Why Fed rate rises are a self-harming process

The Fed makes a payout to participants who hold reserves and to those parking overnight cash. These were small when rates were zero. As they approach 5% (market discount) they become considerable. They are offset by coupon income from the bond portfolio, but not by enough to prevent the Fed from moving into a deficit

Federal Reserve interest rate hikes are painful for the economy. But they are also painful for the Federal Reserve itself. There are two elements here: 1. The return on the Fed’s bond holdings, and 2: Interest rate payments that the Fed itself needs to pay.

Both of these are off the charts and implicate the Fed in a self-harming process that’s far from complete. Let’s take these one at a time.

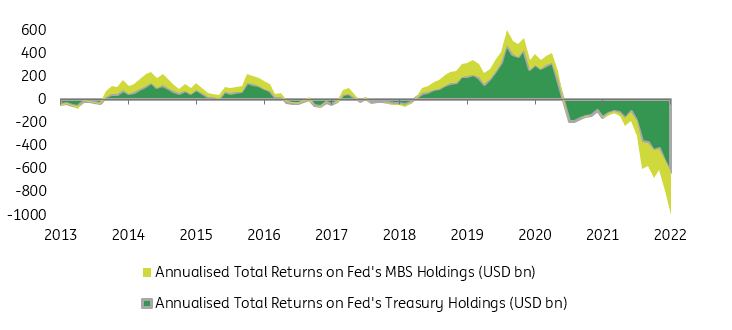

First to the Fed’s bond holdings. These have rocketed through various iterations of emergency bond buying (the Great Financial Crisis and the pandemic), and have left the Fed with a large bond portfolio on its hands. Total returns on bonds for 2022 are the worst on record for modern times, with Fed hikes a key driver. US Treasuries are running on returns of some -14% year-to-date. Applying this to the Fed’s holdings shows a remarkably large negative total return of approaching USD 1trn so far in 2022 (annualised) when the Treasury and Mortgage-Backed Security holdings are aggregated.

US Treasuries are down 14% so far in 2022

At first sight, this looks quite severe. However, for now, this is no more than a paper return and accounting treatment would determine whether the numbers are impactful or not. And they should not be, to the extent that bonds eventually roll off at par, and are held on an amortised cost basis. Another measure of pain in the book might be to look at the average price, which is currently at around 93 on the dollar, a 7% price discount. The longer-dated holdings are at a much deeper discount, but as long as coupons are paid and redemption is met by the US Treasury, there is no material issue.

The Federal Reserve’s net income for 2021 showed a figure of USD 108bn, up some USD 19bn from 2020, and the bulk of this increase was from interest income – effectively coupon payments – on its bond holdings. Even if bond prices fall, they will still pay coupon payments. And to that extent, the bond portfolio continues to make a net positive interest rate contribution. Consequently, it’s worth noting the valuations, but it should not prove to be destabilising and in many ways, it’s a reversal of the positive returns seen in previous years, as you can see in the chart below.

Estimated rolling total returns from the Fed’s holding of bonds

USD bn, annualised

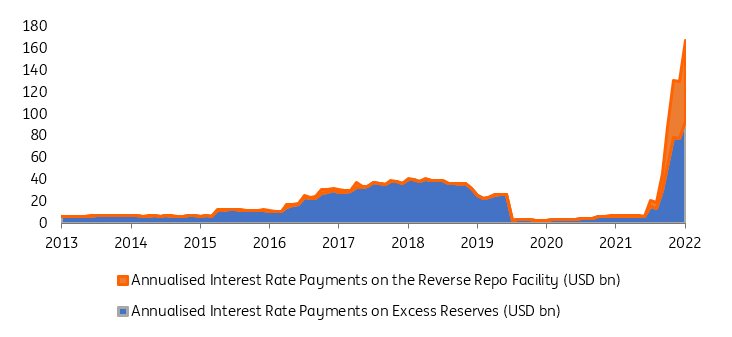

Secondly, there are the payments the Fed makes to eligible counterparties that park cash with them. There are two main routes here. First is the rate paid on excess reserves. Before the Great Financial Crisis, only regulatory reserves were compensated. But that changed as the Fed used the rate on excess reserves as a means to control front-end market rates, helping to ensure that the effective funds rate continued to trade within the ceiling and floor funds rates. The cost of doing so was minimal, as rates were on the floor and the Fed started by paying 25bp on excess reserves.

Fast forward to today though and the rate paid on excess reserves is 3.15%. Moreover, it will be 75bp higher post the 2nd November FOMC meeting, and the market discounts that it gets will be quite close to 5%. On top of that, the volume of excess reserves is now massive, at around USD 3trn. On an annualised basis, the remuneration cost to the Fed at this window is approaching USD 100bn. At the beginning of the year, it was below USD 10bn.

The Fed is now paying $170bn on cash parked with it, up from below $10bn

Reserves are off their highs though, down from a peak in the USD 4trn area. But this has been facilitated by a rocketing in cash going back to the Fed on the reverse repo facility. That’s gone from practically zero at the beginning of the year to over USD 2trn currently. It gets renumerated at a rate of 3.05%, and again that continues to rise in line with official rates. Based on where we are now, the annualised remuneration in this window amounts to around USD 75bn. In total, the Fed is paying some USD 170bn on these windows combined, as we illustrate below.

Renumeration payments made by the Fed on facilities

USD bn, annualised

On the other side of the balance sheet, the Fed can offset some of that through interest rate receipts on other facilities. In fact, the bond portfolio is the largest contributor. If we take a simple back-of-the-envelope average coupon of 2% on a combined USD 7.5trn bond portfolio, that would provide an interest rate receipt of some USD 150bn. That almost covers it. But note that if key rates head towards 5%, that will add an additional interest rate cost of some USD 100bn, which is approximately the size of the Fed’s total net income for 2021.

At the end of 2021, the Fed’s interest rate cost on the reserves and reverse repo windows was less than USD 10bn, and the Fed had a net income of USD 108bn for 2021. The simple running yield coming from coupon payments was in the region of USD 150bn. For 2022, that running coupon income is broadly similar, and actually a tad lower as USD 95bn per month of bonds is rolling off the front end. But the remuneration the Fed will pay out on the reserves and reverse repo windows rockets to an average of a little over USD 100bn for 2022 as a whole, moving the Fed into the red.

The Fed's running payout on cash parked with it approaches $250bn by December

Moreover, it ends the year running at around USD 250bn, painting an even heavier picture for 2023. That’s an additional USD 150bn running cost to be paid versus now. Under Fed accounting rules they would build an equal and opposite offsetting deferred asset, which would be paid down once the Fed returns to a net income position. But it still flips the Fed from being in a comfortable black position to being deep in the red.

Does all of this matter? Well, the annualised journey over the next few months in terms of net income won’t be pretty. Putting some round numbers on it, the swing factor likely sums to an annualised running USD 100-150bn hole at the Fed. At least until the Fed cuts rates in 2023. We think they will, and that will help. The Fed's ongoing roll-off of bonds from its balance sheet will also help, as it will reduce excess liquidity in the system, likely prompting less parking of cash at the Fed's reverse repo window.

Read more about what we expect from the Fed this week, and beyond here.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download opinion

Padhraic Garvey, CFA

Padhraic Garvey is the Regional Head of Research, Americas. He's based in New York. His brief spans both developed and emerging markets and he specialises in global rates and macro relative value. He worked for Cambridge Econometrics and ABN Amro before joining ING. He holds a Masters degree in Economics from University College Dublin and is a CFA charterholder.

Padhraic Garvey, CFA