Australia: Current low inflation likely to unwind

The latest October monthly inflation figures for Australia delivered a 2.1%YoY inflation rate, lower than expected. But markets weren’t particularly moved by the numbers, focussing more on core rates and the prospects that some helpful factors may be about to sunset

There is some good news on inflation...

At 2.1%YoY, the October headline inflation rate was a little lower than had been expected and remained unchanged for a second month. This is well within the Reserve Bank of Australia's (RBA) inflation target (2-3%) though markets are not getting very excited, and there was little response from the AUD or bond yields to the figures.

The main problem is that these inflation figures are heavily distorted by government policy measures, and so the underlying rate of inflation is probably higher than this, and is likely to creep up in the coming months.

There are two important elements to this:

But there is also some bad news...

Firstly: cost of living electricity subsidies continue to have a large impact on the headline inflation rate. Since these began to bite, they have contributed a negative 1.3pp to headline inflation, which would otherwise be running at about 3.4% YoY. However, we feel that the maximum impact of these subsidies is now being felt, and over the coming months, their influence should drift back towards about zero or even turn positive, working against any underlying tendency for inflation to decline - which is in any case, not that evident.

Secondly: There is also likely to have been some drag on inflation from the rental component of housing, via the Covid-era Commonwealth Rental Assistance policy. The CPI measure of rents shows a slight decrease in the annual inflation rate and has not risen on a monthly basis by much recently, though the inflation rate is still running in the high 6% YoY range. The marginal impact on inflation now is probably only quite limited. It will be interesting to see which way this turns over the next few months.

Thirdly: After falling sharply for the last three months, the motor fuel component of transport also flattened out in October, and over the coming months, we would expect this to be less of a drag on headline inflation too - depending on some hard-to-predict geopolitical influences.

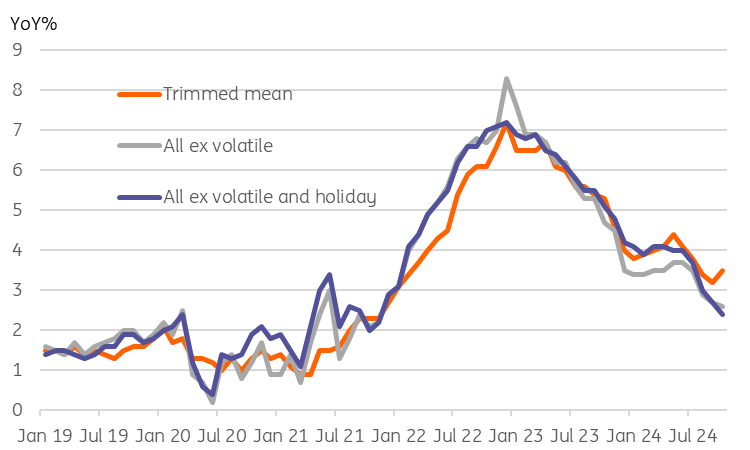

All of these factors are evident when you look at the trimmed mean inflation rate for October. Here, instead of declining, the inflation rate ticked up from 3.2% to 3.5%. And it is this core measure that the RBA is probably focussing on more than headline rates.

Core measures of inflation (YoY%)

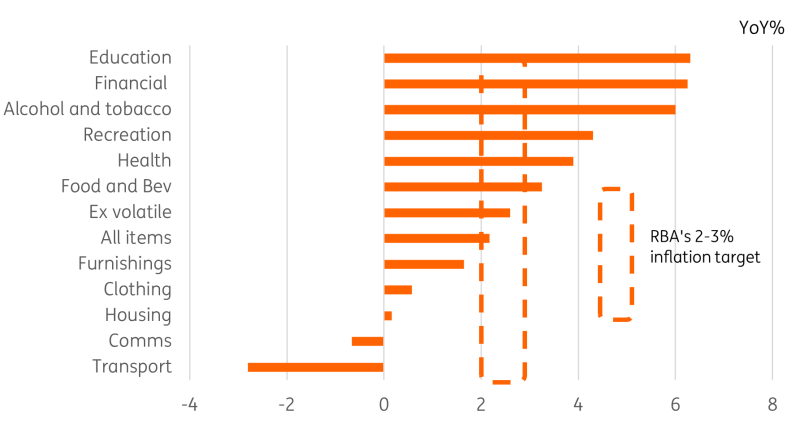

Some components have now drifted back within target

Looking at the other components of inflation, many remain well above levels that will be consistent with the RBA's inflation target, though furnishings, clothing, and communications are looking more respectable. This is also an improvement compared with a year ago when there were almost no components falling into the RBA's target range.

Australian CPI inflation by component (YoY%)

The RBA can take its time on rates

The upshot of all of this is that there is simply no rush for the RBA to do anything with rates anytime soon. Our 1Q25 rate cut forecast remains an "at the earliest" view, and there is certainly scope for this to be pushed back, whereas the scope for a near-term cut seems vanishingly small.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap