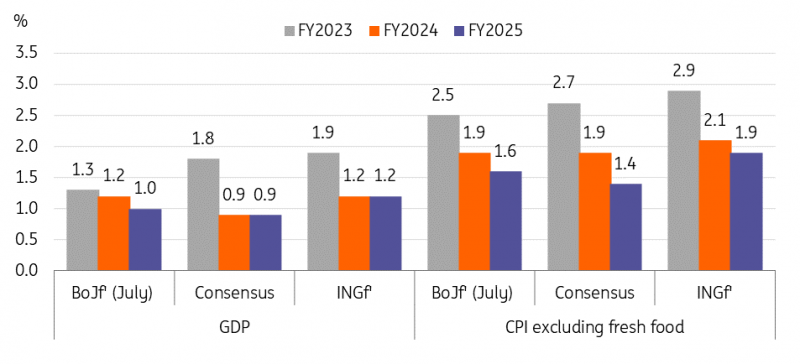

Since the quarterly projection release in July, both growth and inflation have exceeded the BoJ’s forecasts. Annual FY23 GDP is expected to be significantly upgraded to around 1.9% (vs 1.3% in July forecast, and 1.8% market consensus), as GDP growth in the first half of this year has been stronger than expected. Yet FY24/25 GDP forecasts are expected to be little changed as global headwinds intensify.

The market’s focus will be on the inflation outlook because the BoJ is aiming to meet the sustainable 2% price target, a major prerequisite for rate action. We believe that core CPI excluding fresh food for FY23 will be dramatically upgraded to around 2.9% (vs 2.5% in the July forecast, and 2.7% market consensus). Energy prices had climbed even before the Israel-Hamas conflict began, and service prices rose more than the BoJ expected. The energy subsidy programmes are likely to be extended until April next year, but inflation will likely stay above 2%. More importantly, we expect the BoJ to raise its FY24 core CPI forecast to around 2.1% (vs 1.9% in the July forecast, and the 1.9% market consensus), incorporating the recent rise in global commodity prices. Also, the base effect related to the energy subsidy programmes is likely to cause a temporary spike in inflation above 3% in February. In our own estimation, core CPI excluding fresh food will likely remain above 2% almost throughout 2024.

As argued in our previous report, we believe that three conditions must be met for the BoJ’s policy rate action. (1) Inflation above 2%, (2) wage growth of around 3%, and (3) a positive GDP output gap. We still think 2Q24 should be the right time for the BoJ’s first rate action. Inflation will likely stay well above 2% in the first half of 2024. Major wage negotiation results should be positive – given that RENGO, the largest labour union, is calling for a pay rise of at least 5% for FY24, and government policies will support wage growth. Lastly, we believe that the negative output gap will be closed by the end of 2023 at the earliest.

Market's attention is on the newest outlook report

Income tax cut will be discussed soon

Prime Minister Fumio Kishida said early this week that his cabinet is preparing a new economic stimulus package, including a temporary income tax cut for households and tax breaks for businesses. However, details of the tax cut proposal have yet to be revealed. We don't expect this impact to be incorporated into next week's BoJ outlook and we think Governor Ueda is unlikely to comment on this at the press conference.

USD/JPY: It's quiet, too quiet

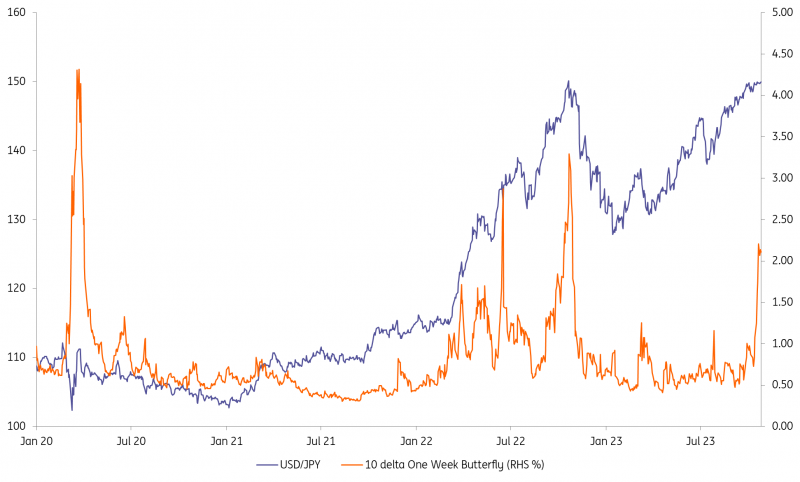

Somewhat amazingly – despite everything going on in the world including the horrors in the Middle East and the gyrations in US bond markets – USD/JPY has spent the month of October flat-lining very close to 150. Realised volatility has fallen to the lowest levels since January 2022 and it is not clear why.

It may well be that heavy FX option positioning in the 149-150 area (there are several large options expiring between 27-30 October) is combining with the threat of imminent FX intervention to suck the volatility out of USD/JPY.

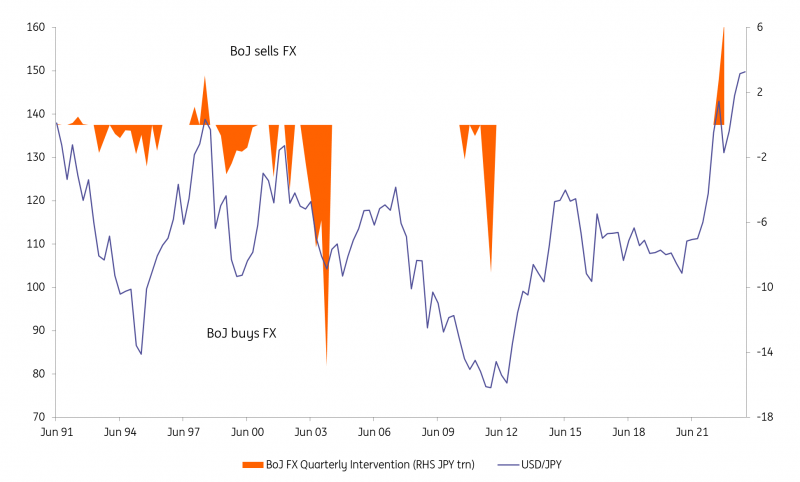

On the subject of FX intervention, 31 October should also be the day that the Ministry of Finance announces FX intervention figures for October. For example, did the BoJ sell dollars on 3 October when the USD/JPY skidded to 147.50 intra-day? The case against intervention is that there has been no follow-through selling from the BoJ and the intervention has not been confirmed. The case for intervention is the remarks from Japanese officials suggesting intervention would not immediately be confirmed plus the fact that on the one day USD/JPY did trade decisively above 150 last year, the BoJ sold $37bn in a single day.

Last year, Japanese officials were incredibly successful in their FX intervention since the broad dollar trend turned lower into October/November, as evidence of US disinflation came through and China undertook a U-turn on Covid restrictions. Like Chinese officials with USD/CNY at 7.30, it now looks like the Japanese are clinging to the defence of USD/JPY at 150 and praying that the broad dollar trend turns lower.

Japan has yet to confirm any FX intervention this year

While there are no immediate signs of the broad dollar trend turning, as above, we do think the prospects of a tweak to the YCC policy are underpriced. And those new macro forecasts will be big market drivers, with any FY25 CPI forecast close to 2% only adding to speculation of a BoJ exit from its ultra-loose policy. Given these big events on 31 October, we think the risks for spot USD/JPY are skewed to the downside.

Yet investors seem to be taking a more ambiguous view on the direction of the break-out by buying what are called butterfly options – i.e. selling the prospects of USD/JPY staying near 150 and buying the prospects of USD/JPY ending above 152 or below 146.50 (10 delta options) in one week's time. That is understandable given the predominant USD/JPY bull trend. Yet expectations of any YCC tweak seem relatively modest given that 10-year JGB yields (now at 0.85%) are only priced at 0.93% and 0.98% in three and six months, respectively in the forward market.

The cost of a one week, 10 delta butterfly option has been rising

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap