What US tariffs mean for the UK economy, rate cuts, taxes and trade

The UK is less susceptible to US tariffs, and not just because it was hit with a lower rate than its EU neighbours. But the impact of a weaker US and European economy could be much more significant. That'll make life harder for the Treasury in the Autumn budget and will help cement quarterly rate cuts from the Bank of England this year

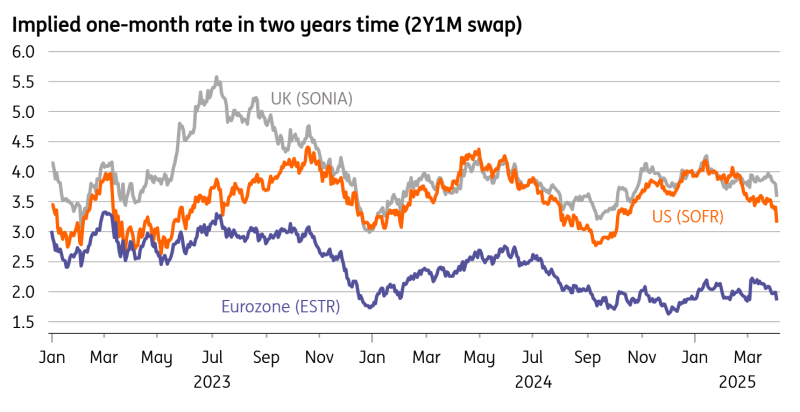

Financial markets have ramped up rate cut expectations

UK Prime Minister Keir Starmer has put a brave face on the US tariffs announcement this week. Financial markets, by contrast, seem much less sanguine.

Britain may have seen a more modest 10% tariff imposed compared to the EU’s 20%. But markets have staged a more dramatic repricing of Bank of England rate cuts than we’ve seen for the ECB. An extra 40-basis points worth of easing is priced over the next year, compared to ten days ago.

To steal a quote from Chris Turner's FX daily, Wednesday's tariff announcement has been a great leveller for global central bank expectations. Economies like the UK, where less aggressive policy easing had been expected over recent months, have seen more dramatic changes in rate expectations since Wednesday’s announcement.

Markets have repriced the Bank of England more than the ECB post-tariffs

What tariffs mean for UK growth

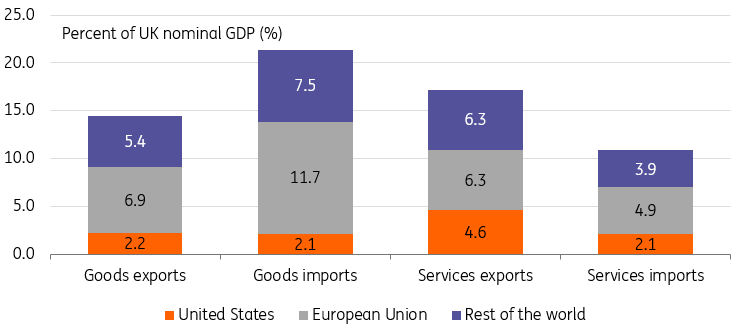

Perhaps that market reaction overstates the economic impact here in Britain, even though we think markets have been underestimating BoE rate cuts for some time. The UK is less exposed to President Trump’s trade war, at least directly. US exports account for 2.2% of UK GDP, where it is closer to 3% in the EU on average and nearer 4% in Germany.

Of course, it is a big deal for specific sectors: 10% of what Britain exports to the US is cars, while pharmaceuticals are also vulnerable to forthcoming tariffs.

Still, the overall hit from tariffs on Britain's GDP is perhaps only 0.2% or so. Certainly not enough to decisively change the outlook for UK growth. And remember there are some decent tailwinds for growth this year, notably from government spending.

Public expenditure is rising significantly this year, both for day-to-day and infrastructure. And for all the talk of cuts at the Spring Statement, spending is actually set to rise even faster across the next fiscal year than was planned back in October.

However, tariffs would be more problematic if the US and eurozone enter recession. That’s not our base case in either economy, though a slowdown would still be felt much more widely across the UK economy and potentially be a much greater source of downside.

The Office for Budget Responsibility (OBR) recently estimated that a 20ppt increase in the average US tariff charged globally – akin to what we’ve seen – could shave up to a percentage point off UK GDP, mostly from the secondary hit of weaker international demand.

We’ll be updating our forecasts next week, but we’re more likely to shave the numbers for late 2025 and into 2026. Before then, the much more immediate unknown is this weekend’s hike in Employer’s National Insurance (social security). It amounts to a 27% increase in the amount of tax paid by companies on an average employee’s salary. Survey after survey have shown it has lowered hiring intentions. So far though, redundancy notifications submitted to the government haven’t risen.

The UK is less exposed to US goods imports than the EU average

What tariffs mean for UK inflation

As for inflation, the fact that the government hasn’t retaliated to the US tariff announcement thus far means the impact should be minimal. And if anything, it could prove deflationary further down the line as economic growth cools and the threat of dumping from other big global producers rises.

The Bank of England has been wary about the forthcoming energy-driven rise in headline inflation from the 3% to 4% area and the ripple effects that might feed into service-sector prices. Services inflation is stuck around 5%, though we’re more confident than the Bank that this should come closer to 4% in the second quarter, assuming April’s annual price hikes prove more modest than a year earlier.

That’s principally why we expect the Bank to continue cutting rates once per quarter for the rest of this year. We don’t think the tariffs necessarily change that. But we have long felt that the Bank will take rates down to 3.25% in 2026. Markets are increasingly reaching this conclusion too.

What tariffs mean for the public finances

Tariffs undoubtedly make further tax hikes in the Autumn look even more inevitable than they already did. Remember Chancellor Rachel Reeves has only minimal headroom left over under her main fiscal rule, which requires a current budget balance by the end of the decade. And having changed the rules significantly last October, scope to do so again so quickly is limited.

Ultimtely, the public finances are operating on fine margins and it would only take small negative changes in the economic outlook to erase that £9.9bn fiscal headroom, just as we saw in March. Even before the tariffs arrived, we felt it was likely the OBR would have to revise down its medium-term growth forecasts, having only just bolstered them on the back of recent planning reforms. That downgrade now looks like a foregone conclusion.

We've argued before that we think the scope to cut public spending plans further is very limited, and if anything these may need to increase again later this year. That's why we expect further tax hikes to come through.

What tariffs mean for US and EU trade talks

All of this matters immensely when it comes to the UK’s negotiations with the US. The government hopes concessions, which might include watering down the Digital Services Tax (which raises £800mn annually) and changes to digital safety laws, will be enough to roll back the tariffs.

But the things that have held back a US-UK trade deal in the past - agricultural access for chicken and beef - look, if anything, more challenging to resolve than in the past.

That's because the UK is seeking a veterinary deal with the European Union, which would see the UK formally align with EU food/plant standards in exchange for removing border checks on these products. And that alignment could go further.

Labour is formally against joining a customs union or the wider single market for goods, but we wouldn’t be surprised to see movement in this direction. For all the Brexit drama, Britain hasn’t actually materially diverged in many – if any – areas of product regulation.

The UK trades much more intensively with the EU than US

Whether the EU agrees to all that is another story, but making concessions to the US in trade talks certainly could make it harder.

Starmer’s government faces a choice. And the reality is that it is much more likely to choose closer ties with Europe over America. Some of that is down to geopolitics and defence. But the government is also making a big priority out of driving up economic growth – and most importantly, making sure any policy announcements are recognised by the Office for Budget Responsibility’s forecasts.

The simple fact is that closer EU ties would have a larger economic impact than aligning more closely with the US economy – and by extension, those OBR forecasts. We’ve previously written how EU realignment might be worth an extra 0.1 to 0.2ppts on annual GDP growth in each year of the OBR’s forecast. That’s not a game-changer for the amount of headroom the Chancellor would have to play with, but it would help mitigate the downward impetus from weaker global growth.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article