Why a Bank of England 50bp rate hike could be a one-off

Even as the Bank of England gears up for a 50 basis point rate hike next Thursday, we think the window for further hikes is closing, as recession fears mount and supply side pressures show hints of easing off

How much longer can the Bank of England keep tightening?

We expect a 50bp rate hike from the Bank of England next week, its first such move this cycle. That’s not because the data we’ve received since June’s 25bp hike decision has moved the needle all that much – it hasn’t. But policymakers hinted back in June that they could act ‘forcefully’ to get inflation lower. And with a 50bp move more-or-less priced, that’s what we expect them to do.

Even so, the window for further rate hikes feels like it's closing. Markets have already pared back expectations for ‘peak’ Bank Rate from 3.5% to 2.9%, though that still implies two further 50bp rate hikes by December, plus a little more thereafter.

That still feels like a stretch. We’ve been pencilling in a peak for Bank Rate at 2% (1.25% currently), which would mean just one more 25bp rate hike in September before policymakers stop tightening. In practice, that might be an underestimate and depending on the signal the Bank sends next week, we wouldn’t rule out an additional 25, or at most 50bp, worth of rate hikes on top of that.

Here, we outline the key factors behind our relatively dovish base case for the BoE, as well as four things that could require us to pencil in a bit more tightening.

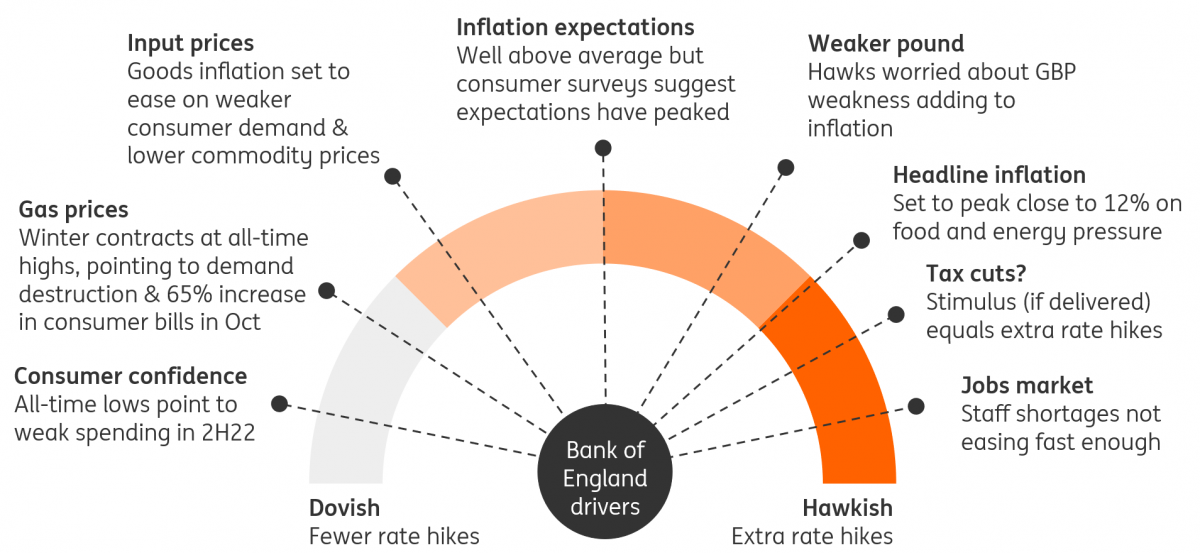

The Bank of England's dashboard

Key dovish factors and risks

Demand is weakening and a technical recession looks increasingly likely

Recession risks are clearly mounting, and that’s the most obvious reason for the Bank to stop tightening by the autumn. The end of Covid testing and an extra Bank holiday mean growth figures will be harder to interpret in the near term. But by the fourth quarter, we’re likely to see the full effect of the cost of living squeeze, not least because gas price contracts covering the winter period are comfortably at all-time highs. We also expect to see demand destruction, particularly in heavy industry. Much will depend on whether the government ultimately offers some form of compensation to energy-intensive industries that slow production, and whether consumer support is ramped up further in the autumn.

Supply issues appear to be improving – core inflation may have peaked

Headline inflation looks set to peak close to 12%, owing to another eyewatering, 65% rise in the household energy price cap in October, and rapidly rising food prices (which look set to exceed 15% year-on-year growth). Strip that out, however, and core inflation looks like it might have peaked. While this measure is unlikely to fall away much before 2023, there are signs that input price pressures are cooling. Some improvement in goods supply, and more importantly a reduction in reduced consumer appetite for these products, appears to be leaving retailers with excess inventory, a precursor to discounting. Throw in further falls in used car prices that are already down 8% since January, and there are good reasons to expect inflation to fall rapidly through 2023 – and probably end next year below target, crazy as that currently seems.

UK headline inflation set to peak close to 12%

Inflation expectations have moderated

If core inflation has peaked, so too it seems have consumer inflation expectations. The latest Citi/YouGov survey put 5-10 year expectations at 4%, down from a few months earlier, though unsurprisingly still above the pre-Covid average of 3%. For the hawks, the rise in expectations this year has been central to their calls for faster rate rises. Admittedly not everyone on the committee agrees, and the doves would argue these measures just reflect rises in visible prices like food and energy (something we’d tend to agree with). That logic might suggest the decline in expectations is a false dawn with gas prices rising, but if the trend in expectations continues, then we would expect the hawks to become less vocal.

Consumer-based measures of inflation expectations have fallen

The Bank’s own forecasts point to a lower terminal rate

Aside from everything else, the Bank has been telling us for months via its forecasts that markets are pricing in too much tightening. Its quarterly projections are based on swap rates, and in May these forecasts pointed to a fairly sharp rise in unemployment and sub-target inflation in two to three years if rates were to rise to 2.5%. Market rates are slightly higher than they were back then, so you’d assume the Bank’s new forecasts next week will send a similar signal.

Key hawkish factors and risks

Labour supply isn’t improving quickly enough

The upshot so far is that demand is weakening and supply may be starting to improve – a cocktail that should soon require less central bank tightening. But where that story could ultimately begin to break down is in the jobs market. There’s been no discernible improvement in hiring challenges, according to various surveys, including the Bank’s own Decision Makers Panel – something we know it puts a lot of weight on. Admittedly, the number of inactive workers has begun to fall and the jobs market is no longer tightening, but lower inward EU migration and a notable increase in long-term illness mean staff shortages are unlikely to be resolved quickly. Regular pay is still growing a little faster than it was pre-pandemic. We’d expect that to cool as firms' margins continue to be squeezed, but without further signs of labour supply improving, policymakers will remain concerned about domestically-driven inflation remaining elevated.

How economic inactivity has increased since the pandemic began

Strong jobs market should limit the scale of a downturn

If worker shortages persist, then we could see a lot of ‘labour hoarding’. In other words, companies have a strong incentive to avoid layoffs even as margins are squeezed, to minimise rehiring challenges. Unemployment could still rise, but so far there’s little evidence of that with redundancies at ultra-low levels. While that’s undoubtedly a lagging indicator at a time where energy prices continue to rise, it does suggest any increase in joblessness could be limited. And that means the hit to consumer spending over coming months can only go so far if workers largely remain employed, particularly when you factor in the scope for (admittedly higher-income) consumers to tap into savings built up during Covid. Indeed, it’s unusual that consumer confidence has fallen so dramatically in such a tight jobs market.

Note, too, that the Bank of England was already well below most other forecasters on growth expectations back in May, and further downward revisions seem likely next week. There’s a fair amount of damage already factored into the Bank’s thinking.

It's unusual that confidence is so low when the jobs market is so tight

Future tax cuts would provoke a stronger BoE reaction

Foreign Secretary and Conservative leadership candidate Liz Truss has promised cuts to both individual and corporate tax rates, which could total roughly 1.5% of GDP in additional stimulus, should she win the contest. On paper, that could lead the Bank of England to hike rates say 25-50bp further than it might otherwise have done, all else equal.

Weaker sterling and hawkish central banks globally add pressure to follow suit

The link between Bank of England policy and that of the Federal Reserve and European Central Bank is often overstated – something that we learned only last month when the Bank resisted the temptation to tighten faster the day after the Fed implemented a 75bp move. The committee has also shown in recent months that it isn't tied to what markets are pricing.

Nevertheless, the hawks have become more vocal about sterling weakness. The pound is down 10% against the dollar this year, though much less in trade-weighted terms. Wider rate differentials could add further pressure if, as we’re assuming, Bank Rate peaks 150bp+ lower than the Fed Funds Rate. Then again, our FX team’s models suggest other factors (like global risk sentiment) are bigger drivers of price movement. And anyway, the overall impact on inflation is unlikely to be that material in the context of other drivers. But it is one of the few inflationary aspects under the Bank’s control, and we suspect policymakers will be reluctant to allow a significant decoupling of UK-US (or eurozone) rate expectations – especially if the Fed were to go even more aggressively than most currently expect.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article