WASDE update: USDA’s first crop estimates for 2023/24

The USDA’s first estimates for the 2023/24 marketing year present a soft outlook for corn and soybeans as global supply improves, whilst demand is expected to increase at a modest pace. However, the wheat outlook is more constructive with the market facing yet another fall in ending stocks in 2023/24

Supply gains outpace demand growth for corn

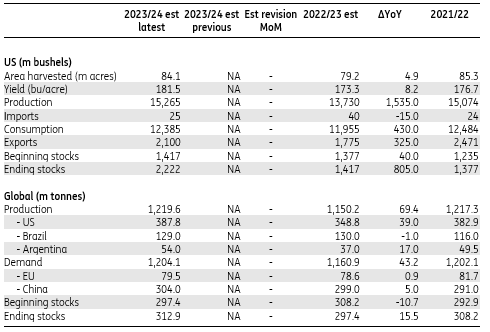

The USDA expects US corn production to rise significantly by over 10% year-on-year in 2023/24, with first estimates suggesting record output at 15.3b bushels due to improved yield and higher acreage. The market was expecting a number closer to 15.1b bushels. Corn acreage is expected to rise from 79.2m acres to 84.1m acres in 2023/24, whilst yields are projected to increase from 173.3bu/acres to 181.5bu/acres. US domestic demand and exports are expected to rise by 430m bushels to 12.4b bushels and by 325m bushels to 2.1b bushels, respectively. Consequently, US ending stocks for 2023/24 are estimated at 2.22b bushels, up from 1.42b bushels at the end of 2022/23. The market was expecting a number closer to 2.1b bushels.

For the global corn balance, world production is estimated to total 1.22bn tonnes in 2023/24, up 6% YoY. Supply gains from the US (+39mt), Argentina (+17mt) and the EU (+11.3mt) are expected to more than offset supply losses from Ukraine (-5mt) and Brazil (-1mt). Global ending stocks for 2023/24 are projected at 312.9mt, up by 15.5mt from the previous year. This is also higher than the roughly 308mt the market was expecting.

Above-consensus ending stock numbers are clearly not constructive for corn prices and this is aligned with the relatively more bearish view we have held for corn. However, there are still clear upside risks as we move into the US growing season, whilst there is also still plenty of uncertainty over the extension of the Black Sea Grain Initiative.

Corn supply/demand balance

Soybean market well supplied in 2023/24

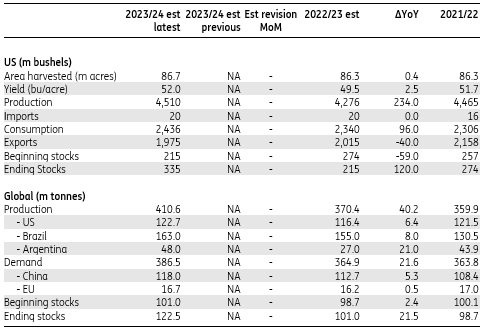

2023/24 estimates for US soybeans were bearish with increased supply, higher ending stocks and lower exports compared to the preceding year. The USDA projects US soybean ending stocks at 335m bushels, much higher than the 215m bushels estimated for 2022/23. This is also well above the 293m bushels the market was expecting. US soybean production is seen at 4.51b bushels in 2023/24, up from an estimated 4.28b bushels in 2022/23, primarily due to higher yields. US exports are projected to decline by 40m bushels to 1.98b bushels following increased overseas competition. Meanwhile, USDA projects US soybean demand at 2.44b bushels, up 4% YoY.

For the global market, the USDA estimates production will jump significantly, following higher production estimates from South America and the US for 2023/24. The agency forecasts global soybean production to rise almost 11% YoY to 410.6mt (+40.2mt YoY) with higher supplies coming from Argentina (+21mt), Brazil (+8mt), the US (+6.4mt) and Paraguay (+1.2mt). Meanwhile, global soybean demand is expected to increase by 6% YoY to 386.5mt with demand growth mainly coming from Argentina (+5.5mt), China (+5.3mt) and Brazil (+2.7mt). Global soybean ending stocks are estimated at 122.5mt for 2023/24, compared to 101mt from a year ago and market expectations of around 108mt.

Overall, the release was bearish for soybeans with both US and global ending stocks coming in above market expectations. This also gives us comfort in our more bearish outlook. But obviously, there are still risks heading into the US summer.

Soybeans supply/demand balance

Wheat balance to tighten further

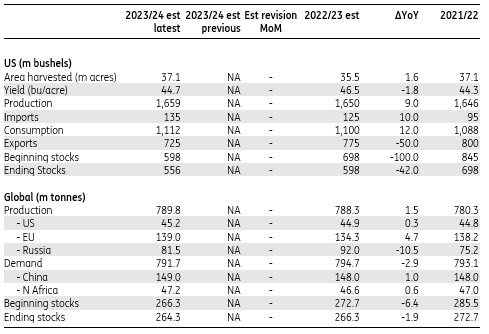

The USDA expects US wheat ending stocks for 2023/24 to fall by 42m bushels (-7% YoY) to 556m bushels, the lowest in 16 years. The market was expecting a number closer to 602m bushels. US wheat production is estimated at 1,659m bushels for 2023/24, marginally higher than the 1,650m bushels seen a year ago due to the increased area. However, it is still below market expectations of 1,812m bushels.

Global wheat ending stocks are forecast to total 264.3mt for 2023/24, slightly lower than the 266.3mt estimated for 2022/23 but above market expectations of around 260mt. Global wheat production projections were seen at 789.8mt, up 1.5mt from 2022/23 estimates. The increase in supply from Argentina, Canada, China, the EU, and India was partially offset by declining output from Australia, Russia, Ukraine, and Kazakhstan.

The WASDE was somewhat bullish for wheat prices given the large drop expected in US ending stocks for 2023/24. However, developments related to the Black Sea grain deal will also be crucial for price direction.

Wheat supply/demand balance

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article