Australian GDP growth remains strong

At an annualised pace of more than 3.5%, the 2Q22 GDP data indicates the scale of the task facing the Reserve Bank in taming demand sufficiently to dampen inflation

| 0.9% |

2Q22 GDP quarter-on-quarter3.6% year-on-year |

| As expected | |

Growth as expected - still strong though

2Q22 GDP growth in Australia was 0.9% quarter-on-quarter, in line with the market consensus, though the year-on-year rate came in a bit higher at 3.6% YoY from an expected 3.4%, due to downward revisions to previous GDP numbers, lifting the annual comparison.

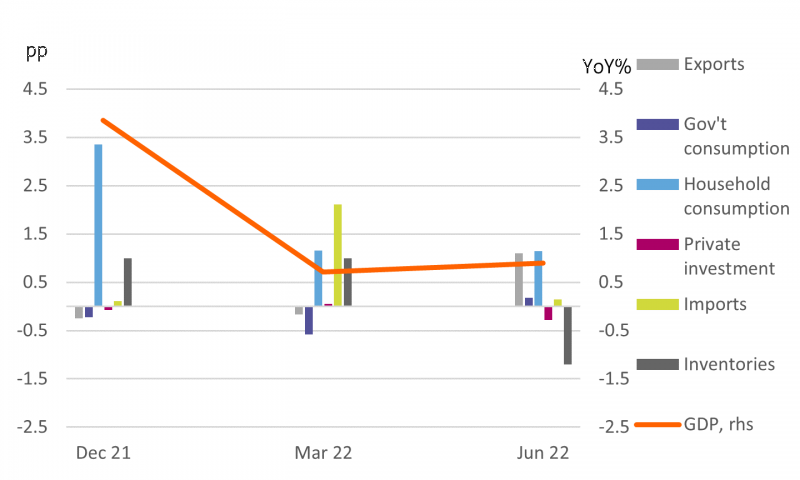

2Q22 contributions to QoQ GDP growth by expenditure type

Consumer spending remains strong

The chart above illustrates the contribution to the GDP total growth figure from selected expenditure categories, and it sheds light on the problem facing the Reserve Bank of Australia (RBA).

Firstly, household consumer spending is still growing rapidly, adding 1.1ppt to the headline figure. This will need to come down if overall demand is to soften sufficiently to dampen inflation. Private gross fixed capital formation (private capex) is looking much more subdued, which reflects weakness not just in residential construction, but across the whole investment spectrum. This segment of the economy has been soft for some time and it is unlikely to dramatically improve given the rates and tough external background...it could even get worse.

Net exports (exports minus imports) are still doing a lot of the heavy lifting. Imports didn't deliver any drag this quarter and exports were a positive boost. But unless domestic demand softens, we should expect the contribution from this sector overall to diminish in the quarters ahead.

There is also likely to be a boost next quarter from inventory accumulation, given the drawdown apparent this quarter, so we may be in for another similar headline figure of around 1.0% QoQ in 3Q22. If so, that would put full-year 2022 GDP growth on track to exceed 4% - not really conducive to getting inflation down rapidly and might indicate that rates will have to go higher and stay higher for longer to achieve the RBA's aim.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap