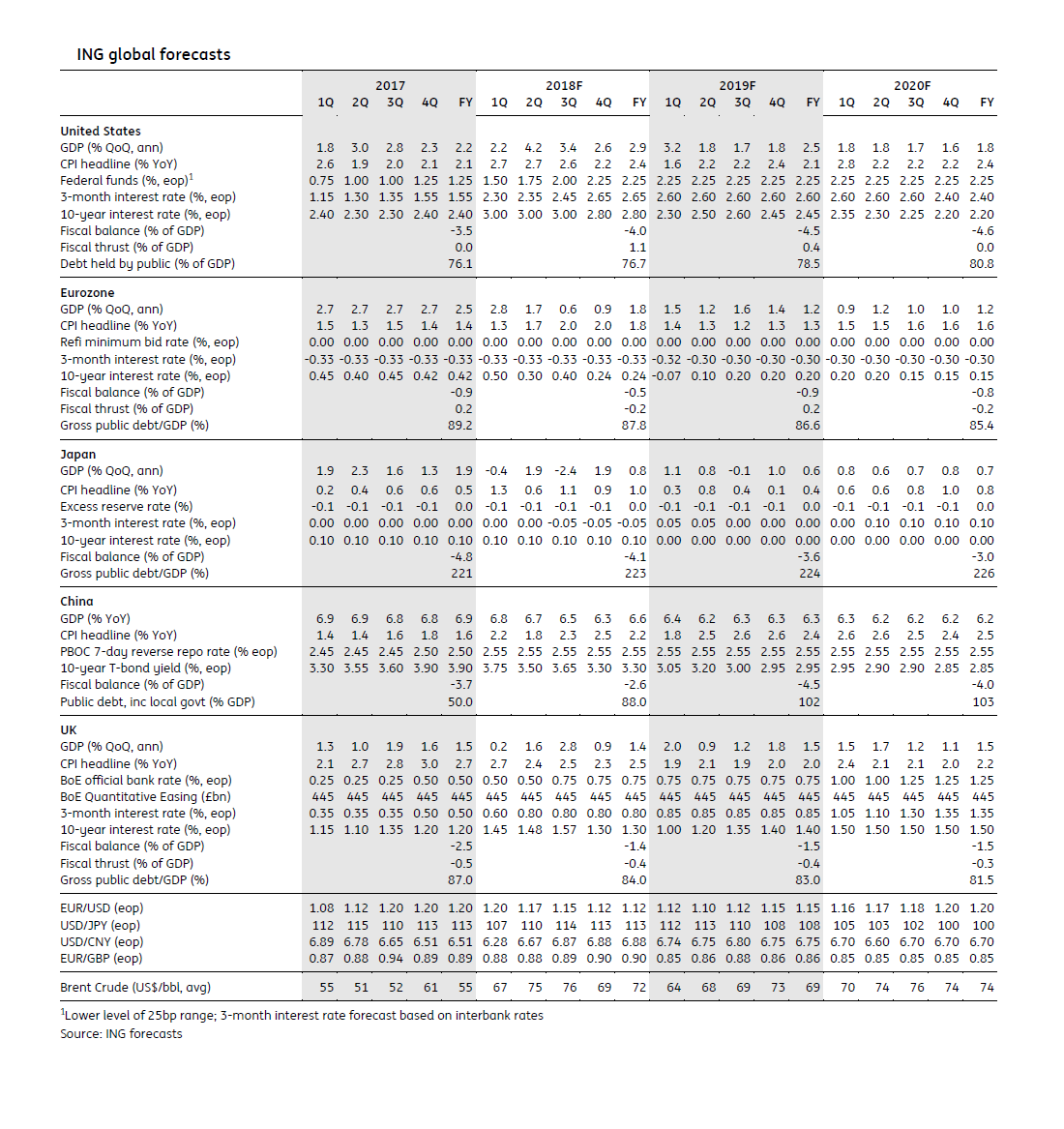

- Report

May economic update: Just when things were looking up

- 10 May 2019

Just as pockets of optimism had begun to emerge in the global economy, trade tensions are back, though we still think a US-China trade deal remains likely. But in the meantime, trade uncertainty, as well as risks relating to forthcoming European elections and Brexit, suggest that financial market caution is likely to stay with us for a little while longer

Trade tensions return

Just as pockets of optimism had begun to emerge in the global economy, trade tensions are back. President Trump has taken the trade war a step further with the imposition of fresh tariffs on China, which also raises questions about the possibility of auto tariffs. We still think a US-China deal remains likely, not least because President Trump will not want a damaged economy and stock market as he heads into a key election year. But in the meantime, trade uncertainty, as well as risks relating to forthcoming European elections and Brexit, suggest that financial market caution is likely to stay with us for a little while longer.

The re-emergence of US-China trade tensions has spooked financial markets, but ultimately we still think a deal is likely. Failure to get a deal, perhaps coupled with further tit-for-tat tariff hikes, would be harmful to both economies and would hit equities. Such an environment would be deeply damaging for President Trump’s chances of re-election in 2020, so we suspect the latest move is designed to extract last-minute concessions from China, rather than a serious effort to trigger a larger global trade war.

However, stronger-than-expected growth in China following earlier fiscal and monetary stimulus provides its government with some extra chips when it comes to renegotiating. The negotiations concern much more besides trade – China’s ability to export its 5G network, coupled with geopolitical tensions in the South China Sea, also matter.

The US economy

Despite the ongoing uncertainty, the US economy continues to prove the doubters wrong, following another robust GDP growth figure for 1Q19. The economy is adding jobs in significant numbers, while financial conditions continue to improve thanks to rising equity markets, a strong and stable dollar and falling mortgage rates. Inflation could rise more quickly than the market anticipates given rising fuel costs and wage pressures emanating from the labour market. While financial markets continue to price in interest rate cuts, the Federal Reserve is maintaining a cautiously upbeat tone that signals stable monetary policy through 2019.

The Eurozone also saw stronger-than-expected first quarter growth, which was probably helped along by a normalisation of the exceptional factors that had held back growth in the second half of last year. But while a recession certainly doesn’t look imminent, a growth acceleration also seems unlikely. The rise in April inflation was caused largely by calendar effects so there’s not much sign of an upward trend. All this suggests the ECB will stay put for the time being.

The UK's ongoing dilemmas

In the UK, there are good reasons to think that the Brexit deadlock won’t be broken before the new October Article 50 deadline. Cross-party talks don’t appear to be making much headway, while there remains a risk of a summer Conservative Party leadership battle. A further extension to the Article 50 period is perhaps more likely than not. But while we think a ‘no deal’ exit will be avoided, firms will have to continue making preparations and this will keep a lid on economic growth over the summer months.

May is typically a bad month for EUR/USD. 1.10 looks the target this summer as US data holds up well and the ECB contemplates the signals it wants to send with the TLTRO III in June. A surprise decline in the Renminbi would also shake up the low volatility mood.

While risk assets have rallied off earlier lows, the US 10-year yield has not managed to budge much from the 2.5% area. However, the positive macro-story in the US, coupled with the fact that a Fed rate cut remains some way off, suggests the balance of risks are slowly swinging back in the direction of a test higher for market rates.

Included in the following bundle

What’s happening in Australia and around the world?

- This bundle contains 7 Articles

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more