Voluntary carbon markets are changing for the better

After years of wavering, voluntary carbon offsetting schemes are likely to be back on the agenda of corporate decision-makers. Here's a reminder of what corporate leaders need to know before considering whether to use them or not

Why carbon offsetting makes sense for corporate decision-makers

Currently, most mandatory carbon pricing schemes, like the EU Emissions Trading System, apply to the power sector and manufacturing. We unravelled the economics of these schemes and why they matter for corporate decision-makers here.

But many companies are not part of mandatory carbon pricing schemes, like retailers, wholesalers, contractors, carriers, farmers. They too want to make their businesses more sustainable, and an increasing number is committing to net-zero emission strategies.

In some of these industries, particularly outside the power sector and manufacturing, the cost of reducing emissions with today’s technologies might be prohibitively expensive or impossible.

That’s precisely where offsetting schemes could play a role in achieving a company’s voluntary climate objective: neutralising residual emissions that are still deemed unavoidable today until a technological alternative becomes available on the market. In the absence of mandatory carbon schemes, they can participate in voluntary carbon markets. These voluntary carbon markets have recently attracted a growing number of entrants such as oil companies alongside companies like Alphabet or Disney, which have been using carbon offsetting for many years.

How voluntary carbon markets work

So, voluntary carbon markets allow corporate leaders to offset carbon emissions that can only be reduced at a high cost or to offset unavoidable emissions. It works by purchasing carbon credits aimed at averting greenhouse gas emissions or permanently removing them from the atmosphere – typically by planting trees, the most popular type of offset project.

Such offsetting schemes are ‘voluntary’ and unregulated, unlike ‘compliance’ markets such as the EU’s Emission Trading System (ETS), with legal obligations and public interventions to push prices up.

Voluntary carbon credits, which are also referred to as offsets, are financial tools issued by project developers that avert or remove GHG emissions from the atmosphere. Each offset must demonstrate that one ton of CO2 (or equivalent GHG) has been averted or removed from the atmosphere.

For a carbon reduction project to generate credits, it needs to respect a set of criteria certified by independent standard-setters like Gold Standard or Verified Carbon Standards (Verra). Once the credits are generated, they can be either traded over the counter or used towards a corporate climate target. The price of a credit is originally determined by the cost of the offsetting project, and to a large extent, by supply and demand.

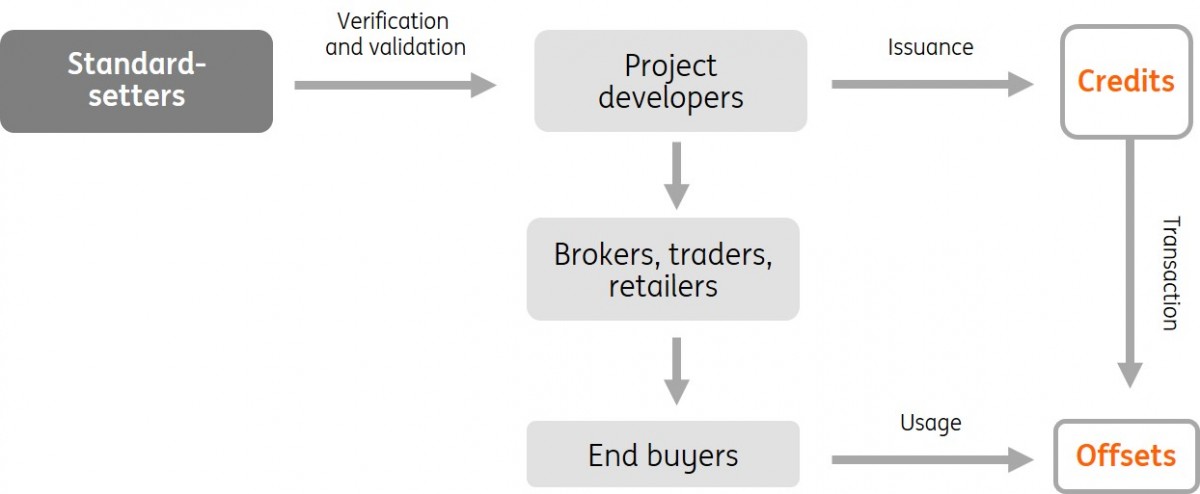

Four types of participants make up voluntary carbon markets

Schematic overview of voluntary carbon market

Credibility is the key challenge

Concerns over the quality and the integrity of carbon offsetting schemes have plagued them since their early days, some 20 years ago following the Kyoto Protocol.

Critics often argue that offsets do not deliver the environmental benefits they promise and that the unregulated and fragmented markets offer companies a licence to pollute. They may, in theory, create a false incentive for companies to believe they can continue with their current business model.

But they also have the potential to bring capital flows into the global south where it is crucially needed. Carbon credits could also be additional tools for companies to offset more emissions than they have historically created, provided that credible offsetting projects of high quality are used.

Another critical question is whether offset-generating renewable energy projects truly depend on carbon finance. Indeed, one of the most important criteria required by the major certification bodies of offsets (so-called ‘standards’ like Verra or Gold Standard) is that of ‘additionality’.

The concept of ‘additionality’ is a crucial criterion for the credibility of offsets. It is the assurance that the reduction in emissions resulting from a project is additional to what would have occurred if it had not gone ahead. Financial additionality is key for the credibility of offsets, meaning that an offsetting project could not have gone ahead without the extra revenues resulting from the sale of carbon credits.

Permanence is another key criterion to ensure that offsetting activities, such as tree planting, will last in perpetuity. Recent forest fires in the American west, burning vast expanses of protected forest which were part of carbon offset projects have illustrated the challenge of ensuring such criterion (once a tree burns, it releases all the carbon it captured back into the atmosphere).

Two dynamics are driving growth in voluntary carbon markets

Despite criticism for failing to deliver the climate benefits promised, some reports suggest that global demand could rise by 15 times by 2030 and 100 times by 2050. Growth is mainly driven by airlines through the sector-wide CORSIA market, by companies especially in hard to abate sectors, and by governments. The latter could use offsetting strategies to reach NDC targets, either by buying credits themselves or requiring corporate leaders to do so on behalf of their companies.

However, voluntary carbon markets are still marginal right now, covering less than 1% of global greenhouse gasses in 2020, though the market momentum cannot be ignored, with the volume of offsets sold rising above $1bn for the first time in 2021. Two dynamics are likely to follow:

- First, civil society led initiatives are working on guidance to inform companies on when and how carbon credits can be used as part of credible corporate climate commitments.

In a nutshell, they should only be used to compensate for a small volume of residual pollution that cannot be eliminated otherwise. The Science-Based Targets initiative (SBTi), the global green gold standard for businesses, now allows companies to factor in carbon offsets as part of their transition journey to net-zero – but only after science-based goals covering the next five to ten years have been adopted and once groups have slashed 90% of their emissions. The IFRS Foundation is also working on providing guidance for the treatment of offset credits in corporate financial and non-financial statements.

- The second dynamic aims to secure the quality of offset credits and to expand their quantity.

The Taskforce on Scaling Voluntary Carbon Markets (TSVCM), headed by former Bank of England Governor Mark Carney, thrashed out a set of core underlying features that carbon credits should adhere to, called the core carbon principles, in an attempt to harmonise carbon certifications. The five core principles are additionality, permanence, exclusive claim, overestimation and the provision of additional co-benefits in line with the UN’s Sustainable Development Goals.

The next steps should be about developing standardised contracts and trading infrastructure to help overcome known shortcomings like low liquidity, scarce financing and limited data availability. A series of newcomers, like asset managers, could offer the liquidity and transparency markets crucially need.

Global demand for voluntary offsets is expected to boom

Voluntary demand for carbon credits, gigatons of CO2 per year

Article 6 of the Paris Agreement is likely to boost government-to-government carbon transactions

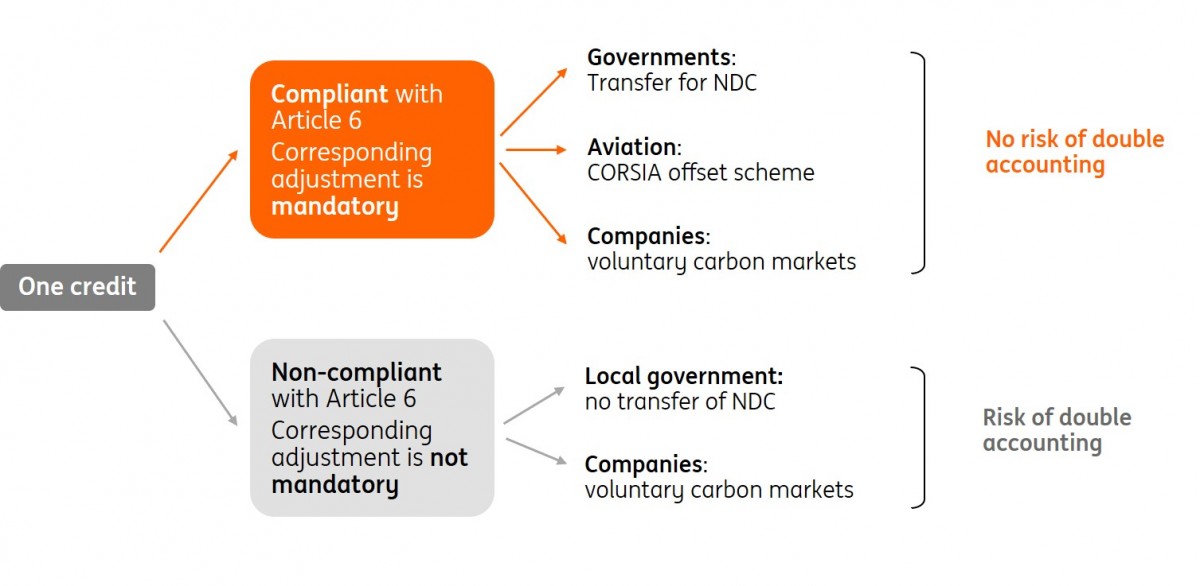

Article 6 of the Paris Agreement has made it possible for countries to purchase emissions reduction abroad and use this towards their own targets, as long as a set of rules are respected. It also agrees that entities other than governments could do so (which includes voluntary carbon markets). After six years of negotiations, this was finally agreed in the very last hours of the COP26 in Glasgow.

The text sets a framework to ensure that any emissions reduction units generated by projects abroad may only be used towards a country’s nationally-determined contributions (NDC) if there are corresponding adjustments in place. In other words, when an emissions reduction unit is sold abroad, the host country (where the project takes place) must cancel out the impact on its own carbon inventories accordingly to mirror the transfer.

This solution was one of the stickiest points of the negotiation, but it avoids one emissions reduction unit being counted by two countries. Practically, it means that only credits which are adjusted for under Article 6 can be used towards another country’s NDC, which guarantees credibility.

Article 6 in the spotlight

Article 6.2 provides an accounting framework for international cooperation, such as linking the Emissions Trading Systems of two or more countries. It also allows for the bilateral transfer of carbon credits between countries and other entities (so-called Internationally Transferred Mitigation Outcomes, ‘ITMO’).

Article 6.4 establishes a centralised UN mechanism (successor of the Clean Development Mechanism from the Kyoto Protocol) to certify tradable credits from emissions reductions generated through offset projects.

For example, an investor in country X could fund solar panels in country Z to replace electricity generated by a coal plant. Emissions are reduced, country Z benefits from the clean energy and, as long as the emissions reductions exceed country Z's Paris target, the investor can sell the credit to country X to use towards its Paris target.

Watch out for greenwashing

However, Article 6 does not make corresponding adjustments mandatory for all voluntary market initiatives. It provides a framework where both would be allowed but doesn't say what they can be used for. Importantly for corporate decision-makers, it means that voluntary offsets without corresponding adjustments can still be used by companies claiming carbon neutrality, keeping the door open for greenwashing (eco-friendly marketing spin).

In the past, companies like Volkswagen and Shell have been accused of reporting their carbon emissions incorrectly and being too heavily reliant on offsetting strategies. It is clear that NGO’s like Greenpeace are no fans of carbon offsets.

The big question coming out of the COP26 in Glasgow is to what extent private voluntary carbon markets comply with the new Article 6 framework.

Ultimately, companies will have the freedom to use offsets towards carbon neutrality claims that do or do not have a corresponding adjustment. Additional guidelines from civil society initiatives and regulators are therefore needed.

The reputational risk that comes with it is already an incentive to focus more on offsets involving a corresponding adjustment. Plus, the Article 6 framework may further encourage improvements of third-party standard setters like Gold Standard or Verra to require corresponding adjustments in voluntary markets, leading to a greater level of credibility.

But it might not be enough. Reputational risk will not drive change on its own. With a large number of voluntary market standard-setters of various quality and little institutional oversight, offsetting schemes could continue to be perceived as the wild west – leaving some room for additional guidelines and more stringent standards.

Corresponding adjustments are mandatory under the Article 6 framework, but not for all offset credits

Price of carbon credits is still inconsistent with the economics of carbon reduction

Companies buying carbon credit in voluntary markets can already choose credits stemming from avoidance or removal projects through nature-based or tech-based solutions.

The latter category tends to trade at a premium to avoidance projects as the investment level to reduce emissions is generally higher. Demand for these projects from sustainable companies or investors is also generally higher as they are more powerful tools than avoidance projects.

Right now, credits can be bought with or without a corresponding adjustment. The two types of credit result in another price differential for voluntary market participants, based on whether an offset credit implies a corresponding adjustment (sold at a premium) or not.

We show in the graph below that the volume and average price of offsets already vary significantly per category of projects due to differences in quality. Forestry and land use projects and renewable energy projects are by far the most popular categories for offsetting. With land use projects trading at prices five times higher than renewable energy projects.

Note that qualities and options also vary within each project category. Unfortunately, due to the lack of transparency in voluntary carbon markets, price spreads data within each category are hard to get hold of.

The result is that most of the offset credits are available for less than €5 – much cheaper than the cost to reduce a ton of carbon with current technologies. In Europe, those costs are represented by the carbon price in the EU ETS, which currently stands at around €90/tCO2. This is much lower than the global price of carbon needed to be consistent with the temperature goals of the Paris Agreement, which should be between €100-€150 per ton CO2 by 2030.

Prices and demand for offsets differ widely between project categories

Average price and volume of carbon offsets per project category in 2020, MtCO2e

Concluding remarks

From the current market dynamics and latest developments at COP26, we conclude that the lines are changing within the offsetting world, putting carbon credits on the agenda of corporate decision-makers:

- Voluntary carbon offsetting makes sense as a last resort to neutralise a company’s residual emissions until a technological alternative becomes available on the market or becomes financially viable.

- Public and private initiatives are flourishing to scale up voluntary carbon markets. They bring more credibility and liquidity to offsetting schemes – two characteristics particularly praised by private actors. There is still a lot of room to improve transparency and data availability.

- The new Article 6 framework could further improve the credibility of voluntary markets.

- It is misleading to believe that voluntary carbon markets are the solution to the climate crisis. Corporate decision-makers need to avoid accusations of greenwashing. Even if offset credits become more credible with corresponding adjustments, prices are likely to remain much lower compared to mandatory carbon markets that are focused on reducing companies’ emission levels.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

19 January 2022

Higher risks, higher costs, higher wages This bundle contains 6 Articles