What next for Brexit with 30 days to go

The threat of a Brexit delay puts pressure on Brexiteers to rally behind the Prime Minister's deal, although we still think Theresa May faces an uphill battle to get her agreement approved. This means an Article 50 extension looks increasingly likely, but crucially we may not know for sure until days before the 29 March deadline

What happens next

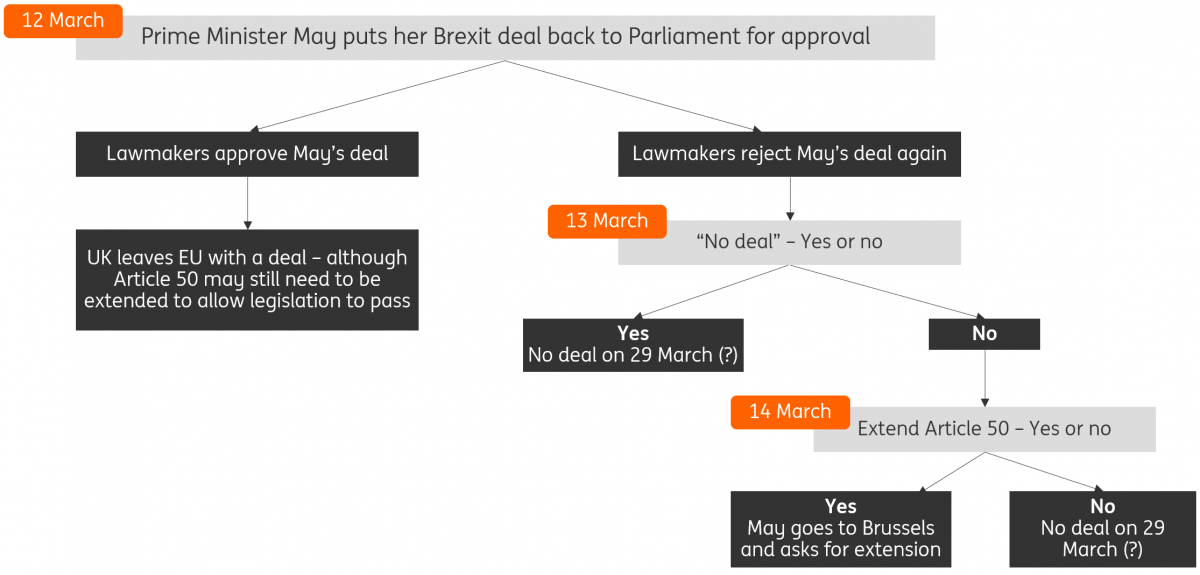

The big news this week is that Prime Minister Theresa May has ceded to pressure from a cross-party group of lawmakers and has laid the groundwork for a possible Brexit delay.

The PM has promised MPs a final meaningful vote on her Brexit deal by (or more likely on) 12 March. If the deal fails to gain approval, then she will return the House of Commons the next day to ask lawmakers whether they would like a ‘no deal’ Brexit. While MPs rejected an SNP-led push to symbolically rule out a 'no deal' Brexit on Wednesday evening, it still seems very unlikely that lawmakers would actively vote for this outcome.

Assuming then that the answer is a resounding “no” to 'no deal', the Prime Minister will return on 14 March to give lawmakers a vote on extending the Article 50 period. Judging by the latest round of Brexit votes on Wednesday, it’s likely that MPs would back a delay – although of course, as this vote is still two weeks away, we won’t know for sure until much closer to the 29 March deadline. There's also still plenty of uncertainty surrounding how long a delay would last, although it seems that the wind is currently blowing slightly towards a shorter extension (at least on the UK-side of the equation).

With all of this in mind, there are two questions worth asking: 1) Does the threat of a Brexit delay make it more likely MPs will back May's deal after all? and 2) With the next set of Brexit votes still two weeks away, what does this all mean for the economy?

The road to a possible Brexit delay

Despite the threat of a delay, May still faces an uphill battle to get her deal approved by Parliament

Now that the road to an Article 50 extension had been partially laid, there's a lot of debate over whether it is now more likely that the Prime Minister's Brexit deal will be approved after all. For many Brexiteers, the idea of a delay to the 29 March deadline is very unpalatable, and the looming vote on extending Article 50 could prompt some MPs to start re-considering May's deal.

Renewed chatter about a second referendum over coming days may also weigh in on the decision facing the Brexiteers. Following Parliament's rejection of Labour's preferred customs union strategy on Wednesday evening, all eyes are on the main opposition party to see whether they will endorse a second public vote, as had been hinted earlier this week. Admittedly there still appears to be some reluctance from Labour Leader Jeremy Corbyn to go down this route, and officially the party are still keeping a range of options on the table.

Either way, the pressure appears to be building and there have been signs that some members of the hardline European Research Group (a caucus of pro-Brexit Conservative MPs) may be looking for a ladder to climb down. Jacob Rees-Mogg, head of the ERG, suggested to the Financial Times that he'd be "quite happy with an appendix" which put forward some legal fixes to his concerns on the Irish backstop. Previously he, like the Democratic Unionist Party (DUP), had said the backstop would need to go entirely if he was to be won over.

However, there a couple of reasons why it's probably too early to think the tide will suddenly turn in favour of May's deal before 12 March.

It's still too early to assume the tide will suddenly turn in favour of May's deal

Firstly, there's no guarantee that the EU will accept the legal changes the ERG and others are pushing for. In fact, the gap between the EU's position and the ERG's demands still seems fairly large - Brussels has said many times now that a hard end-date on the Irish backstop, or a unilateral exit mechanism, are both non-starters. That's partly because the EU cannot be fully sure these changes would be enough to persuade Parliament to suddenly swing behind the deal.

Secondly - and this is perhaps the key point - Theresa May appears to be leaning towards a pretty short delay, maybe only as long as two-to-three months. The Brexiteers will be acutely aware that not much is likely to change during this time, meaning 'no deal' remains on the table, and implying they may be tempted to sit tight for now and vote against May's deal again on 12 March.

The situation could begin to look slightly different though if the idea of a much longer extension (say 9-12 months) starts gaining traction. Many things could happen in that time, including perhaps a reversal of Brexit altogether. For the pro-Brexit MPs, this means that - in theory - there's a chance the meaningful vote on 12 March might be their last opportunity to enact Brexit at all.

As thing stand though, our feeling is that the Prime Minister will still find it extremely tough to get her deal passed by lawmakers in two week's time.

The economy will struggle until we know for sure Article 50 has been extended

While it looks increasingly likely that Brexit will end up being delayed, the important thing for businesses is that we may not know for sure until there is little more than one week to go until 29 March.

While it looks likely MPs would back an extension to Article 50 on 14 March, it can't be 100% guaranteed - and even then, it will still presumably take a few days for PM May to return to Brussels and gain the unanimous EU approval that is required.

In the meantime, firms are likely to accelerate their 'no deal' contingency planning. A recent Bank of England survey conducted in December/January suggested a number of companies are yet to implement (or in some cases, create) plans for a hard Brexit. On the specific issue of goods trade, the Department for Exiting the EU noted this week that of the roughly 240,000 companies that are estimated to have only ever traded with the EU, only around 16% have applied for the registration number they need to be able to complete customs declarations.

British firms still preparing for 'no deal'

These preparations come at a cost, and in the short-term, this planning process will continue to weigh on investment more broadly. Equally, as we inch closer to the deadline, the real-world impact 'no deal' will be increasingly felt too. To take one example, a week or so ago the Thalassa Mana container ship set sail from the UK to Japan. Given that the EU-Japan trade deal looks unlikely to be 'rolled over' for the UK in time for 29 March, the firms who have sent the goods on this ship and others like it, have no idea whether their products will be subject to additional customs or administrative costs upon arrival.

The upshot is that economic growth will continue to struggle over the next few weeks. What happens then largely depends on how long an extension to Article 50 lasts - we discussed this in more detail in a separate infographic

Meet the Thalassa Mana, the ship sailing into the unknown...

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

27 February 2019

In case you missed it: Meetings and deadlines This bundle contains 7 Articles