Omicron in the Asia pipeline

It's probably only a matter of time before Omicron-infections really kick off in Asia. The question is, will governments take it in their stride, or will this lead them to moonwalk back their re-opening efforts?

Things look and feel very different in Asia than Europe

I've just returned from 2 weeks holiday in Europe. Practically every family we know has had at least one Omicron casualty, though fortunately, none of them serious - most of them very slight. But it has ruined Christmas for many. Holiday's have been cancelled, reunions shelved. As far as I am aware, our family's hermit-like existence at our rural French retreat has left us all unscathed, though I am only halfway through my VTL testing period, so never say never. And the wife still has to run the gauntlet of 2 days in London before she heads back to Singapore. So we are not in the clear yet.

But it feels very different here in Asia. Where France, Germany and the UK have been seeing 100,000-200,000 cases some days, all these countries seem to be trying, as far as is possible, to take a pragmatic approach to what appears to be an intrinsically milder variant of Covid-19. Here in Asia, Omicron is on everyone's mind, but it isn't yet a clear and present danger for most. And it isn't affecting behaviour particularly. Oddly, with only about 840 daily Covid-19 cases and zero deaths yesterday, Singapore has, according to Bloomberg, been put on a travel warning for US travellers. The US in contrast is tallying 500,000 cases per day. This seems a bit odd.

But what also seems to be abundantly clear, is that while Asia is not yet suffering the full fury of Omicron, it is only a matter of time before Omicron really starts to take off. And as the reaction functions of Asian governments throughout the crisis have been inherently more conservative than their European or American peers, it is not unreasonable to be a little bit concerned about where this may lead. Global markets seem to be writing off Omicron as an existential threat, with some suggesting that the Omicron variant represents the 'last hurrah' for Covid. Let's hope they are right. But there may still be a final hit to activity in Asia before we can return to a semblance of normality.

Omicron vulnerability in Asia

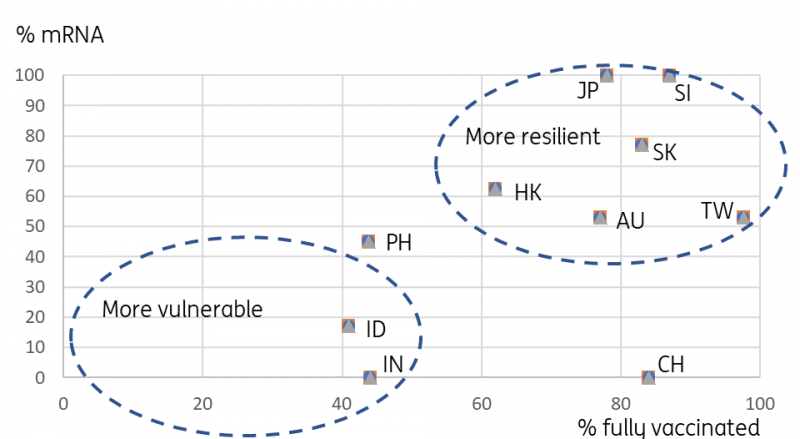

Where is the biggest worry for omicron?

One question that we will see answered over the coming months will be whether China's zero-Covid policy is maintained in the face of Omicron. I will avoid commenting on whether I think they should persist with this approach (that sort of comment gets economists into trouble), but with Omicron reportedly 70-times more infectious than even Delta, I would question whether strict lockdowns and hosing cities down with disinfectant will actually work. My non-medically qualified gut feel is that this is an unwinnable battle. Of course, if this zero-covid policy remains in place, then there is a good chance that we will see lockdowns drag on across the year weighing on an already subdued growth prospect for China.

Elsewhere in the region, my main concern is that most of the Omicron analysis I have read so far relates to heavily vaccinated populations (Europe, UK). Also, a lot of the studies I have read in the last few days seems to indicate that of the vaccines widely distributed, only the mRNA type of vaccines seem to offer much in the way of protection from infection, and that these also provide a greater degree of protection from severe forms of the disease. This is perhaps a reason for some governments in Asia to be a bit more cautious than those in Europe / US when Omicron numbers inevitably start to rise sharply.

In the chart above, we show a scatter diagram showing the percentage of the populations in the region that are fully vaccinated against the proportion of vaccinations in each country that are mRNA based (for example, Pfizer, Moderna).

So for example, China is heavily vaccinated, but almost exclusively with Sinovac / Sinopharm's traditional vaccines - though it seems that boosters are now focussing on mRNA vaccines to provide a stronger degree of protection. India is not nearly as well vaccinated as China, and it too has focussed almost exclusively on traditional vaccines, mainly based on the AZ vaccine produced locally. Indian daily cases have been very low in recent weeks, only about 7000 or so. Earlier this week, the daily case numbers rose to 9,000. Today, they were 34,000. At this rate, Indian daily cases will be in the 100,000s by next week, and there is no telling where the peak will be. However, judging by other countries, it will at least match the 400,000+ tally hit during the March/April 2021 wave. Again, the question is, will this overwhelm health services locally? Or is Omicron so intrinsically less severe that India can just push on through?

As well as India, both Indonesia and the Philippines also lag the median in terms of vaccination rates and in terms of the prevalence of mRNA vaccines in that mix. Both countries struggled with access to vaccines in the early stages of the rollout and had to rely on donations of Sinovac / Sinopharm as well as Astra-Zeneca. More recently, both countries have been concentrating more on mRNA vaccines, but the bulk of their historical vaccine protection relies on traditional vaccines that may prove ineffective against Omicron.

Markets are torn, but will probably keep rising

As far as markets are concerned, there is a clear tension here. Global markets seem to want to find a silver lining in the Omicron wave, and Asian markets should benefit from any sentiment upturn. But the experience of Europe may provide too optimistic an extrapolation for some Asian economies. And improving global sentiment could clash against a negatively evolving story locally and against a stronger USD and higher bond yields, both of which could take the wind out of Asian risk sentiment.

Asian markets will therefore likely remain quite choppy for the next few weeks or months as we get to know Omicron better and can get a better understanding of where the world is heading. But the underlying trend could well remain a positive one, punctuated by occasional periods of local anxiety.

As my first note of the year, let me take this opportunity to wish you all a healthy and prosperous New Year. Good luck.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download opinion