What to expect from Australia’s central bank next week

The Reserve Bank of Australia will probably say they'll keep rates as they are until all, not just most, of the evidence points to a hike. But we might not have too long to wait for that and asset purchases may soon be on the way out. Even if we get a hawkish tilt, the market's already hawkish pricing along with external woes should limit AUS/USD upside

Bye bye asset purchases?

The 1 February RBA meeting was always going to be an interesting one. Back on 7 September 2021, the statement accompanying the RBA's rate decision noted that the asset purchase programme would be extended until at least mid-February 2022, pushing a decision on any change on that policy to this forthcoming meeting.

It is worth just quickly rewinding to the guidance given at that meeting before seeing how far we've come since then. And back in September, the RBA maintained that:

"The Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 percent target range. The central scenario for the economy is that this condition will not be met before 2024. Meeting this condition will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently".

So barely 4 months ago, we were guided that there would be no rate hikes until 2024 on a central scenario - this itself was a slight watering down from the earlier guidance that even as late as June 2021 it took the line that 2024 would be the "earliest", that rates might be hiked.

Fast-forward to the last meeting in December and the guidance was very different. Gone are all references to any dates for rates liftoff:

"The Board will not increase the cash rate until actual inflation is sustainably within the 2 to 3 per cent target range. This will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently. This is likely to take some time and the Board is prepared to be patient".

It is actually the previous paragraph in the statement that deserves more attention though, as it sets out a blueprint for the RBA's reaction function. It states that:

"In reaching its decision in February, the Board will be guided by the same three considerations that it has used from the outset of the program: the actions of other central banks; how the Australian bond market is functioning; and, most importantly, the actual and expected progress towards the goals of full employment and inflation consistent with the target".

Let's take a look at these three considerations in more detail.

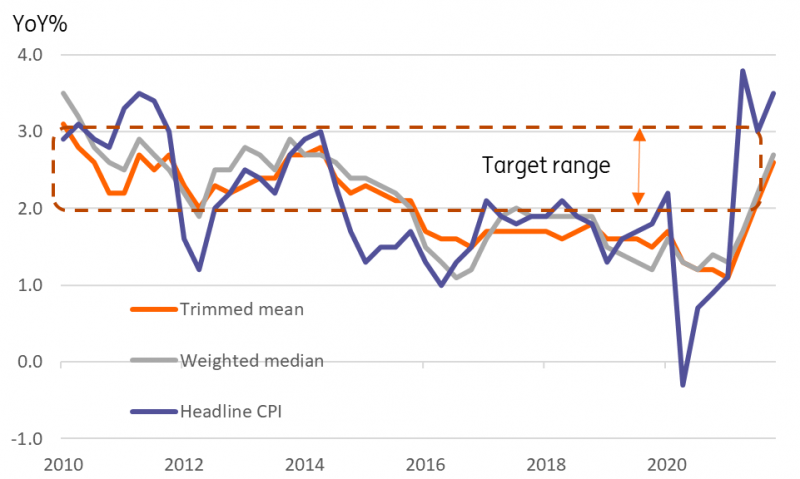

Australia inflation measures

The actions of other central Banks

If the underlying goal of the RBA has been at all times to be somewhat more dovish than the US Federal Reserve (our view), perhaps with one eye on the currency markets for the Australian dollar, then the goal-posts have shifted substantially. The last FOMC meeting teed up the Fed for a March rate hike. The Fed also indicated that they would be ending their asset purchase scheme soon after. The wonder is that the Fed didn't end QE on the spot this month, given that they have already acknowledged that their balance sheet is larger than it should be given the economic backdrop.

So that fact alone may give the RBA some room to taper further before an end to their own programme. This could be, say, by reducing the monthly asset purchase total from AUD4bn to AUD2bn, and then reviewing in May. That would leave a slightly ambiguous end to the programme, which might also be viewed as less disruptive for markets than an immediate end or a more definite end date. So that's the asset purchase scheme dealt with. But with the Fed clearly signalling a March hike, this opens up the door for a 2Q RBA hike, and further hikes over the second half of the year.

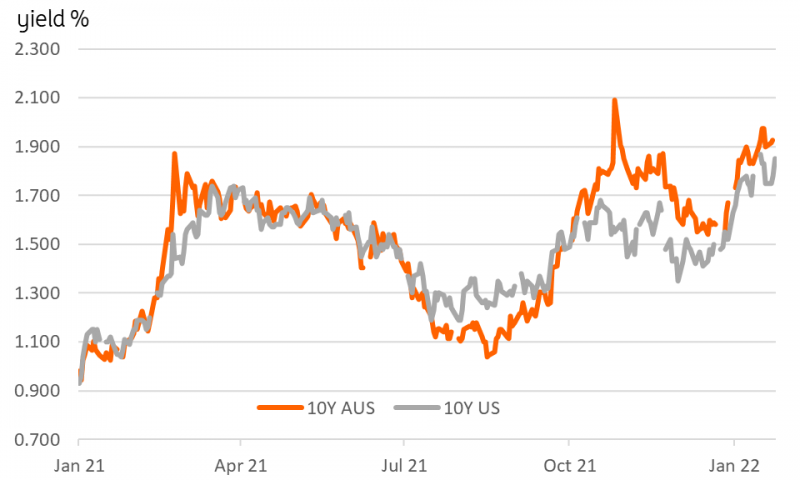

How the Australian Bond market is performing

10Y Australian government bonds currently yield a shade over 2%. That's up from about 1.52% in mid-December. but it is more or less in line with what we have seen in terms of US Treasury bond yields of the same maturity. Fighting the slight spread over US Treasuries is unlikely to be a constructive or effective approach to the Australian bond market, and in all fairness, a 2% yield is hardly a signal of a stressed government bond market, considering the growth and inflation backdrop, on which more shortly. As far as excuses to leave monetary policy unchanged, it looks as if the RBA can leave box 2 unchecked.

The actual and expected progress towards the goals of full employment and inflation is consistent with the target

As the RBA notes, this is the most important of the three reasons. And the 4Q21 CPI reading immediately suggests that it has been met, with a 3.5%YoY inflation print, above the top of the RBA's 2-3% inflation target range. That release was only slightly preceded by a sharp drop in the unemployment rate from 4.6% to 4.2%. Now if the RBA wants, it can note that at least some of the latest inflation increase is probably down to factors that are unlikely to persist (though the term "transitory" is looking somewhat cliched these days).

They can also note that trimmed mean inflation remains within target, as do weighted median measures - though both have risen substantially in recent quarters. What becomes much harder to ignore, would be evidence that wage inflation had also picked up to a level that might generate self-fulfilling inflation gains above the RBA's target.

The RBA Governor, Philip Lowe, last year gave a speech entitled "The Labour Market and Monetary Policy". In this, he provided two useful metrics. The first was that he believed that in order to consider the economy to be operating at full employment, the unemployment rate needed to be sustained in the low 4's. Well, we are there now, though it may need one or two months to persuade the RBA that this is "sustained".

The other metric was that to generate inflation consistent with the RBA's 2-3% CPI target, wage growth would need to exceed 3%. We get the 4Q21 Wage price index on 23 February - still a few weeks after this coming meeting. This is perhaps the only piece of the puzzle that remains absent from any argument for raising rates. But we will know soon enough. If the 4Q21 figure remains below 3%, then perhaps the RBA can put off raising rates a bit longer. If not, then a 2Q rate hike does become a possibility, as do further hikes in the second half of the year.

10Y Yields, Australia, US

Markets already there?

None of this, bizarrely, has all that much relevance for financial markets. Rates markets have been pricing in an aggressive series of hikes from the RBA for some time now. The implied yield on the December 2022 3m bank bill futures contract is currently 1.37%, which even allowing for some term premium over the cash rate is quite aggressive. And our longstanding view has been that although the RBA's forward guidance was likely to have to be substantially ratcheted back, so too would the market rate hike view. This leaves open the possibility of a counter-intuitive softening of market-rate expectations as the RBA walks back from its earlier dovishness.

While a key determinant of some major FX rates (EUR/USD, for instance) rate differentials have not been a major driver of AUD/USD in the past year, even after the RBA dropped the 2-year yield target: back then, the FX reaction was indeed more contained that the one in the bond market. In a similar fashion, the aggressive hawkish pricing of RBA tightening had a quite limited pass-through into AUD. Ultimately, AUD/USD has appeared to be pretty much glued to EUR/USD and global risk sentiment dynamics lately.

The link between FX and short-term rates may pick up once both the Fed and the RBA have initiated their tightening cycles, but for now, the weakness of this link means that hawkish signals by the RBA at next week’s meeting may provide only some time-limited support to AUD/USD, also considering the rates market is already pricing in around 120bp of tightening in the next 12 months.

A positive AUD reaction after the RBA announcement next week may largely be a consequence of some short-squeezing (AUD is the most oversold currency in G10), but the fragile global risk environment, strong USD, AUD exposure to China’s zero-Covid approach and unresolved Sino-Australian diplomatic/trade tensions all mean that a hawkish tilt by the RBA should fall short of truly revamping a strong bullish sentiment on AUD/USD in the near term. We continue to expect any AUD/USD rally to stall around 0.72 in 1Q22, with a balance of risk that remains tilted to the downside.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

27 January 2022

Looking forward to looking back This bundle contains 7 Articles