Australia: Inflation breaches 5 percent

You have to go back to 2Q 2001 to find a headline inflation rate in Australia that is higher than the latest 5.1%YoY figure. Core inflation is also up. The Reserve Bank of Australia (RBA) will not be able to ignore this

| 5.1% |

CPI YoY%Up from 3.5% |

| Higher than expected | |

Headline inflation and core rates all up

Headline inflation in 1Q22 rose to 5.1%, a lot more than the consensus expectation of 4.7%, and comes off a 2.1% quarter-on-quarter increase, accelerating from 4Q21's 1.3%QoQ rise.

The quarterly increase was broadly spread among sub-components. The only item to decline this quarter was clothing (-0.6%QoQ). A few other items put in modest price growth: communications (0.3%QoQ), recreation (0.6%QoQ), and insurance/finance (0.5%QoQ). All other items showed gains of one per cent or more over the previous quarter, led not surprisingly by transportation (4.2%), education (4.5%), food (2.8%), housing (2.7%) and health (2.3%).

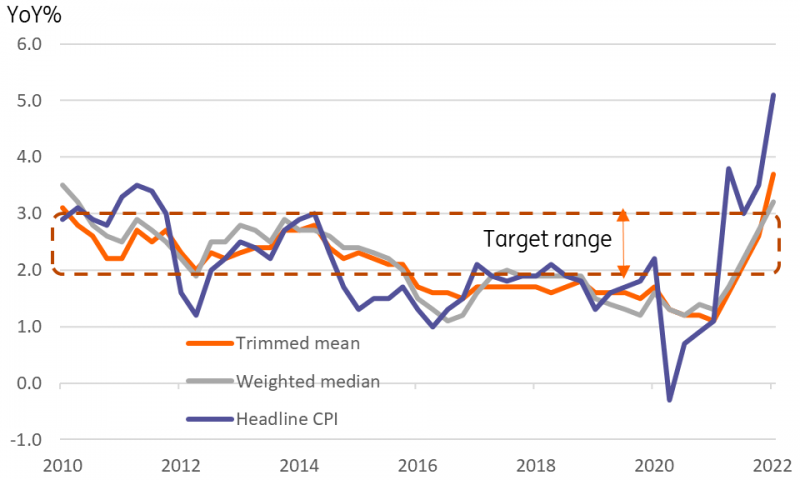

The broad spread of gains meant that as well as the rise in the headline inflation rate, core inflation rates also surged. The trimmed mean inflation rate rose from 2.6% to 3.7%, and the weighted median inflation rate rose from 2.5% to 3.2% (see chart below). With the Reserve Bank's target for inflation of 2-3%, all three measures of inflation are now comfortably above the upper band of that target.

Headline and core rates of inflation

What will the RBA do?

The Reserve Bank of Australia has been slowly trying to distance itself from the incredibly dovish stance it took early last year when it sought to portray itself as always slightly more dovish than the US Fed. But with the Fed now about to start ramping up its rate hikes by 50bp at the coming few meetings at least, that relative positioning doesn't mean a lot anymore.

You don't have to go too far back in history to find RBA statements saying that rates would be unlikely to rise before 2024. More recent iterations of their statements have pared back this guidance and walked away from specific dates, instead, replacing calendar references with comments about "patience" with respect to monetary policy. That too was jettisoned at the April meeting.

Today's inflation upside miss also makes the debate about whether or not the inflation increase is "sustained" somewhat redundant. There was at one time a view that for this to be the case, we would need to see the wage price index growth rate hit 3% or more (it was still only 2.3% in 4Q21). The 1Q22 release of this is not due until after the upcoming 3 May RBA meeting (wage prices released on 18 May) and it is only because of this that we think the coming meeting will be about positioning the market for a June hike, rather than starting to hike next week.

There is also now increasing justification for the first move being more substantial than we first considered likely. Taking the cash rate target to 0.5% with a 40bp hike from the current 10bp would seem to make more sense now than a 15bp hike to 0.25%, which bond markets might now view as a derisory response to the inflation surge and the record low unemployment rate. The AUD's recent dip also makes more room for the RBA to hike more aggressively, and arguments for the "front-loading" of policy make as much sense for Australia as they do for the United States.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap