Australia: Inflation declines in July

July headline inflation dropped from 3.8% in June to 3.5% YoY in July, though this was slightly higher than the consensus view (consensus 3.4%, ING f 3.5%). However, core measures of inflation came in lower and may offer more hope that inflation is finally beginning to respond to higher rates

| 3.5% YoY |

Headline inflation for Julydown from 3.8% in June |

| Higher than expected | |

Better news on inflation for the Reserve Bank of Australia

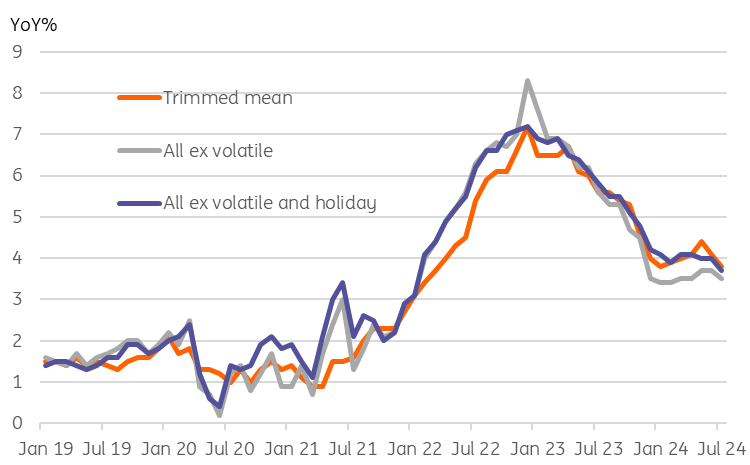

Although the headline index of inflation for July did not fall as much as the consensus had hoped for, declining only to 3.5% YoY from 3.8% in June, there is a lot to be optimistic about in this latest set of inflation data.

- The direction of travel is going the right way again - down. For much of this year, it has been sideways to slightly higher. We are not going to quibble over a tenth of a per cent here or there. Forecasting just isn't that accurate anyway.

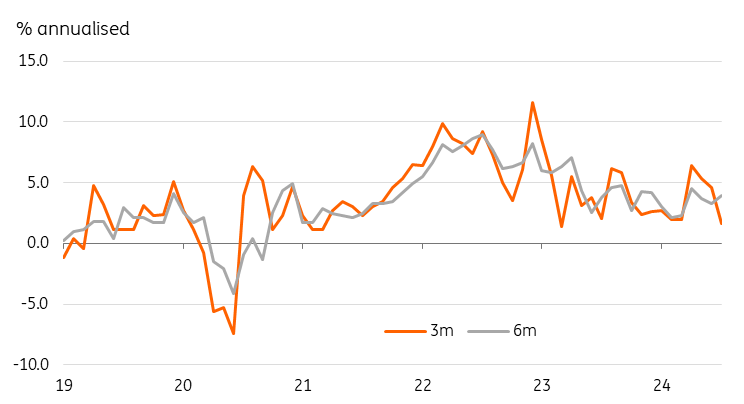

- The month-on-month incremental move was actually negative, which considerably improves the 3m trend run-rate of inflation, which had been much too high previously (the 6m rate still needs some work). The non-seasonally adjusted month-on-month move was -0.07% to two decimal places (backed out of the index numbers).

- Although there was clearly some help from volatile items like falling gasoline prices working through the transport component, and seasonal swings in recreation and holidays also played their part in the soft July number, core measures of inflation also all fell, offering some hope that the underlying inflation picture is also improving.

Core inflation measures are now falling again

Markets are dwelling on the negatives

The market response to this data is slightly odd, and while an end-of-year rate cut is still more than fully priced in, the implied yield for December has risen slightly. It looks like markets are more agitated by the slight upside miss to the headline index than accepting that the underlying story seems to be improving.

This is not the first time we have been at odds with the market's interpretation of events, and we still think a December rate cut looks unlikely. That said, we are encouraged by this latest data, which we think makes a first-quarter 2025 cut look less speculative than it had been looking.

It would be helpful now to see some supportive data from the activity side of the economy, most notably the labour market, to reinforce today's encouraging underlying inflation story. However, the next labour release is not until 19 September. We do, however, get 2Q24 GDP data on 4 September, which could help make the case for a cooler economy and a lower inflation outlook.

"Run-rate" (annualized) CPI measures

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap