Weaker eurozone bank lending in August: perhaps just a summer lull

- 28 September 2021

- Financial Institutions

ECB August monetary data show weakening demand by eurozone businesses' for bank loans. Yet it is too early to sound the alarm

A strong start to the year has given way to a weak summer...

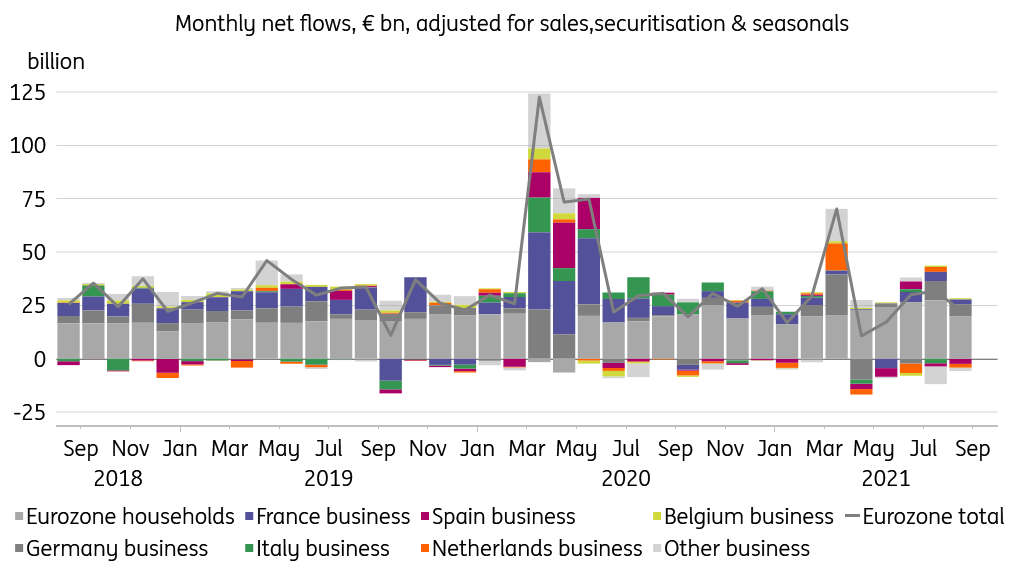

Eurozone net bank lending to households – over 70% made up of mortgages – decelerated somewhat in August after four very strong months (see chart below). In fact the €27.3bn of net lending in August was the highest monthly net lending since September 2007. Meanwhile, net bank lending to eurozone businesses was only €2.6bn in August. The first few months of this year showed some promising signs, even looking through the likely targeted longer-term refinancing operations (TLTRO) deadline-related lending spike in March. These promising signs included a bias towards longer duration loans, suggesting loans were used for investment purposes instead of e.g. working capital financing or cash management.

Eurozone bank lending to households and non-financial businesses

... with familiar rifts between countries widening again

Yet in recent months overall net lending to businesses has been slowing. We would prefer to explain the August weakness as a holiday-induced easing of activity, except that seasonal effects have already been filtered out of the data. That said, it is too early to draw any definite conclusions from just one weak month. In terms of business finance, we are in a transition period, coming from a situation of unprecedented government support, and moving (if all goes well) towards normalisation. We are likely to see more divergence in business borrowing demand between countries, as economies and government policies develop differently.

We are likely to see more divergence in business borrowing demand between countries, as economies and government policies develop differently

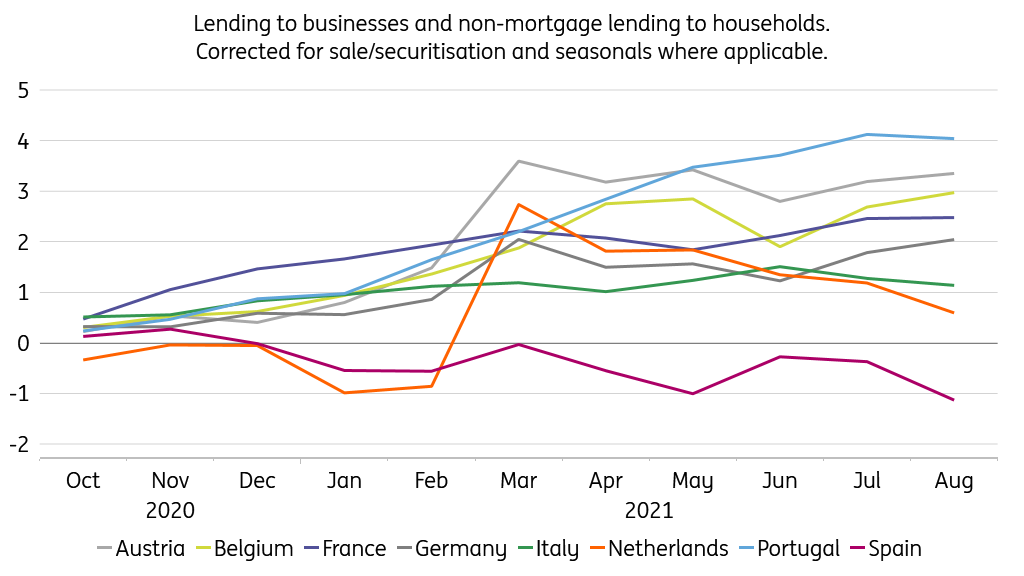

Such divergences have already become visible: Lending to Spanish businesses has been on a slightly negative trend since summer last year. While this can hardly be called good news, it is also a continuation of the pre-pandemic trend. In Italy, net business borrowing has been decelerating more gradually and is now hovering around zero – here too, little different from the pre-Covid years. In our opinion, France and Germany are the countries to watch in the months ahead. The general trend in both countries over the past year has been one of slightly below-pre-pandemic net borrowing. Whether borrowing in these countries will again reach or exceed pre-pandemic volumes, may tell us a lot about how eurozone businesses are emerging from 1.5 years of lockdown, and are dealing with today’s supply chain disruption issues.

A new TLTRO deadline has appeared on the horizon

As we are slowly moving towards the end of the year, banks will be looking at their TLTRO-relevant lending as well. To qualify for a favourable -100bp rate on TLTRO loans in the June 2021-June 2022 period, outstanding bank loans to businesses and non-mortgage lending to households on 31 December 2021 have to at least meet the volume on 1 October 2020. As the chart below shows, Spanish banks are in a challenging situation. Weak loan demand in Spain has caused their loan volumes to shrink 1% below the threshold. Other large economies remain above the threshold for now, though TLTRO-relevant lending in the Netherlands is trending down. That all said, we anticipate more action in bank lending towards the end of the year, given that companies will increasingly have to do without government support, which likely affects their borrowing decisions – positively or negatively.

Cumulative TLTRO-eligible bank net lending growth since October 2020 (%)

Decelerating money growth as governments hoard cash

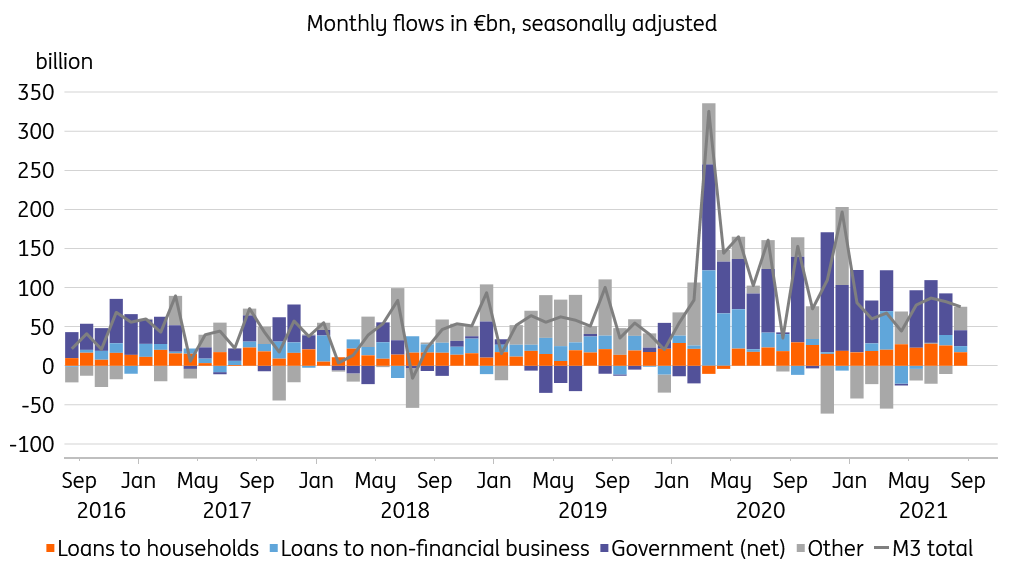

ECB data showed slightly decelerating M3 money growth in August. Weaker bank lending to households and businesses, as described above, plays a role in this. Yet the times when money growth was primarily driven by household and business borrowing, are long gone. The Eurosystem’s purchases of government bonds have been the main driver for years, and even more so during the pandemic. Eurosystem purchases decelerated in August, reducing money growth. What’s more, governments parked an additional €40bn of cash at the Eurosystem in August. From a bookkeeping perspective, these government deposits form a drain on money creation.

In any case, money growth will not be the primary place to look for clues about consumer price inflation in the months ahead. Yet elevated money growth will likely continue to contribute to inflation of asset prices.

Drivers of Eurozone M3 money growth

August’s monetary data are best interpreted as a signal to be alert: the relative strength of bank credit in the first half of the year, appears to have faded. The months ahead will have to make clear whether this is a temporary dip, or a more sustained break caused by phase-out of government support and supply chain disruptions. With over €10bn of favourable TLTRO rate revenues at stake, banks have a strong incentive to counter any weakness in lending demand.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more