What banks can expect from the capital requirements regulation review

Talks over banks’ capital requirements aren't new and 2024 promises to be no different. Once the final CRR III policy has been approved, banks will need to take a range of actions to implement it before January 2025. A delay in the final policy or national regulators' preferential treatment position could result in a sequencing issue for European banks

The upcoming amendments to the European Capital Requirements Regulation (CRR) include several changes to banking supervision that have been adopted through the Basel III reforms. These changes aim to reduce the uncertainty related to discrepancies in the risk-weight assignment, increase the risk sensitiveness of the standardised approach and reduce the overall unequal risk treatment to enhance comparability between financial institutions.

While the reforms might strengthen trust in the European financial system, they also introduce significant changes to banks' capital ratio calculations and will modify the risk weight enforced on certain asset classes. These modifications will have an impact on financial institutions. However, the magnitude will vary depending on each institution’s asset portfolio, potentially negatively affecting certain banks. We thus deem it important to take a closer look at what the policy really entails.

The Capital Requirements Regulation in short

In the aftermath of the 2008 Global Financial Crisis, the European Union decided to strengthen the banking sector to better handle future shocks. The Capital Requirements Regulation (CRR) and Capital Requirements Directive (CRD) were first implemented in 2013 as the prudential regulatory framework for credit institutions operating in the Union. This prudential framework aims to enhance resilience in the event of severe stress in the sector. To do so, the CRR sets the adequate capital level that each bank must hold to limit insolvency. This capital requirement is calculated at the bank’s aggregated level by assigning different risk weights per asset class, depending on the expected risk.

The capital ratio is calculated as follows:

The calculation of the risk weight is done either through the use of a standardised approach or an Internal Ratings-Based approach. Risk weights are set by the regulator and largely based on the international standards developed by the Basel Committee on Banking Supervision (BCBS), known as the Basel III standards. As holding more capital is hampering banks’ return on equity, setting global requirements is fundamental. Since its implementation, Basel III has already been updated to increase the quality and quantity of regulatory capital required. Following the Basel initiative, the CRR has evolved, reducing banks’ excessive leverage, increasing resilience to short-term liquidity shocks, and reducing reliance on short-term funding and concentration risk.

Basel Committee on Banking Supervision in a nutshell

The Basel Committee was established in the mid-1970s by 10 European countries in the hope of enhancing financial stability and improving the quality of banking supervision at a global level. The Committee now comprises 45 institutions from 20 jurisdictions.

Through the inclusion of three sets of frameworks (Basel I, II and III), the committee aims to reduce the gap in international supervisory coverage, thus ensuring that banks do not escape supervision and have adequate and consistent supervision across countries. Because holding greater capital negatively affects banks’ return on equity, harmonising capital requirements is essential to avoid a regulatory race to the bottom.

While Basel I and II focused on setting global standards for capital adequacy, Basel III was designed in response to the Global Financial Crisis. It reinforced the requirements stated in Basel II by not only enforcing stricter quality and quantity requirements on regulatory capital but also by implementing countercyclical buffers and even liquidity requirements. In 2012, the Basel Committee started to improve the calculation of capital requirements.

For countries part of the European Union, the Basel regulatory requirements must be translated into EU law to be enforced nationally. To do so, the Union drafted and enforced both the CRR and CRD.

In June 2019, the EU amended the CRR to implement the latest Basel III finalisation provisions. Amid increasing worries about discrepancies in risk weight assignments, mostly with the use of internal ratings-based models, and the belief that the standardised approach is not sufficiently sensitive to the riskiness of the underlying assets, the European Commission came up with a proposal to amend the existing CRR.

Legislative update

Since the Commission's proposal of a new CRR III was introduced in October 2021, it has been discussed at the European Parliament and the Council. The Trilogue negotiations reached a political agreement at the end of June 2023. This provisional political agreement will now have to be approved by the Economic and Monetary Affairs Committee and voted on in the Plenary. Finally, the Council will need to approve the document before it comes into force in early 2025.

The CRR has been evolving since 2013, following changes in the Basel agreements

What are the main changes in the CRR III?

The CRR amendments include several major changes to the current regulation. The following section will discuss the three main changes in our view and their expected impact on European financial institutions.

Inclusion of an output floor

Due to increasing concerns over the calculation of own funds requirements, the proposal makes changes to both the internal ratings-based and the standardised approach.

The most widely-discussed amendment of the CRR III proposal is the inclusion of a lower bound on banks’ capital requirements when banks use the internal ratings-based (IRB) approach. The current CRR allows some financial institutions to calculate their required own funds using internal ratings-based models. However, there have been growing concerns regarding the excessive variability in institutions’ own funds requirements with the use of these models. Indeed, banks might be inclined to underestimate their risk exposure and therefore also their own funds requirements. By amending this article, the EU is aiming to harmonise and limit the variability in own funds across countries and institutions, enhancing capital ratios’ comparability and reinforcing confidence in capital ratios.

Until the end of 2017, European banks were subject to the Basel I floor which required own funds calculated with internal models to be at least 80% of the one resulting from the standardised approach. The European Parliament's impact assessment highlighted several flaws in the enforcement of this floor due to the heterogeneity of risk weights and failures to reduce the variability across risk-weighted assets. To mitigate this, the current rules would require national supervisors to approve the use of internal models case-by-case, making the standardised approach the default calculation method.

To increase the consistency in the IRB calculation, the proposal sets an output floor (OF) to the internal ratings-based capital requirement when calculated by institutions’ internal models. This floor is set at 72.5% of the own funds requirements that would apply based on the standardised approach. Ultimately, this implies that financial institutions will be required to calculate both the IRB and standardised approach to make sure this output floor is respected.

This new minimum own funds requirement (also called Pillar 1) should be used at the parent level of the banks. To calculate this, institutions must calculate their Total Risk Exposure Amount (TREA). This ensures that institutions using internal models to calculate their TREA reach at least 72.5% of the TREA resulting from the standardised approach.

It results in applying the following equation:

As this change could significantly increase the own funds requirements for some banks using the internal rating method, the proposal includes a gradual enforcement of this new output floor. This amendment would make the 72.5% output floor fully functional as of 2030 and give approximately five years for banks to transition.

Output floor is expected to be enforced gradually as of January 2025

The impact of the output floor on institutions will vary significantly depending on banks’ main activities, justifying a gradual implementation to limit sudden shocks. Indeed, depending on the institution’s main activities, this new TREA floor could mean significantly higher own funds requirements.

Two asset types are expected to be significantly affected by the output floor:

Impact of the output floor on unrated corporate portfolios

With the new TREA calculation, institutions using internal models for their unrated corporates will now also have to calculate capital requirements through the standardised approach. The standardised approach for credit risk (SA-CR) requires the use of external ratings to determine the credit quality of the corporate borrower which typically doesn’t exist for EU unrated corporates. Furthermore, as own funds requirements for unrated corporates calculated under SA-CR are usually stricter than for rated names, the implementation of the output floor could substantially increase the own funds requirements for institutions with large unrated portfolios.

Additionally, the new regulation is changing the risk weights to be more granular. A risk weight of 100% for all corporates that don’t have any credit assessment available would be required. This could negatively impact the credit supply to unrated corporates as it would represent a significant increase in own funds required for banks. To avoid any negative impact, on top of the overall transitional agreement, banks are allowed to apply a preferential risk weight of 65% to their exposure to corporates that don’t have an external rating. This is subject to the condition that those exposures have a probability of default of less or equal to 0.5% (coinciding with an “investment grade” rating). This preferential treatment will only be in place until the end of 2032.

As the transitional period gives time to the regulator to make both higher capital standards and stable credit flow for unrated corporates coincide, several options have already been highlighted. The first, but rather unlikely option, would involve making corporate ratings mandatory. Considering the cost of rating all European unrated companies, this is not a likely option.

A second possibility would be to start developing national central bank ratings for corporates. This solution could fill in the gap left by forbidding banks from coming up with their own rating of unrated corporates. This option already exists in some jurisdictions like France.

Impact on real estate

The second type of asset under scrutiny with the amendment of the CRR III is real estate, more specifically mortgages. Indeed, the proposal makes a differentiation between types of immovable properties. Therefore, depending on the category of property, the risk weight associated with the exposure will vary. The first important criterion is whether the exposure is backed by a constructed and already available property or an acquisition, construction or land (ADC). For built properties, the policy also distinguishes between commercial real estate and residential.

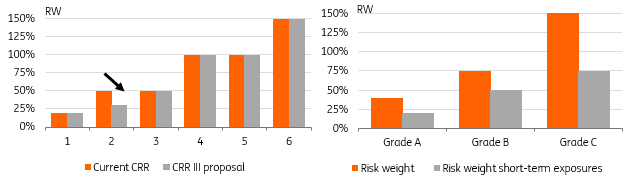

First, looking at residential properties, the current policy sets a risk weight of a minimum of 35% on properties occupied or let by the owner. That risk weight can be applied to a loan of a maximum of 80% of the market value of the house.

However, the policy states that the national regulator can apply a stricter risk weight but it should not be higher than 150%. If the <80% LTV conditions are not met, the risk weight applied should be 100%. This regulation allows for little differentiation in the quality of the collateral. Therefore, the CRR III amendments aim to enforce more granularity in the risk weights applied by looking in more detail at the exposure banks have to the property. To do so, it specifies different risk weights relative to the exposure-to-value (ETV).

The ETV is calculated as follows:

The proposal aims to implement six risk weights dependent on the property’s ETV

Aside from the increased granularity of the risk weight distribution, it also sets a lower weight for the best ETV ratios.

However, the Commission also proposes allowing national institutions to apply a different risk weight when deemed necessary. The stricter weights should not be higher than 150%. As mentioned before, the review of the CRR aims to align the European capital framework to the most recent updates of the international Basel standards. Some changes to the international capital standards are therefore not motivated by the European situation but by the situation in other countries. This is specifically the case for the change in real estate risk weights as some jurisdictions, such as the United States, are facing much higher default rates on their residential properties. These increased risk weights are less necessary for European countries where default rates remain low due to social benefits. Nonetheless, European banks will have to align with their international counterparts on these higher risk weights.

The implementation of a transitional agreement can be granted to banks by each European member state independently. The transitional period consists of a multiplying factor of the mandatory risk weight to reach the final risk weight by 2033.

The transitional period includes a multiplying factor on the RW

This multiplying factor increasing each year of 25pp to be 100% of the RW in 2033

National regulators might be willing to grant this preferential treatment if they deem their banks sufficiently protected against potential shocks. On the other hand, other countries might not want to allow such deviation from Basel III agreements as they might deem their domestic financial institutions’ buffers not sufficient. This could lead to competitive disadvantages across European jurisdictions. National regulators are expected to take a stand on this issue before the implementation of the CRR III revision but not before the final text of the policy is published. The impact resulting from such enforcement differences might be long-term and could seriously impact financial institutions with a large share of residential or real estate assets in their portfolio.

Turning to commercial immovable properties, the Commission's proposal follows the same idea as for residential assets by enforcing a more granular set of risk weights. The current policy calls for a risk weight of 50% for any loan fully secured by commercial real estate and allows national regulators to set a different rate up to 150% when deemed necessary. The new proposal makes a distinction between properties producing income (IPRE) and those not producing income (non-IPRE). For the latter, the proposed risk weight is 60%. However, for IPRE, the Commission proposes to differentiate the risk weights depending on the ETV of the property.

For commercial properties, risk weights vary depending on the ETV but start with a 70% RW

As with residential mortgages, the transitional period and the long-term risk weight will differ depending on the national legislator. Therefore, it could lead to national discrepancies and unfair competition by reducing the required own funds for financial institutions in certain jurisdictions.

The Commission also includes a specific category for exposure to land acquisition, development and construction (ADC) with a default risk weight of 150%. However, the ADC for residential purposes could benefit from a lower risk weight of 100% under certain conditions.

ADC exposure aimed at residential properties benefit from lower risk weights under certain conditions

Changes to the Internal Ratings-Based Approach

As discussed previously, the proposal’s main objective is to reinforce the comparability and confidence in risk weights applied by financial institutions to different asset classes. One of the main issues stems from the important variability in the IRB approach. Therefore, the proposal aims to limit the use of IRB and prioritise the SA-CR method. In addition to setting an output floor to the internal ratings-based methodology, the use of advanced IRB models will be replaced by foundation approaches for some portfolios like large corporates. It will also be only permitted for banks to use IRB under the condition of being granted pre-approval from the national regulator.

To further limit discrepancies in the use of IRB models, the Commission introduces input floors. The current version of the CRR includes an input floor for the probability of default to corporates or institutions of a minimum of 0.03%. This rate would be increased to 0.05% with the new legislation. The proposal is also implementing input floors for the loss given default (LGD) calculations of corporate and retail exposures.

Both corporate and retail exposure is reclassified to increase granularity and assigned a risk weight up to 25%

An input floor is also proposed for the credit conversion factor (CCF) which should be at least 50% of the off-balance sheet exposure not included in the revolving commitments calculated with the standardised method.

Changes to the standardised approach

The Commission’s proposal also includes a revision of the standardised approach for credit risk (SA-CR). It aims to increase the risk sensitivity and further widen its use, especially as the legislator wishes to reduce the use of the internal ratings-based approach (discussed earlier). The changes target three types of asset class: off-balance sheet assets, exposure to institutions and exposure to corporates.

Looking at the off-balance sheet asset class, the proposal adds an extra risk bucket, increasing the risk weight granularity. With the current CRR regulation, risk classes are distributed in a range of four categories between low and high risk with risk weights going from 0% to 100%. The new proposal would implement five buckets and change the risk weights so that even the least risky bucket applies a 10% risk weight whilst the highest remains at 100%.

This increase comes at a cost for most financial institutions as it will increase their provisions and could reduce potential revenues. Therefore, the Commission also proposes a transitional period to allow banks to slowly implement the new regulation (as discussed previously).

Regarding the exposure to institutions, the proposal also aims to increase granularity. In addition to the current requirement to get an external rating, the proposal introduces a standardised credit risk assessment approach (SCRA), requiring institutions to classify their exposure in three buckets. To do so, it makes a distinction between rated and unrated institutions. For rated institutions, the risk buckets are kept as they currently exist, but the risk weight is corrected lower. The change would also mean specific risk weights for unrated institutions.

Second bucket risk weight would be lowered with the enforcement of the proposal

Three new buckets will be created to classify and risk weight unrated institutions

Additionally, the regulation gets rid of the link between institutions and their sovereign by eliminating the option to link the risk weight to the sovereign’s rating. This could be beneficial for institutions situated in lower-rated countries.

Turning to corporates, the proposal keeps most of the risk weights identical to the current regulation, with the exception of one bucket that is lowered. To improve granularity, it introduces a risk weight for special lending exposures.

Third bucket risk weight would be lowered for both normal and special corporate lending

However, the main change for corporate exposure is expected to cascade from the implementation of the output floor (discussed previously), requiring financial institutions, that until now solely used the IRB approach, to also estimate their exposure using the SA-CR method. They would therefore potentially apply higher risk weights to their portfolio.

What is on banks’ agenda for 2024?

The implementation of the latest Basel reform at the European level has been a topic of debate for a few years already. Nonetheless, as we approach the January 2025 enforcement date, several important points remain unclear as the final version of the policy is still not available. It appears that 2024 will also be marked by a sequencing problem.

Indeed, the three points discussed earlier are based on the current proposal of the CRR reform. Firstly, several steps remain in the legislative process before the final version of the policy is amended and enforced. 2024 will therefore be crucial as the legislative process will come to an end.

Only once the final policy version is published will financial institutions be able to start making the necessary changes to their risk scenarios approaches. With the final version of the policy will also come the necessary technical implementation documentation. In some cases, these new methodologies must be approved by the regulator. Banks will thus need to act fast between the publication of the final CRR III and the enforcement date, to draft their new capital requirement calculation and get them approved by the supervisory authority.

Furthermore, the current proposal notes the possibility for national regulators to enforce a preferential transitional period for their domestic banks. It remains challenging to predict which EU jurisdiction will grant such preferential treatment to their financial institutions. Nonetheless, if such deviation from the Basel agreements is enforced, it could trigger a competitive disadvantage for the rest of the banks in the Union. Here again, 2024 will be crucial as we expect national regulators to disclose their stance only once the text is final and before its enforcement.

The sequencing problem will be enhanced by the delay in the UK and US enforcement of the Basel regulation. Both countries announced that their national implementation will not be enforced as of January 2025 but rather July 2025. This implies inconsistencies between jurisdictions for the first six months of the policy enforcement. This is not without consequence for some institutions such as investment banking and institutions heavily relying on international investments as they will have to comply temporarily with two different sets of capital requirement standards.

On the brighter side, European regulators seem to be willing to put an end to the capital requirement negotiations and start enforcing and monitoring the newly reviewed policy. Andrea Enria, chair of the Supervisory Board of the ECB alluded to it in his speech at the EUROFI 2023 financial forum: “Let’s move on from the debate on the calibration of capital requirements. Let’s implement the international standards we have all agreed on. And let’s focus on making sure that banks take the right corrective actions to address the shortcomings that their supervisors identify. It is in banks’ own interest to engage with us in this endeavour and make sure that, the next time market confidence dwindles, no weak links can be identified.”

Financial institutions still have a lot of work to do in 2024 to prepare for the enforcement of CRR III. But once this is in place, one can hope for a period of pure monitoring, making these changes the last major improvement in the European capital requirements regulations.

To conclude

Overall, the review of the current CRR will trigger three major changes for European financial institutions. The first one is the implementation of an output floor on the risk weights applicable to the IRB model. This will heavily impact the Union’s unrated corporates and real estate. The possibility to include a transitional period might help to smooth out the changes but at the cost of setting comparative disadvantages between jurisdictions.

The second important change relates to the implementation of an input floor when using the IRB and its usage limitation. Finally, the increased risk sensitivity of the SA-CR for certain asset classes will also affect the European financial sector.

Looking forward to 2024, banks will only be able to start implementing the new requirements once the legislative process is over. Once done, they will be able to look into technical requirements, getting some of their new risk processes approved. This might be challenging in such a short time before the official January 2025 enforcement date.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

19 October 2023

Banks Outlook 2024: A world of higher for longer This bundle contains 7 Articles