Momentum waning in US Treasuries, Korean output

The recent Treasury sell-off has taken a breather; Korean production momentum also appears to be losing some momentum

Who's in the driving seat?

In recent days. it has been the rise in bond yields that has driven market moves from equities to FX, but overnight, it looks as if the equity market has stolen back control, with big increases in the S&P500 and NASDAQ taking them to within spitting distance of their recent all-time highs. This still helped deliver a small increase in 10Y US Treasury yields, which nudged up just over one basis point to 1.417% as of writing. So it looks as if equities are now driving other markets, not the other way around. So what next?

Well, while it may be tempting to conclude that the equity market is getting used to higher yields, this also means that this takes away one of the hurdles for yields to keep moving higher. What would undermine an uptrend in bond yields, would be a big collapse in risk appetite, brought on by too precipitate an increase in the first place. This new two steps forward, one-step-back approach keeps the uptrend intact, but also enables it to keep drawing fresh market interest and keep going.

I don't believe we have seen the end to increases in inflation expectations in the US, nor potentially to the end of rises in real bond yields, which still have a way to go before we might conclude that they have reached a sensible level, which means no longer substantially negative, even if a decent positive real yield remains elusive.

Divergence between Fed and ECB a factor for EURUSD?

One of the clearest divergencies in central bank rhetoric currently is between the ECB and the US Fed. Yesterday, The Fed's Barkin declared he was not too concerned by the increase in US Treasury yields, as it reflected greater optimism about the recovery, and some improvement in inflation expectations - both things the US Fed has been trying to achieve. Barkin says he remains more concerned about the US labour market, where there is still plenty of slack.

Compare that with the ECB's Villeroy de Galhau, who remarked that the ECB "...can and must react..." against any unwarranted rise in bond yields that threatens to undermine the euro area economy. With this difference in central bank stance getting more glaring, one could be forgiven for thinking that this undermines thoughts of a much weaker USD, and again overnight, the USD had a decent day, dropping to just a bit over 1.20.

Further Fed commentary may be available this time tomorrow, as both Brainard and Daly will have spoken at various events, so we may get a further angle on Fed sentiment.

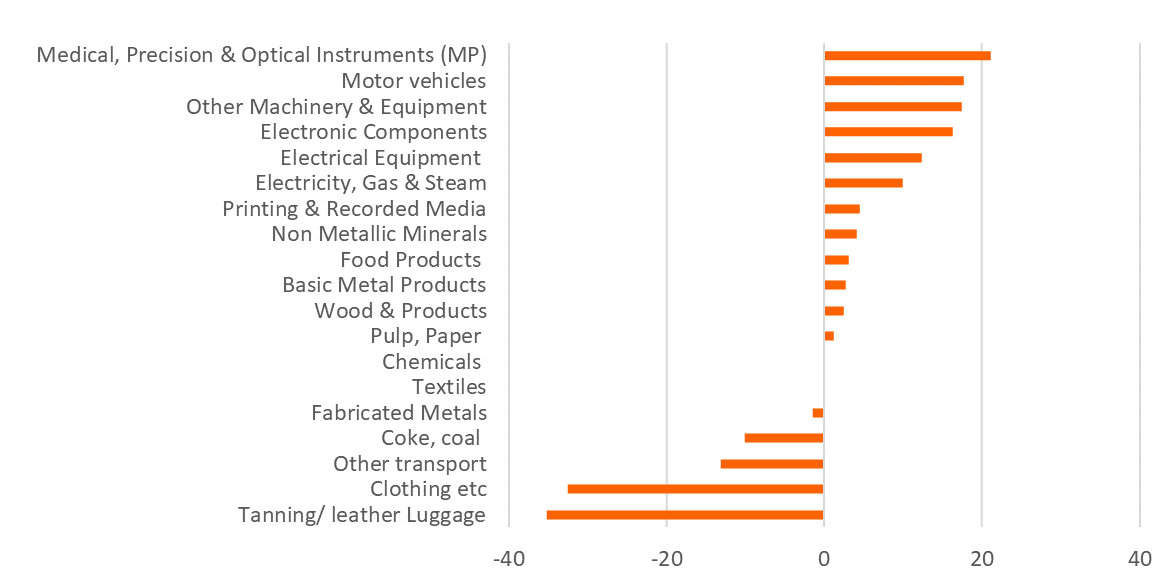

Korean production by item type (YoY%) January 2021

Korean production, a bit up and a bit down

I have found it virtually impossible to draw any firm conclusions on Korea's January industrial production data out this morning. Although the year-on-year production growth rate increased to 7.5% in January, up from 2.5% in December and stronger than the 5.9% expected, this came as a result of a much weaker than expected monthly growth figure, which showed production declining by 1.6%MoM. The only way you can reconcile these two events is if the history of production data over the last year has been extensively revised lower.

The breakdown of production growth by component shows technology and electronics still leading the way, but there is quite a drag from clothing and items associated with travel such as luggage. Most items are showing non-descript growth of low single digits, and it is only when you get to electrical equipment that the growth rates look to pick up. This data is not inconsistent with the poor Korean labour market data we have seen recently, and indicates that the BoK will not be rushing to normalize their policy rates any time soon - certainly not this year, and maybe not until well into next.

RBA meeting

After their recent intervention in the bond market, the RBA's monetary policy statement due out this morning might also make interesting reading. The 3Y Government bond yield remains a shade over the 0.1% target, and though 10Y Australian government bond yields are off their recent 1.9277% highs, they do show signs of creeping higher again from their current level of 1.6663%.

The RBA may be able to influence their own bond market (actually, that is yet to be conclusively proven), but it is not clear how much of the recent rally was their doing, and how much just the spillover from the correction in the UST market. One thing is sure, if US Treasury yields decide to power higher, the RBA does not have the firepower to stand in its way and Australian bond yields will be dragged higher. So even if the policy statement outlines a greater commitment to keeping bond yields under wraps, except for the front end of the curve, I wouldn't read too much into that.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download opinion

2 March 2021

Good MornING Asia - 2 March 2021 This bundle contains 2 Articles