- Opinion by Padhraic Garvey, CFA

Colombia: Another rate hike process begins - how to play it

- 29 January

- Rates

We've been here before – on the eve of a rate hike process. Higher rates are indeed required. But the extent of cumulative hikes need not be as some may think, nor is there a need for super large individual hikes. Market rates are already ahead of the pace, and the peso is strong (but complex). We identify three strategies with a view to ultimately getting long

Three issues to consider as we assess the prognosis for Colombian rates

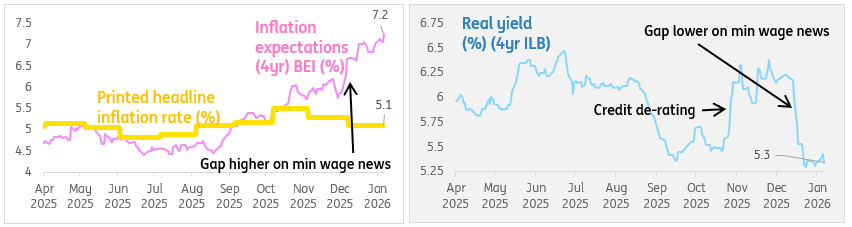

First and foremost, the c.24% hike in the minimum wage announcement (30 December). That's huge, and well in excess of inflation plus productivity growth. It's also a one-off, effectively immediately. At the same time, it only directly affects some 10% of the workforce. Half of the rest earn more, but the other half in fact earn less (the 'informal' workforce). Still, it's had a material effect on inflation expectations – now at c.7% (based off the 4yr bond breakeven rate).

Second, inflation expectations were on the rise anyway; from September to November 2025, they rose from 4.5% to 6%. The intermediate events centred on heavy re-funding requirement focus (6% fiscal deficit). The backstory reflected a series of 2025 downgrades, and a lurch of ratings down to the BB zone. And over the prior two-year period, foreign ownership of local bonds had declined from 27% to 18%. Lots of this mushroomed through November, coinciding with higher real yields (credit de-rating) and an even larger rise in nominal yields (rising inflation expectations). See the charts further below.

Third, part of the negativity and uncertainty has been reflective of political fiscal (mis-)management, but also on prospective political circumstances through 2026. We're facing congressional elections in March and presidential elections over the summer, in what is quite a fractured political landscape. We don't call politics here, but we need to be cognisant of over and undershoot risks that can and tend to stem from them.

The net effect of this?

Alpha is determined by assessing what is discounted versus delivery, and acting as the delta starts to turn

Inflation expectations have topped 7%, versus a 3% target (or, in actuality, a 4% tolerance rate). Hence, the prognosis for Banco de la República (BanRep) policy is tighter. Now for the money question – by how much, and to what extent is the newsflow discounted?

Inflation expectations top 7%

Versus printed inflation on the left. Real yield on the right

(Inflation Expectations = Conventional Yield minus Real Yield)

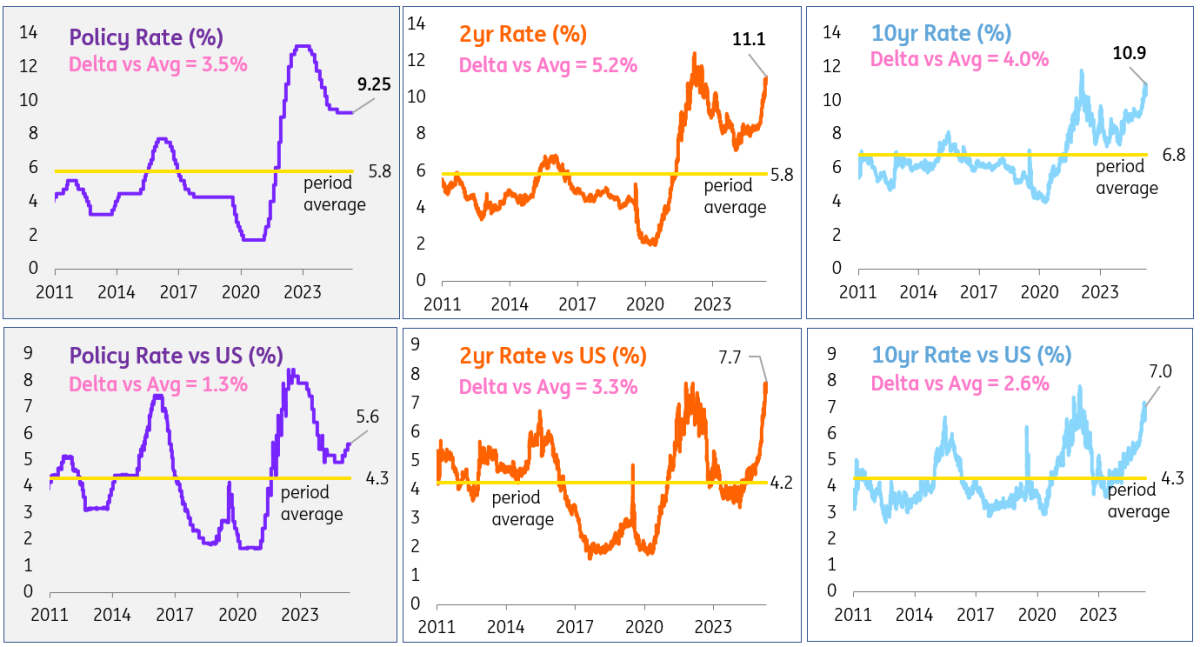

Market rates are well ahead of the Central Bank

BanRep's policy rate is currently 9.25%. We calculate the policy rate buffer as 1.8% (shown below), so policy is already moderately tight.

Policy Rate Buffer Calculation = 1.8%

Weighted average of:

- Policy rate differential versus the Fed (+1.3%)

- Domestic real policy rate (+4.3%) and

- Real policy rate differential versus the US (+1.1%)

Inflation expectations are running at 7%, which is 4% above the ideal 3% inflation rate. That argues for a policy rate buffer of 4%, and supports the logic that BanRep might indeed need to hike, by up to 200bp (taking the buffer to around 400bp, c.4%). That compares with the current market expectation for cumulative hikes in excess of 250bp.

Against this backdrop, the 2yr and 10yr swap rates are at around 11%. Prior peaks were in the area of 11.5% to 12% in late 2022 as BanRep was hiking, culminating in an official rate peak at 13.25% in early 2023 (charts below - upper three).

Our first observation here is the current 7% inflation expectation is well short of the prior inflation peak at above 13%; that, at first glance, suggests a less dramatic rate-hike requirement ahead.

Colombian market rates are many steps ahead of the Central Bank

Top charts show the absolute levels. Bottom charts show spreads versus the US

Spreads versus SOFR are already quite wide (good), and the peso quite strong (mixed blessing)

Our second observation is set with reference to where US rates are pitched (charts above – lower three). We find that Colombian market rates versus US SOFR rates are practically at prior peaks. In the 2yr, it's virtually at the prior peak, while for the 10yr it is only marginally short of the prior peak. That points to a lot of spread comfort already priced in.

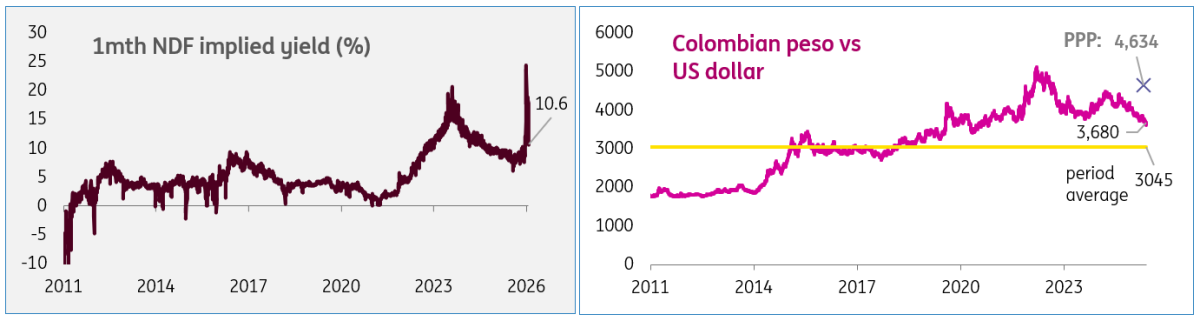

And then we have the FX angle, a third consideration. There is absolutely a positive carry story to be told here, as a robust part-rationale for Colombian peso prior strength versus the US dollar. With imports equating to about a fifth of GDP, that's not inconsequential as an additional element of comfort (from an import of inflation perspective).

At the same time, a significant official sector debt swap programme has resulted in residual peso buying pressure. As a bold stand-alone liquidity management policy, this has credit positives. And from a pure FX outcome perspective, it's helped the peso hold a remarkable bid in recent months. It's now trading quite rich versus a simple purchasing power parity calculation.

This is good, but with a twist. Prior peso strength could also prove a vulnerability, should it turn tail and decide to weaken. And the aforementioned political events through late first quarter and through the second quarter are the type of excuses that can stoke issues. Therein lie the biggest risks, together with unknowns that can stem from geopolitical gyrations, for example, vis-a-vis the US.

Colombian peso strength versus the US dollar of late - must be factored in

And the non-deliverable forward implied 1mth yield

Here's how to trade it

Bottom line, we think the central bank does indeed need to hike. But there is no need to materially panic with outsized hikes. Market rates have already paved the way, and currency moves have also acted to tighten conditions. The backdrop is one of US rate stability (with a medium-term Fed ambition to cut) and a softer dollar – that helps too. Had it not been for the elections coming in March and May, we'd actually be quite comfortable getting long Colombia.

As it is, we see three potential strategies:

- Get in now at reasonable levels, hold respective noses as we go through the probable election wobbles, and come out the other side with an ambition for Colombian market rates to be lower by year-end

- Or, wait for a better entry level as we venture through February and into the early March congressional elections, ideally with the prognosis of a policy-conducive outcome

- Or, average in from here. Do a bit now, so there is a long in place. And add to it should we get to 'better' levels in the weeks (and potentially months) ahead

In all cases, though, we're ultimately looking for an opportunity to get long again (probably from an existing short, in many cases).

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more