The US has strong SAF potential, but it needs more policy support

The US is positioned to become the world’s largest SAF producer by 2030, but whether all planned capacity can come online depends on policy support, feedstock availability and offtake agreements. Meanwhile, the feedstock type and carbon intensity of US-produced SAF can impact both domestic tax credit benefits and global trade

Supply-side incentives to make the US a major SAF producer

Unlike the EU and several APAC countries, the US does not have a medium-term sustainable aviation fuel (SAF) blending mandate to boost demand. Instead, the Biden administration has set an SAF production goal of 3bn gallons (9.1mn tonnes) per year, up from the 2024 production estimate of 0.46bn gallons (1.4mn tonnes). The growth of the US SAF market mainly relies on policy incentives from the supply side, and the country is poised to become the largest SAF producer in the world by 2030.

The most attractive policy incentive to realise the production goal is the Inflation Reduction Act (IRA), which provides tax credits ranging from $0.35 to $1.75 per gallon of qualifying SAF produced. These tax credits are playing a visible role in enhancing revenue streams and encouraging producers to supply more SAF into the market.

In addition to the IRA, state-level policy will play a crucial role in scaling up the SAF market from both the supply and the demand side. California has included SAF in its low-carbon fuel standard (LCFS) trading system, while Washington state has proposed to integrate SAF into its Clean Fuels Program. Washington, Minnesota, and Nebraska have established SAF tax credits ranging from $0.75 to $1.5 per gallon of SAF produced, blended or both for about a decade.

SAF production incentives under the Inflation Reduction Act

Compared to other regions, notably the EU, SAF production in the US is expected to be predominantly based on agricultural feedstock, which includes soybean (Hydrotreated Esters and Fatty Acids, or HEFA, through soybean oil) and corn (HEFA through corn oil and Alcohol-to-Jet, or AtJ, through corn grain). Partly because of using agricultural products as feedstock and the associated existing infrastructure, SAF projects in the US are a lot larger in size. This, combined with the current financial incentives, is set to supercharge SAF production in the country.

According to Bloomberg New Energy Finance’s Energy Transition Scenario (ETS), which is moderately more optimistic than business as usual, the US is capable of achieving the 3bn gallons (9.1mn tonne) grand production challenge target in 2030. Sky NRG is taking a more conservative view, projecting US SAF production of 2.3bn gallons (7mn tonnes) in the same year. More broadly in the Americas, South America is set to become an emerging supplier of SAF as well as SAF feedstock (from countries such as Brazil), although the region itself will not likely be a hotspot for SAF demand.

US SAF production estimated to pick up

Production forecasts from different sources, in bn gallons

Will US production get there?

Whether the US can reach the 3bn gallons (9.1mn tonne) production challenge depends on feedstock availability, policy consistency, and offtake agreements.

Feedstock availability

SAF feedstock availability in the US can be affected by domestic agricultural output, processing of waste feedstocks, import, and competition from other fuels like renewable diesel.

First, agricultural feedstocks such as corn and soybeans can play a large role towards 2030 since they provide an opportunity to scale up SAF production quickly. Currently, they’re at a disadvantage compared to waste feedstocks like used cooking oil (UCO) or animal fat because emissions from SAFs produced from agricultural crops are generally higher. This means that extra decarbonisation and efficiency measures are needed to receive tax credits. While policymakers have indicated that agricultural feedstocks can be a major part of SAF production, this will clearly have implications for land use (see also this paper).

Second, waste feedstocks such as used cooking oil, animal fat and municipal waste will be important. Regarding animal fats, the market for collecting and processing them into (aviation) fuels is already quite advanced. That's also the case for used cooking oil – although there seems to be some room to increase the available supply. For municipal waste, it’s not about the supply, but about cracking the code to get facilities that process waste into fuel to a solid business model.

Third, imports of multiple types of feedstock into the US have gone up. US companies are increasing their imports of feedstocks from Asia (UCO) and Latin America (beef tallow from Brazil and soybean oil from Argentina). Such trade flows tend to be quite volatile because of the current nascent state of the market and because the demand side is heavily influenced by policy decisions. Looking ahead, political decisions like a tougher stance on China might affect UCO imports again in the future.

Fourth, SAF production in the US will continue to face strong competition from renewable diesel (RD). Because of the similarity in production processes, feedstock, and infrastructure, a refiner can choose to produce renewable diesel or SAF, or both. In the short to medium term, policy support for RD is slightly more favourable than that for SAF, as indicated in the chart below. RD also has a more predictable demand growth path than SAF in the US. Nevertheless, in the long term, the production and demand for SAF can significantly build up since there are limited alternatives, and the demand for RD may soften because of electrification, which can incentivise more refiners to produce SAF.

Renewable diesel enjoys slightly higher policy incentives than SAF

Combined value of incentives in $/gallon

Policy consistency and innovation

Another factor that can disrupt both the demand and supply of SAF in the US is policy disruption after the elections. The Section 40B and Section 45Z tax credits under the IRA expire at the end of 2024 and 2027 respectively. If Trump is elected, these tax credits may not be scrapped right away, but may not be extended either. The aspirational production and demand targets set by Biden may be scrapped as well.

Policy stability is more guaranteed at the state level, but the current SAF policy design under the LCFS markets has not been effective. Take California as an example – SAF producers can boost revenue by selling SAF to the state’s LCFS market (carrots), but the market itself does not have a limit on emissions from aviation (no sticks). Moreover, the surging demand for renewable diesel has led some refiners to choose to produce renewable diesel over SAF. As a result, SAF only accounts for 0.3% of the LCFS credits sold in California.

It is true that SAF demand will pick up this decade as airline companies, logistics companies, and even companies that have extensive travel emissions (such as consulting companies) work to achieve their sustainability targets. But what would take US SAF demand to the next level is blending mandates at state and federal levels, such as the Renewable Fuel Standards for road transportation.

Offtake agreements

Whether planned US SAF capacity can come online will also depend on project developers’ ability to secure offtake agreements that are ideally long-term. In the US, the length of offtake agreements is low in general, with about 60% of the contract counts featuring purchasing commitments for five years or less. The longer and larger the offtake agreements are, the higher investor confidence tends to be, and the easier project financing might become. Demand-side policy needs to pick up for offtake agreements to be more easily penned.

The sustainability of SAF can affect trade and tax credit benefits

Despite these potential challenges, the US is still expected to see a surge in SAF production this decade, and it is highly likely that it will not be able to absorb it all. So naturally, US SAF producers will look to export their products. This would, in theory, be positive for the global SAF market – but in reality, the kind of SAF products the US can export to which regions will depend on feedstock.

The EU’s Renewable Energy Directive, which lays out the criteria for a certain kind of energy to be considered ‘renewable’, excludes feed and food crop-based feedstock from SAF consideration. This means that US-produced SAF from corn, soybean, and sugar cane will not be able to be used to meet the EU’s blending mandate for flights departing from the bloc. That would be a blow to future US SAF exports, leaving Asia as the principal remaining export destination; it could also create more supply-demand mismatches across different regions across the world.

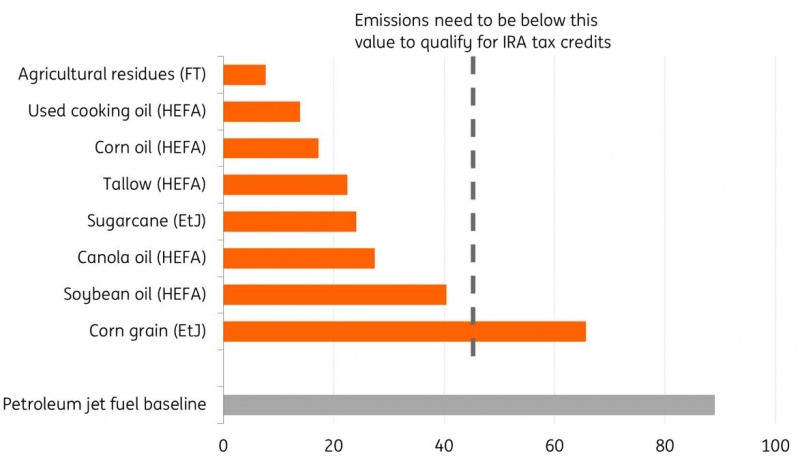

Regardless of the EU’s rule, for US-produced SAF to take advantage of the IRA’s Section 40B tax credits, the life-cycle carbon intensity (CI) of an SAF needs to be at least 50% lower than those of traditional jet fuels, estimated at 89 carbon dioxide equivalent per megajoule, or g CO2e/MJ (guidance for Section 45Z tax credits is expected to be released by the end of the Biden administration). And that is a problem for SAF production pathways such as corn-based AtJ, whose life-cycle carbon intensity is over 60 g CO2e/MJ on average.

SAF life-cycle carbon intensity varies across feedstock types

Core life cycle assessment values, in grams of CO2 equivalent per megajoule of fuel, for a range of feedstocks compared to emissions from conventional jet fuel

A recent policy development is the establishment of a safe harbour provision, which stipulates that corn and soybean-based SAF feedstock produced using all the required Climate Smart Agriculture (CSA) technologies can register an extra 10 g CO2e/MJ and 5 g CO2e/MJ of CI reduction respectively. This can potentially put corn and soybean-based SAFs in the range of 50% CI reduction, making them eligible for the IRA SAF tax credits. This guidance provides significant benefit for US SAF refiners as well as corn/soybean farmers while giving another boost to domestic SAF production.

Nevertheless, these CSA technologies are expensive to install, and the applicability can also depend on geography and soil. Finally, it is worth noting that these CI requirements are only applied to producers seeking for tax credits, but not mandatory for SAF production in general in the US (unlike the EU’s rule). This means that while CI-conditioned tax credits are an important means to drive emissions reduction in SAF production, more policies may be needed in the long term. California has proposed a modification to the current LCFS to only allow companies to claim up to 20% of credits from biomass-based diesel produced from soybean or canola oil – and this may eventually be applied to SAF.

In short, the US is well positioned to become the largest SAF producer in the world, but whether all planned capacity can come online depends on policy support, feedstock availability, and offtake agreements. The life-cycle carbon intensity of SAFs will also determine how much of the fuel can be exported to jurisdictions with stricter rules, as well as how much federal incentive a refiner can get. Meanwhile, the US needs demand-side SAF policies to enhance consumer commitment.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

25 September 2024

Sustainable Aviation Fuels: SAFs are paving the way for greener skies This bundle contains 4 Articles