What to expect from the US SEC’s proposed climate disclosure requirements

The US SEC is on the verge of setting hard rules on climate-related data disclosure that corporate issuers would need to abide by. They have not been published, but here we outline some key elements that we think will feature. The rules will enhance climate data standardisation and can accelerate the already rapid expansion of sustainable investing

With more companies voluntarily disclosing sustainability information and investors demanding higher quality sustainability data, the US Securities and Exchange Commission’s (SEC) Chairman Gary Gensler last week provided more clarity on the Commission’s long-awaited rules proposals, requiring companies to disclose various climate-related information. The chairman signalled that the SEC would set rules in tiers, meaning that different sizes of regulated entities will be required to comply with different types and levels of rules, likely through different timeframes.

The SEC is moving to make certain items of corporate climate disclosure mandatory.

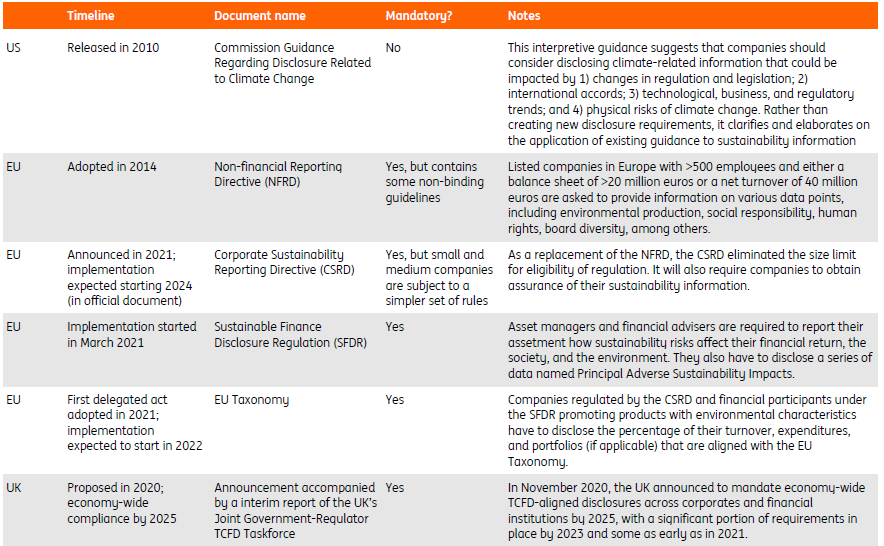

Another salient feature of the anticipated new rules is the shift from a non-binding guideline to binding requirements. The SEC published guidance on climate risk disclosure as early as 2010, but it is only interpretive and does not require regulated entities to report any specific climate-related data (see table below).

Now, the SEC is moving to make certain items of corporate climate disclosure mandatory. The SEC’s work is embedded in an administration-wide effort to better tackle the physical and transition risks of climate change in all sectors, including finance.

The rules are expected in the coming month or so. Here’s our take on what to expect:

Initial rules likely stricter for large companies

The number of entities covered by the proposed rules is a test of how broadly the SEC’s rules are to be applied. The more entities made subject to disclosure requirements the better, as that brings more sustainability data to the attention and scrutiny of all types of stakeholders.

As a comparison, the EU’s proposed Corporate Sustainability Reporting Directive (CSRD) will cover about 49,000 companies, including large listed and non-listed companies, as well as listed small and medium-sized enterprises. This is a major expansion to the bloc’s 2014 Non-financial Reporting Directive (NFRD), which applied to roughly 11,000 large companies that are listed.

The SEC has signalled the likely establishment of a different set of rules for large versus small listed companies, in a move similar to how the EU has approached disclosure requirements over the past few years. Small companies will likely be subject to fewer and less stringent disclosure requirements, and possibly none at all, partly as there is a cost burden involved, but also as smaller entities are typically less relevant from an issuance perspective.

Double materiality expected to come into play

Just as the EU requires for companies within its jurisdiction, the SEC will likely ask regulated entities to consider 'double materiality' – enterprise value creation (financial materiality) plus the “significant impacts on the economy, environment, and people” – when determining whether a piece of information should be disclosed.

The SEC will likely ask regulated entities to consider 'double materiality'.

The growing need to apply double materiality ties to the evolving interpretation of fiduciary duty, which suggests that long-term investment value drivers, which asset managers should take into account, include environmental, social, and governance issues (the classic holistic of ESG).

Both qualitative and quantitative disclosures are considered

The SEC has signalled that it will likely require companies to disclose both qualitative and quantitative sustainability data. From a qualitative perspective, information such as a company’s governance situation and strategies to address the physical and transition risks of climate change will likely be required.

The SEC is also mulling over mandating quantitative emissions data, though we expect that in the rule proposal, emissions disclosure requirements, especially for smaller companies, will primarily focus on Scope 1 emissions (see the table below for the definition). Scope 2 and Scope 3 emissions have been gaining attention, and pioneer companies have already been voluntarily reporting them, but requiring all regulated entities to report Scope 2 and 3 emissions could prove difficult, as they are complicated to calculate and there lacks a current consensus on sector-specific calculations for indirect emissions.

Definition of scope of greenhouse gas emissions

Disclosure could be required in 10-Ks and other public filings

Qualitative information, such as a company’s plans to address climate risks, emissions reduction technologies to reach net-zero emissions targets, and governance strategies related to climate, will likely be required for disclosure in the management discussion and analysis (MD&A) section of 10-K reports. Relevant quantitative data, such as emissions, will likely be required in metrics in one or more of the SEC public filings. Requiring climate-related qualitative information disclosure in the MD&A section will be relatively easier to implement, as the SEC's 2010 guidance has already be recommending. The important thing now is for companies to adequately apply the concept of double materiality mentioned above. Mandating quantitative climate data in public filings will be more complicated. The preferred form would be to issue line-item disclosure requirements that will together form climate data metrics. It is possible that the SEC pursues such an approach, but even if it does, the SEC will start with a very small set of requirements.

Implementation likely beyond 2022

According to the SEC, the new proposed rules could be released as early as this autumn, but the timeline of implementation is uncertain. We expect that the new regulation will likely be implemented beyond 2022, given that it would take time for the proposed rules to be finalised and sufficient corporate adaption time will be needed. Other jurisdictions have allowed several years of preparation before moving to the implementation phase. For instance, the EU released the CSRD proposal in April 2021 and expects to start implementation in 2024; the UK announced in 2020 to require disclosure aligned with the Taskforce on Climate-Related Financial Disclosure (TCFD), and expects the mandate to become effective in 2025.

Additionally, the SEC will likely work to ensure that the disclosure requirements are aligned with international standards such as the TCFD, whose principles are increasingly adopted by regulators and companies. Attention will also be devoted to the International Financial Reporting Standards (IFRS), which announced this year that it plans to set IFRS sustainability standards. The higher the alignment level is among these frameworks, the lower the compliance cost will be for companies and financial institutions.

Higher data quality, more effective capital allocation

C-suite executives will consequently face challenges and opportunities

The proposed SEC rules on climate disclosure will have a substantial impact on regulated companies. The disclosure requirements will put companies under greater scrutiny on how they manage their climate-related risks. Corporates will increasingly see their disclosed sustainability data examined against climate targets. C-suite executives will consequently face challenges and opportunities to improve their companies’ sustainable reporting schemes, which include setting up adequate reporting metrics, policy, and procedure; establishing internal controls; enhancing sustainability data assurance; exercising necessary board oversight; among others.

On a broader scale, through enhancing sustainability data standardisation, transparency, and comparability, climate-related disclosure mandates can more effectively allocate capital to companies or projects with higher performance or greater progress in managing sustainability. Mandated climate disclosure through regulations can benefit the sustainable finance market, where more credible data should help boost the confidence of investors in green and sustainability bonds and help reduce greenwashing perceptions (whether real or otherwise).

Challenges of greater disclosure on climate-related information also remain. Even if the SEC rules come in tiers, both large and small companies need to be prepared for higher costs – in terms of both financial and human resources – to monitor, gather, and report sustainability information. Moreover, mandating higher climate disclosure will sometimes lead capital to cleaner sectors that in general are better sustainability performers while ignoring hard-to-abate sectors that also need huge capital to decarbonise. That said, disclosure mandates could benefit from additional sector-specific guidelines that define sustainability and materiality, such as the EU’s Taxonomy and Sustainability Accounting Standards Board’s sector materiality map. Nevertheless, mandating the reporting of sustainability data is a first step towards appropriately addressing climate-related risks and improving the quality of sustainable investing.

Comparison of climate-related disclosure frameworks across jurisdictions

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article