Markets return to risk aversion

It didn't take very long before oil markets shifted their storage concerns from yesterday's expiring May contract to the June NYMEX WTI future, and stocks are following oil lower

Mood sours on oil

Stocks were looking precarious yesterday on the back of the collapse in front-month WTI futures to an unprecedented negative level. That contract expired yesterday, and the negativity has transferred straight to the new June contract. Admittedly this has recovered a bit, having traded as low as $6.50 and is now running at about $13.93, but it highlights that yesterday was not a one-day blip, but a problem that is going to need to be dealt with and priced in until US oil supply drops enough to eat into the supply glut, or demand recovers sufficiently to do the same.

As the demand story rests upon opening up the states again, and as that rests upon the Covid backdrop, we'd have to say that we wouldn't be holding our breath that demand provides much of the heavy-lifting in this process. New Covid-19cases in the US ran at about 28,000 yesterday, close to where they have been in the last week or so. ANd they look like they will come in about the same today as the numbers roll in ((just over 27,000 at the time of writing). I think you could just about say that there was a downward trajectory developing, but it is a very shallow one. Supply will, therefore, be more likely to be the main mover in this oil story.

Creeping lockdown will hit GDP in Singapore

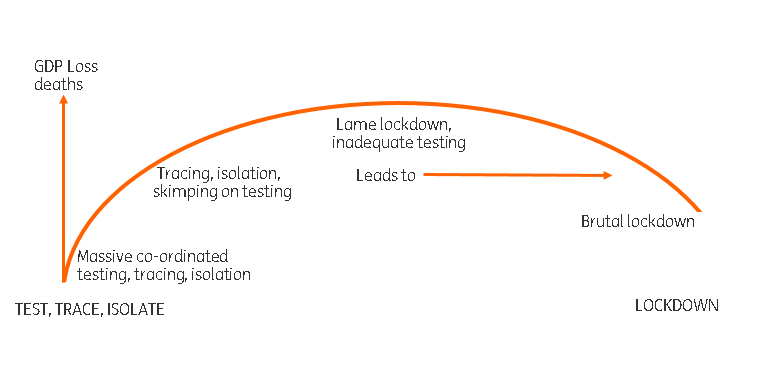

The extension to the "circuit-breaker: in Singapore to June 1 will have a negative effect on GDP, and Prakash Sakpal talks more about this below. In my view, the Covid-19 impact on an economy rests heavily on the policy response to it. We can represent this as a lopsided inverted smile as in the diagram below.

The vertical y-axis of this stylistic diagram (hence no units) is the damage (loss) to the GDP counterfactual. The higher you go, the bigger the loss compared to what would have happened. The horizontal x-axis takes you from a high-testing, high-tracing, high-isolating approach on the far left, which exemplifies Korea's approach to the pandemic, across to the far right, where you have a fairly brutal Wuhan-style lockdown, which we can typify as the Chinese response. The loss from lockdowns is always greater than a test-test-test model, but if you miss the boat on testing (which most economies did), and can't deliver that model, then a rapid and total lockdown (we would argue) hurts less and is over more quickly than a creeping piecemeal lockdown. This ends up just lasting longer as it is far less effective at squeezing out infection rates. But it crimps consumer spending almost as much while it is in place.

Singapore probably now joins Japan in such middle-ground, though we would probably put Indonesia's half-hearted movement restrictions at the very lower end of the effectiveness table, which suggests to us that at some stage, they will be compelled to adopt a much more restrictive approach. This is the main reason that Nicholas Mapa is chopping his 2020 forecasts for Indonesian GDP to -0.5%, joining the ranks of all the other lockdown negatives for the year. In contrast, our forecast for Korea is about flat for the year - not a bad outcome all things considered, and we may end-up revising it higher if all goes well.

Stylistic diagram representing Covid-19 response and loss of GDP

Circuit breaker extension and other ASEAN news

(From Prakash Sakpal)

Singapore: The government extended its circuit-breaker measures by four weeks until 1 June given the accelerated Covid-19 spread over the last few days. It also ramped up support measures with S$3.8 billion of additional budget spending on job support schemes. Even so, the extended circuit breaker means a bigger dent to GDP growth in the current quarter than we earlier thought and a prolonged recovery once the pandemic ends, whenever that is. We are cutting GDP growth forecast for 2Q20 to -6.8% YoY from -4.5% and for the full-year 2020 growth to -3.7% from -2.6% earlier.

Malaysia: March consumer price data is due. The sharp slump in demand due to the Covid-19 lockdown beginning in mid-March underscores the consensus view of inflation slipping into negative territory, -0.1% YoY down from +1.3% in February. We expect food and transport prices to be the key negatives here. This brings further support to our forecast of an additional 50bp Bank Negara rate cut in this quarter.

Thailand: Trade dodged Covid-19 pain in 1Q20 with a 0.9% YoY rise in exports and only a 1.9% fall in imports in the quarter. The continued large trade surplus suggests net trade contributed positively to GDP growth in the last quarter, but probably only to be outweighed by the increasing drag from weak domestic spending and stalled tourism. We consider our -2.2% YoY 1Q GDP growth view at risk of a downside miss (data due in mid-May), keeping the Bank of Thailand on course for a further 50bp rate cut in the current quarter.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download opinion

22 April 2020

Good MornING Asia - 22 April 2020 This bundle contains 3 Articles