Vietnam and Switzerland unsurprisingly tagged as FX manipulators

The long-delayed US Treasury FX report found Vietnam and Switzerland having exceeded the three criteria to be labelled a currency manipulator. Now, a period of bilateral talks will start, giving a chance to gauge the Biden administration's early trade policy stance. In the case of Switzerland, this is unlikely to push the SNB to curtail intervention

The Treasury “skipped” one report, and “spared” Thailand and Taiwan

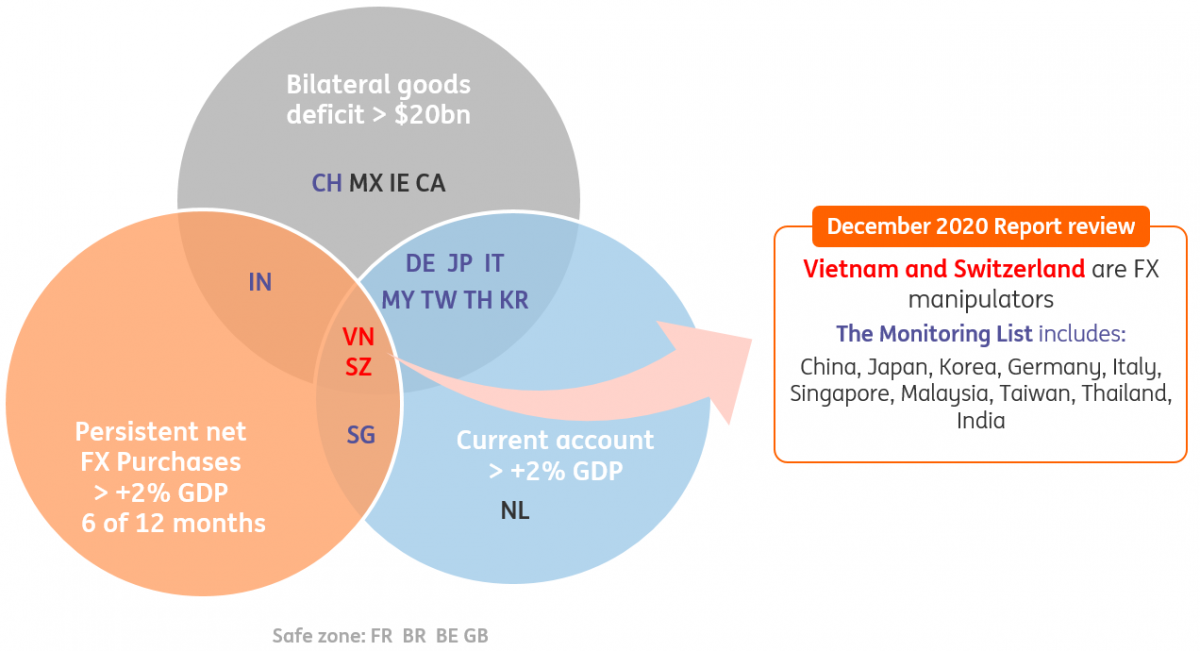

The US Treasury normally publishes its “Report on macroeconomic and foreign exchange policies of major trading partners” twice a year, taking into consideration four quarters of data – either through June or December of each year – to calculate the criteria (Figure 1) that, if met, would cause a country to be labelled an FX manipulator.

Figure 1 - US Treasury's criteria for FX manipulation

However, the last few issues of the report have been delayed, first due to the ongoing trade negotiations with China, then due to the Covid-19 emergency. The Treasury's report for the period January 2019 to December 2019 would have (see: US Treasury FX report preview: Three and a half manipulators) found that Vietnam, Thailand and Taiwan exceeded the three thresholds, while Switzerland would have been marginally below on the FX intervention criteria, according to our estimates.

But the Treasury decided to skip the report covering that period and has moved on to publishing one covering the July 2019-June 2020 period (here is the link to the publication). For this latest period, the Treasury found Vietnam and Switzerland exceeded all three criteria and labelled them as currency manipulators, but “spared” Taiwan and Thailand.

When looking at these results, we must remember that the FX report has had strong political overtones in the last few years and the Treasury staff has a great deal of discretion when deciding how much of the increase in reserves should be seen as FX intervention. Accordingly, it is not surprising in our view that the Treasury had a lighter touch approach on Taiwan – considering its tactical geopolitical alliance with the US – and Thailand – which is less involved than Vietnam in the re-routing of exports from China to avoid US duties.

The report was less focused on China compared to the latest issues. While China remained on the monitoring list (which merely implies deeper scrutiny by the Treasury) due to its large trade surplus with the US, the Treasury explicitly welcomed the fact that the People's Bank of China allowed the renminbi to appreciate after the manipulator tag was lifted in January 2020. Figure 2 below provides an overview of the FX report and shows the other countries included on the monitoring list.

Figure 2 - Overview of the December 2020 FX report

Vietnam’s manipulation tag is hardly a surprise to anyone

Despite having been officially labelled a manipulator only today, Vietnam has been under special scrutiny in the past year and a half as its current account surplus and goods exports to the US spiked during the US-China trade tensions period and the Vietnamese central bank often intervened in the FX market to cap the dong’s appreciation.

In the four quarters ending 2Q20, the Treasury calculated that Vietnam exceeded all criteria as it had a US$58bn goods surplus with the US, a current account surplus worth 4.6% of GDP and the Vietnamese authorities disclosed to the Treasury they had engaged in FX intervention worth 5.1% of GDP.

Earlier this year, the Treasury started a probe into Vietnam’s foreign exchange practices, which was largely seen as a precursor to the FX manipulator designation. According to the US Trade Facilitation and Trade Enforcement Act of 2015, the Treasury must engage in bilateral talks with the authorities of the country labelled as a manipulator. This process should last one year and may eventually lead to export duties or sanctions. In other words, there are no immediate implications for Vietnam.

Vietnam has indeed been one of the key beneficiaries of the re-routing of Chinese products to dodge US tariffs and the US stance on Vietnam and its currency can be considered as a good gauge of how much the US is willing to expand its tough trade stance on China to the broader Asian region. The future FX reports and comments on the manipulation tags will likely begin to provide an idea of the Biden administration's foreign trade policy in Asia.

Switzerland: the SNB will hardly budge

That it was designated a currency manipulator was probably no surprise to Swiss authorities given that Switzerland blew through all of the US Treasury’s three key criteria (as we already highlighted in a September publication). In the four quarters to June 2020, Switzerland’s bilateral trade surplus with the US was US$49bn (US$20bn limit), its current account surplus was 8.8% of GDP (2%) and its FX intervention was 14.2% of GDP (2%).

It would not have been a surprise either for US authorities to have pre-warned their Swiss counterparts of these findings – especially since the Swiss National Bank tomorrow holds its quarterly monetary policy meeting, where negative interest rates and continued FX intervention remain the key tools to address the ‘highly valued’ Swiss franc.

Will the threat of a currency manipulator tag deter the SNB from FX intervention? We suspect this is the start of a long, drawn out process where the two sides in theory will start a dialogue on how to address this issue. And from the looks of today’s price action in both EUR/CHF and USD/CHF, the SNB has no immediate plans to step away from intervention. This has been backed up by the SNB confirming, shortly after the report’s release, that it remains willing to intervene more strongly in the FX market.

At the heart of the issue is a clash between the US wanting a level playing field on international trade against an unwelcome (to the Swiss) intrusion into Swiss sovereignty, be it US recommendations on SNB monetary policy (‘try more quantitative easing’) or fiscal policy (‘cancel the debt brake that generates a serial government under-spend’).

Let’s see whether the SNB addresses these issues head on tomorrow. It would not want to encourage investors to think that its FX intervention activity will be curtailed. Instead the manipulator tag is a subject for the Swiss government/Department of Finance to handle. But Switzerland’s cards have certainly been marked and the SNB may have to add Washington scrutiny to a long list of factors pressing the CHF higher.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article