What to expect from China’s monetary policy framework reforms

The PBOC has signalled that changes to China’s monetary policy framework may be on the horizon. We unpack China’s current monetary policy tools, analyse any upcoming changes, and report on their potential impact

PBOC governor's prompts speculation

Pan Gongsheng, the governor of the People’s Bank of China, gave a speech at the Lujiazui Forum on 19 June where he discussed the current monetary policy stance and the future direction of China’s monetary policy framework.

Governor Pan noted that certain central banks used the short-term operational rate as the main policy rate, and other interest rates may “soften their role.” This has led to discussion on whether the medium-term lending facility would be phased out as the main policy rate in favour of the 7-day reverse repo rate.

In the following weeks, the PBOC also made several announcements that signalled that this process was underway, including an expansion of open market operations to after-market hours and announcements that it would start to borrow government securities from primary dealers.

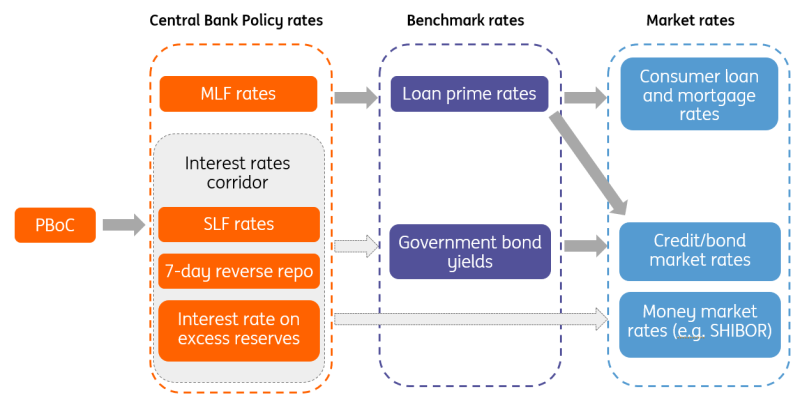

A look at some of China's key interest rates

China's current key benchmark rates and policy tools

Discussion of monetary policy framework and tools are often difficult to get your head around, even in the best of times, and central bank policy toolkits continue to expand. Rather than attempting an exhaustive list, here's a snapshot of the main policy rates and tools:

Key interest rates (priced-based instruments):

- Loan prime rate (LPR) – These rates are often seen as the “main rate” to watch as they are the benchmark for the majority of lending activity in China, with the 1 year rate linked to regular consumer loans, and the 5 year rate linked to mortgage loans. The National Interbank Funding Centre (NIFC) under the PBOC calculates this rate by taking quotes from 20 commercial banks on their respective prime lending rates. The LPR is derived after removing the top and bottom quotes and then taking the arithmetic average of the remaining quotes.

- Medium-term lending facility (MLF) – this is currently the PBOC’s main policy rate, set monthly. The MLF is the rate at which banks can borrow from the PBOC for a 1-year term utilising qualified collateral. The PBOC sets this rate, which typically then has a direct impact on commercial banks’ loan prime rates, updated several days later. In 1H24, there was RMB 2.29tn of volume through this facility. The PBOC sets the MLF rate, but banks take the initiative to utilise the MLF.

- Reverse repo rate – this is the short term policy rate for the PBOC, and is the rate at which the PBOC purchases government securities from commercial banks, with an agreement to sell them back in the future, thereby providing banks with short-term liquidity. The most common term is 7 or 14 days, though longer durations are occasionally used. This rate is lower than the standing loan facility, which allows for a broader pool of assets (including corporate bonds, green bonds, etc.) to be used as collateral. Governor Pan’s comments indicate an intention to feature the 7-day reverse repo rate as the main policy rate in the future.

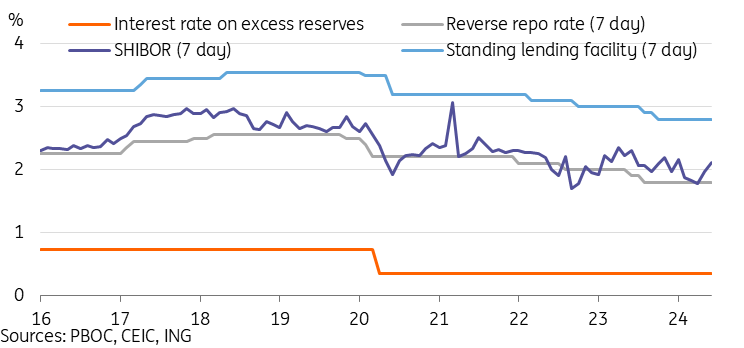

- Interest rate corridor: the interest rate corridor represents the upper and lower bound for market interest rates; the ceiling and floor represent the rates at which banks could borrow from and lend to the central bank, which has the least counterparty risk. The standing loan facility and interest rate on excess reserves form the interest rate corridor for China. The 7 day reverse repo rate is the policy rate, while the 1 week Shanghai Interbank Offered Rate (SHIBOR) is the market rate which both fall within this corridor.

- Standing loan facility (SLF) – on its inception in 2013, the SLF provided 1-3 month loans to commercial banks. These days, overnight and 7 day rates are available, and this represents the ceiling for the interest rate corridor. Use of the SLF is low relative to the MLF.

- Interest rate on excess reserves – this is the interest rate banks receive for depositing excess reserves at the central bank, and as that is a risk free option, it represents the floor for the interest rate corridor.

- At the time of writing, the 7 day SLF rate was 2.80%, while the interest rate on excess reserves was 0.35%. This corridor is quite wide compared to what is seen in most other countries.

Quantitative Instruments: the PBOC uses its balance sheet to adjust the monetary base and liquidity conditions. Historically the PBOC aimed to target specific quantitative goals for M2 and aggregate financing.

- Required Reserve Ratio (RRR): the PBOC requires banks to hold a certain amount of their reserves at the central bank. Adjusting this ratio affects how much money banks are able to lend out. The effectiveness of this tool depends on if there is pent up borrowing demand.

- Open Market Operations (OMO): the PBOC conducts open market operations in the form of repos and reverse repos as necessary in order to influence interest rates and liquidity in markets. These are primarily short term operations, and the 7-day reverse repo rate is the main rate for OMO, but the PBOC has signalled it wishes to expand to trading of longer term securities as well. In OMO, the PBOC takes the initiative.

Structural instruments: the PBOC also extends lending facilities to financial institutions and policy banks in order to facilitate special loans (green loans, innovation loans, infrastructure loans, micro & small business loans, etc.). One large structural instrument is the pledged supplementary lending programme, which had RMB 2.82tn of outstanding loans at the end of June 2024. Additionally, the PBOC also sets various special interest rate policies, including mortgage rate floors.

The above listed tools are the PBOC’s main levers, but are by no means exhaustive. An English translation of a PBOC paper with more details can be found here.

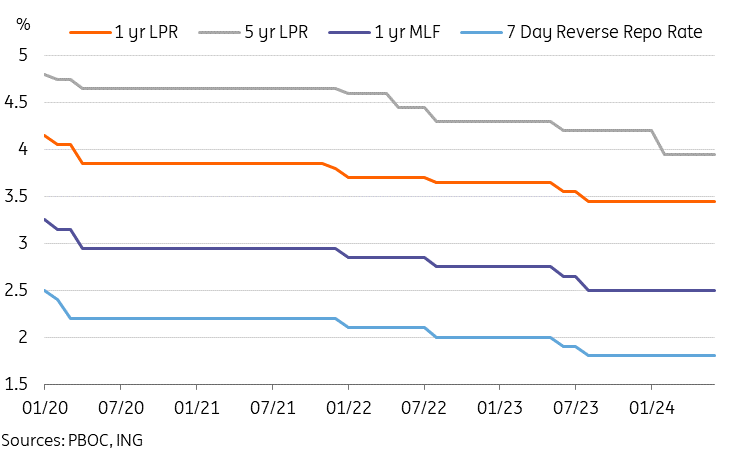

China's key interest rates have been on a gradual easing trajectory in recent years

What changes are coming and why?

The primary aim of monetary policy reforms is to improve policy transmission and allow the central bank to more effectively impact actual market interest rates. Currently, the MLF is effective in impacting the medium-term market rates denoted by the LPR, but short-term rates often fluctuate from the 7-day repo rate, the PBOC’s short-term policy rate. Given China’s relatively wide interest rate corridor, this fluctuation can sometimes be notable.

Details are still sparse at this stage, but Governor Pan’s comments indicated that the future monetary policy framework will gradually shift toward targeting short-term interest rates. He noted that the 7-day reverse repo rate basically fulfilled this role currently in China, implying that this will be the main policy rate moving forward. Policy communications may gradually shift to emphasise the 7-day reverse repo rate over the MLF as the primary policy rate.

Recent announcements indicate that we will likely see more frequent open market operations to better manage the short-term interest rate to track closer with the PBOC’s target rate instead of fluctuating within the larger interest rate corridor.

As part of this reform, the PBOC also aims to improve the transmission mechanism from short-term interest rates to long-term interest rates. The addition of government bond trading as a new policy tool will likely allow the PBOC to exert some influence on longer-term yields as well.

One common question after this announcement was if adding bond trading to the policy toolkit entailed plans for yield curve control or quantitative easing. It is more likely that these policy levers will be primarily used to manage liquidity and rein in excessive market movements rather than as a form of stimulus like the QE or YCC policies seen in developed market central banks. With that said, the addition of this policy tool does open the window for this sort of action in the future if needed.

Another frequent question was if the policy shift meant we would see the MLF phased out or retired. This discussion is mostly due to Pan’s comments that “other interest rates” would “soften their roles” as policy rates. However, the MLF remains quite an important tool for medium-term financing; at the end of 1H24, there was RMB 7.07tn of MLF outstanding, and there was RMB 2.29tn of volume in the first half of the year. As such, even if it is no longer the primary policy rate, we expect the MLF will remain a relevant tool and any phasing out would be gradual.

The PBOC also stated that it would like to reform and improve the LPR to better reflect actual market interest rates given to clients. We have not yet seen details on how this might be achieved, but the concern was that actual prime rates given to clients did not always match the LPR banks quoted to the NIFC.

Finally, the PBOC indicated that it would gradually weaken its focus on quantitative targets. Currently, monetary policy targets M2 and aggregate financing. Rather than sticking to quantitative targets, the focus is likely to shift toward price-based targets, i.e., market interest rates.

There is no timeline given for these changes, and we expect the process will be gradual in order to avoid disruption to markets.

China currently has a wide interest rate corridor and short term market rates occasionally diverge from the policy rate

What impact will these changes have on markets?

Assuming adjustment to the monetary policy framework continues in a transparent and gradual manner, it is likely that the market impact will be limited.

- Monetary policy direction to be unaffected: Historically, adjustments to China’s key interest rates have mostly moved in synchronization, so a focus on a specific rate should not change the overall policy direction.

- Expanded PBOC open market operations to reduce volatility of short-term rates and bond market:

- If the focus shifts to short-term interest rates, more active open market operations to narrow the interest rate corridor could reduce volatility in short-term market rates. SHIBOR should track closer to the reverse repo rate if the PBOC is successful in these efforts.

- Adding trading of longer term bonds to the policy toolkit also gives the PBOC an option to intervene when it deems the market is moving in either extreme. Currently, where the PBOC is now borrowing government bonds to sell, in a vacuum it adds upside pressure to yields via direct selling as well as impacting market expectations. In practice this pressure may not be enough to offset other factors.

- No change expected to top-level RMB policy: markets have been discussing whether or not the PBOC’s framework shift or the possibility of tariff hikes under a Trump administration would trigger a dramatic shift in the PBOC’s exchange rate policy. Governor Pan reiterated that “the ultimate objective of China's monetary policy is to maintain the stability of the currency value and thereby promote economic growth”. This is in line with previous guidance that policymakers see a stable RMB as being conducive for China’s long-term growth priorities, and implies no departure from the current stance.

- No disruption to MLF borrowing: We are not expecting a sudden sunsetting of the MLF, so banks needing to utilise this facility can continue to do so and there should not be a disruption on this front.

Adjustments to central banks’ policy rates occasionally happen as policymakers review their policy toolkit, and it is not unprecedented but occurs relatively rarely. Usually there is sufficient communication ahead of major changes that the end impact does not cause too much uncertainty or volatility.

Longer term, these reform measures aim to improve the market-based system for interest rate regulation, and give the PBOC more flexible tools to affect market rates. If successful, these reforms can improve monetary policy transmission in China.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article