Australia: May inflation raises the spectre of rate hikes

Everything now hangs on the June inflation print, just days before the Reserve Bank of Australia’s (RBA) 6 August rate meeting. We need to see inflation dropping then, or we may be facing another rate hike

| 4.0 |

May inflation (YoY%)Up from 3.6% |

| Higher than expected | |

5 months in which inflation has gone nowhere except backwards

Until December 2023, Australia had made decent progress on inflation, with the December print of 3.4%YoY well down from the peak of 8.4% in December 2022.

Since then, inflation has not just stalled, it has started to rise again. The latest reading of 4.0% YoY came in well above the consensus expectation for a 3.8% increase and up from 3.6% in April.

We said a few months ago that we were just one bad inflation print away from taking out all cuts from our forecast. We removed the final cut last month. We also said we were just two bad inflation reports away from forecasting a hike.

Well, we're there now. And we are sorely tempted. The only thing stopping us from doing this right now is that we still have one more inflation report, just days before the RBA's next rate meeting on 6 August. The June report comes with the second-quarter inflation numbers and will carry more weight than today's data. Consequently, we think the RBA will want to see the June data before deciding whether or not to pull the trigger on a rate hike

But that is where the risks are skewed because we think the RBA will want to see concrete evidence that its policies are working by that August meeting and a "flat" inflation report then won't do that, it needs to show a decline.

The arguments for and against rate hike action are finely balanced for the August meeting

The May CPI data showed a very modest decline of 0.04%. There weren't any real surprises in the data. Motor fuel showed a fall of 5.1% MoM. That decline helped deliver a 2.5% MoM decline in the larger transport component. But that was as expected. Other than that, there were the usual predictable seasonal fluctuations in categories such as apparel and holiday prices.

For June, retail gasoline prices have risen by more than they fell in May, so the drag from transport could turn into a similar or slightly larger boost. Also, some of the drag from seasonal holiday prices could reverse in June. These two components, together with some slight underlying inflation from other components, could take the June CPI to about 0.6% MoM.

The 2023 June CPI index rose 0.73% MoM. So a 0.6% increase for June 2024 should deliver a 0.1pp decline in year-on-year inflation. That would take June monthly inflation back down to 3.9% YoY. But for the full quarter, and using our own seasonal adjustment, we think that would deliver something like a 1.1-1.2% QoQ increase, up from 0.88% in 1Q24, and 0.74% in 4Q23. The direction of travel is worrying.

If it were us, we'd have to admit that the evidence was not just pointing towards making inadequate progress towards the RBA's inflation target, but that maybe, rates hadn't been raised sufficiently high to deliver that target over the medium term.

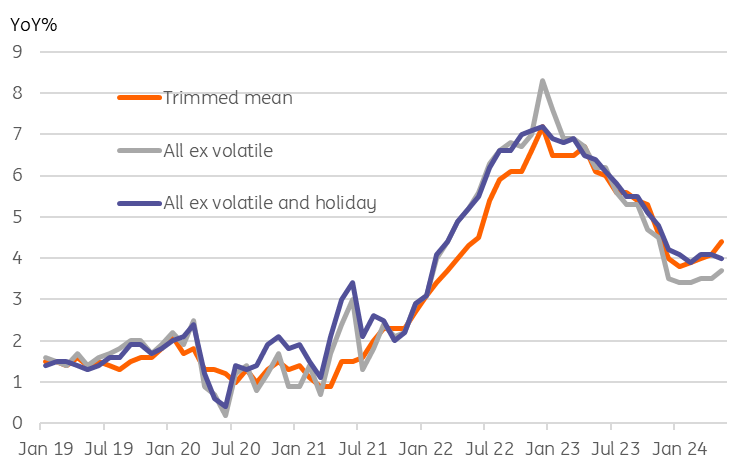

Various measures of "core" Australian inflation

Could core inflation provide some excuse for inaction?

Just to leave no stone unturned, we've looked at the various monthly core measures of inflation to see if we can find some underlying reason to be more optimistic about the inflation outlook.

And with the small exception of the May inflation rate for the index excluding volatile items and holiday travel, which dropped slightly to 4.0% YoY in May from 4.1% in April, the news isn't great. The measure excluding volatile items provides the lowest inflation reading at 3.7%. But this is still up from 3.4% in January. The trimmed mean shows an inflation rate of 4.4% YoY, up from a low of 3.8% in January.

There is no respite to be found here.

AUD spikes higher

The AUD spiked higher on the CPI release, rising from 0.6640 to close to 0.6680, though such spikes have recently proved short-lived, and the gravitational force of EURUSD has tended to keep the AUD rangebound. Short-term interest rate markets are at least beginning to price in just over a 50% chance of a hike by September, which seems sensible. We could see this rising to about 80% ahead of the June CPI release on 31 July, which could provide a further boost to the AUD.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap