The next Bank of England rate hike may be smaller than you’re expecting

- 28 October 2022

- United Kingdom

Markets and most economists are expecting a 75 basis-point rate hike from the Bank of England on 3 November. But we think a 50bp increase is narrowly more likely. More importantly, we think the Bank Rate is unlikely to go above 4% next year. And that suggests that markets are overestimating the amount of tightening still to come

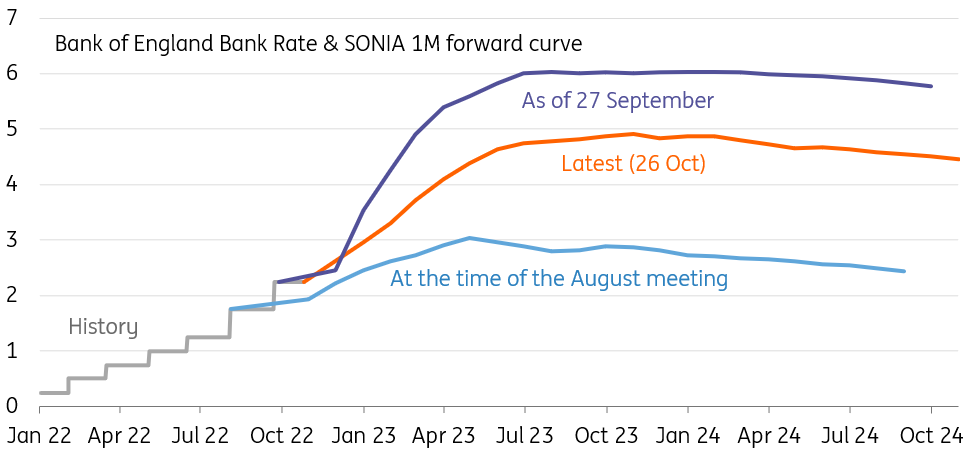

Investors have pared back rate hike expectations, but perhaps not far enough

It’s been a wild ride for Bank of England (BoE) expectations since September’s fateful ‘mini budget’. The resulting chaos in financial markets had prompted investors to, at one point, price in more than 150bp worth of tightening by the time of the November meeting. BoE chief economist Huw Pill spoke of the need for a ‘significant’ response.

Since then, UK markets have calmed, buoyed by the appointment of Rishi Sunak as prime minister and the steadier backdrop for public finances that is perceived to have ushered in. Markets have drastically scaled back expectations for November’s rate hike and are now pricing less than 75bp.

Having previously been among those looking for a 75bp hike, we now think 50bp has become narrowly more likely – though either way the committee is likely to be heavily divided. Consensus expects a 75bp move.

| 50bp |

ING's BoE rate hike forecast(vs. 75bp priced) |

The Bank of England is becoming more vocal about excessive hike expectations

It’s becoming increasingly clear that the Bank of England is uncomfortable with the amount of tightening markets are pricing. Investors still expect Bank Rate to peak around 5% next year. In a recent speech, BoE deputy governor Ben Broadbent suggested that GDP would take a near-5% hit over coming years if the Bank were to deliver that sort of tightening.

The Bank’s August forecasts – which themselves already pointed to a five-quarter recession – were based on a much lower terminal rate of roughly 3%. Citing a simple model, Broadbent suggests recent fiscal announcements warrant ‘only’ an extra 75bp of tightening on top of that.

It’s important not to take this too literally, but it’s nevertheless compatible with our long-standing view that Bank Rate is unlikely to go above 4%. Even Catherine Mann, one of the most hawkish committee members, was quoted saying recently that markets are “too aggressively priced”.

That frames the messaging we can expect from Thursday’s meeting. The new set of forecasts due, which crucially are based on market interest rate expectations, are likely to be dismal – showing both a deep recession and inflation falling below target in the medium-term. That should be read as a not-so-subtle hint that market pricing is inconsistent with achieving its inflation goal.

Markets still expect Bank Rate to peak close to 5% next year

Sky-high mortgage rates likely to outweigh concerns about a weaker pound

The obvious counter-point here is that the Bank’s forecasts have been sending this signal for much of this year – and the Bank hasn’t made much of an effort to otherwise talk down market expectations. Partly that's been because of mounting concerns about a weaker pound, and partly because of growing caution about the accuracy of forecasts as inflation has consistently outpaced expectations.

But this calculation is now changing. Not only does it look like inflation is close to peaking, but the risk of overdoing it with rate hikes is growing. Two-year mortgage rates hit 6.5% this month, and despite a fall in swap rates since the abolition of the 'mini budget', we suspect they’ll stay pretty high. Especially for high loan-to-value, lenders will either keep mortgage products off the market or build in more of a premium given the mounting risk of a house price correction. On a similar note, the Bank of England’s financial policy arm has also warned that small and medium-sized businesses are vulnerable given their heavier reliance on floating-rate borrowing.

Given the choice of hiking aggressively and baking in – or even pushing up – these borrowing costs, or tightening more cautiously and risking a weaker pound, we suspect most policymakers will lean towards the latter.

Inflation is close to a peak, though could stay 2-3pp higher from April 2023 if energy support becomes less generous

Five reasons for a 50bp rate hike

Admittedly none of what we’ve said so far necessarily precludes the central bank from hiking by 75bp on Thursday. Policymakers may feel the bank needs to reassert its authority after a chaotic few weeks. But here are five reasons why we think the committee will lean towards a smaller move:

First, the fact that we’re essentially back to square one on the mini-budget also reduces the pressure for a jumbo hike.

Admittedly the Bank finds itself in the awkward position of not knowing the full details of PM Sunak’s rewrite of the Medium-term Fiscal Plan. But the most consequential government action for the economic outlook has always been the Energy Price Guarantee, the cap the government has placed on consumer and business energy costs.

This had already been announced well before the Bank of England’s September meeting, where the committee resisted pressure to hike by 75bp. Indeed, we have since learned that the government has committed to making its energy support less generous (albeit we don't yet know how this will work).

In short, and with the notable exception of the cut in National Insurance, the expected boost from fiscal policy is similar to what was expected before September’s meeting.

Second, the economic dataflow doesn't provide a clear enough justification for more aggressive tightening. It's certainly true that the Bank's own surveys continue to point to chronic staff shortages and wage pressures, and this remains a key concern for the BoE. But the most recent inflation data was mostly as expected, while activity data has clearly deteriorated.

Third, trade-weighted sterling is actually now stronger than it was at the time of the September meeting. Concerns about depreciation we'd been seeing through the summer will have been a factor in the decision of three committee members to vote for 75bp at the last meeting. The latest market moves should alleviate some of these concerns at the margin.

Fourth, the Bank will be acutely aware that hiking by 75bp sets a precedent – it risks becoming viewed as the default move by investors, having only hiked in 50bp increments until now. At a time when the Bank is trying to talk down market rate expectations, that’s not ideal. With economic risks growing, the BoE will want to retain some optionality for future meetings.

Policymakers have also shown on more than one occasion now that they don’t feel pressured into a big move by what other central banks are doing. We’d therefore caution against assuming the BoE will hike by 75bp, just because that’s what the Fed and more recently the ECB have opted to do.

Finally, the committee is divided. While three members voted for a 75bp hike in September, one rate-setter – Swati Dhingra – voted for just 25bp. We think other committee members will remain reluctant to step up the pace of rate rises this late into its hiking cycle. That potentially heralds another three-way-vote-split on the committee on Thursday.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Scream if you want to go faster

- This bundle contains 7 Articles